- THE SUPERVISION BLOG

Sound credit, sustainable growth

24 February 2026

Sustainable lending that supports economic growth benefits everyone: consumers, firms and banks. But bad loans are often made in good times. As lending evolves and risks grow, banks must apply sound underwriting standards to prevent future non-performing loans. From a supervisory perspective, it is important to identify vulnerabilities early on. This is why we will carry out a thematic review, including a targeted data collection, on underwriting in 2026.

Credit is the lifeblood of the economy, enabling investment, entrepreneurship and business growth, and creating opportunities for households. Banks play a central role in channelling credit to these ends. As supervisors, we help ensure that banks remain resilient and can thus fulfil this vital function, but they must lend prudently and engage in sound underwriting to ensure lending remains sustainable.

When granting a loan, the first and most critical step in the bank’s credit risk management cycle is credit underwriting. Applying robust criteria when granting loans helps ensure that potential future losses in the loan portfolio remain manageable and is therefore essential for a bank’s long-term sustainability.

From a broader macroeconomic perspective, sound credit underwriting supports the allocation of funds to households and businesses that are financially viable. This is a prerequisite for investments that drive economic growth. Conversely, granting credit too loosely increases the risk of default, which can undermine financial stability and adversely affect the real economy.[1] Consequently, both microprudential and macroprudential supervisors need to clearly understand banks’ underwriting practices and intervene when they identify high-risk activities.

In light of this, together with the recent recovery in lending and the growing risk environment driven by geopolitical and global trade tensions, ECB Banking Supervision has identified credit underwriting as a supervisory priority. As announced previously, it will launch a thematic review on this topic, including a dedicated data collection, in the first half of 2026.[2]

This data collection has been designed in line with the principles set out in our recent report Streamlining supervision, safeguarding resilience, avoiding overlaps with existing templates and focusing on “need‑to‑have” information. Supervisors carefully analysed banks’ submissions and feedback received following the 2019 exercise and used these insights as a key input to the simplification process by which the number of datapoints was reduced by one third.

Why robust credit underwriting matters

Banks play a fundamental role in the economy by allocating credit to households and firms. By facilitating the flow of credit, banks play a pivotal role in enabling investments, driving economic growth and fostering a resilient economy.

When granting credit, banks must carefully assess the borrower’s future ability to repay. This includes evaluating the borrower’s expected financial position to keep default risk manageable and maintain a low level of non-performing loans.

Banks also need to assess the quality of collateral when the loan is originated, so that they can recover funds efficiently if the borrower defaults. In the long term, robust credit underwriting practices safeguard profitability, support future lending and help build public trust, encouraging individuals and businesses to deposit their funds with confidence.

How supervisors stay vigilant

Given that credit underwriting is vital for banks’ long‑term sustainability and for the broader economy, supervisors have a core responsibility to supervise credit underwriting practices throughout the supervisory cycle. It becomes even more important in an environment of heightened uncertainty. Supervisors recognise that sustainable bank lending is essential for the prudential soundness of banks and positively contributes to the wider economy. A recovery in lending can also coincide with competitive “race-to-the-bottom” dynamics, where standards soften as banks seek to defend or grow market share.

Based on the data currently available, we see that credit growth has recovered since the ECB began cutting rates in June 2024, without any clear signs of a deterioration in standards. However, we do not have sufficiently granular information on corporate lending standards, for example. It is therefore critical to close these data gaps. That is why the thematic review will focus strongly on improving data availability and comparability.

The thematic review and data collection build on the credit underwriting exercise launched in 2019, during which risk indicators were collected from most banks under the ECB’s direct supervision across all major credit portfolios, thereby enabling supervisors to benchmark practices across the banking sector.[3]

Recent trends in credit underwriting

When assessing new lending, supervisors differentiate between portfolios by risk profile. Key portfolios include residential real estate, commercial real estate, loans to firms and consumer credit.

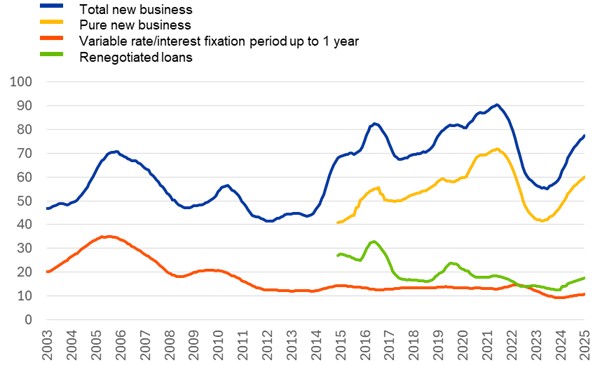

Lending to households for house purchases peaked in 2022, driven by historically low interest rates and increased demand for housing. As inflation rose and the ECB increased interest rates to curb price pressures, demand for mortgage loans declined. When key interest rates began to fall again in 2024, banks partially passed on these lower rates to households and residential real estate lending started to recover. Another observation is that in countries where no borrower-based measures are in place, banks tend to originate loans with riskier lending standards, highlighting the role of borrower-based measures in strengthening standards.

Chart 1

Banks’ new business volumes – loans to households for house purchase

(EUR billions)

Source: ECB MFI interest rate statistics and ECB calculations.

Notes: This chart shows lending for house purchase excluding revolving loans and overdrafts, convenience and extended credit card debt in the euro area (changing composition). The monthly production is summed by period (yearly moving averages). The chart also shows the following subsets of new business volumes: the level of renegotiated loans, the level of pure new business as well as the level of loans with variable rates and with a fixation period of up to one year. Total new business equals pure new business plus renegotiated loans.

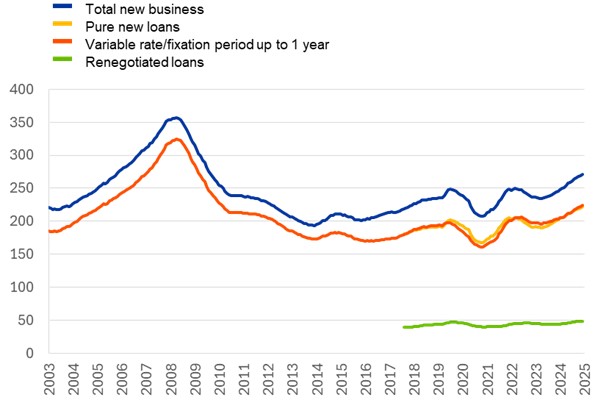

The trend in new lending to firms has been similar, albeit that new lending to firms appears even more closely linked to the real economy and the associated demand for new investment. As with residential real estate, new lending to firms has been rising steadily since 2024.

These trends are also evident in the January 2026 euro area bank lending survey.[4] It shows banks themselves reporting a slight increase in firms’ demand for loans, as well as moderate growth in housing loan demand and a slight decrease in demand for consumer credit.

Renegotiation activity, i.e. new lending that comes from changing the terms of existing loans (for example refinancing, extending maturity or adjusting the repayment schedule), which in some countries represents a significant share of the new business and might concern riskier borrowers, has remained broadly stable for both residential real estate and non-financial corporation portfolios. New loans with variable interest rates, i.e. variable rate and with a fixation period of less than one year, still represent a significant share of corporate portfolios – around 80% of total new business as of December 2025. By contrast, variable loans have become less common in residential real estate portfolios.

Chart 2

Banks’ new business volumes – loans to non-financial corporations

(EUR billions)

Sources: ECB MFI interest rate statistics and ECB calculations.

Notes: This chart shows loans, other than revolving loans, overdrafts, convenience and extended credit card debt, to non-financial corporations in the euro area (changing composition). The monthly production is summed by period (yearly moving averages). The chart also shows the following subsets of new business volumes: the level of renegotiated loans, the level of pure new loans and the level of loans with variable rates and with a fixation period of up to one year. Total new business equals pure new loans plus renegotiated loans.

Next steps in 2026-28

As supervisors, we seek to ensure that lending is underpinned by robust underwriting and risk management. Against the backdrop of rising geopolitical risk and competitive pressures, we want to assess the credit quality of new loans and to use harmonised data to deepen our understanding of recent lending developments.

In March 2026, ECB Banking Supervision will issue a data request to most directly supervised banks. It will cover key risk indicators necessary for assessing the quality of their new lending across all major portfolios, such as the debt service-to-income ratio.

This data request builds on the template used in the 2019 exercise with substantial streamlining. It is now more proportionate and the data points are treated as “need to know” rather than “nice to have”. The request also takes account of existing data to remove duplication and avoid excessive costs for banks. Definitions are harmonised, factoring in national practices and referring to international standards set out by the ECB and the ESRB. For example, the new lending definition will be applied consistently across the sample to ensure a coherent scope, and the loan-to-value calculation will build on the ESRB definition which takes into account national specificities.

In preparing for this workplan, ECB Banking Supervision contacted national supervisors to understand the extent of data being collected at the national level for consumer protection and macroprudential purposes. We also consulted with our international peers to better understand their supervisory working practices and activities. Where possible, the information gained has been integrated into our thematic review to better inform reporting instructions and to enhance bank engagement.

We have carefully analysed banks’ submissions and comments received following the 2019 exercise and the learning points have been crucial for simplifying our template. Our approach aims to strike a balance between gathering the necessary data to assess and benchmark credit underwriting practices and minimising the reporting costs for banks. In comparison with the 2019 exercise, there is also an expectation that banks will have strengthened their information systems and put sound internal processes in place, which should reduce hinderances when it comes to providing data.

Where supervisors identify outliers, they will investigate the underlying causes specific to those banks. If necessary, in line with standard practices, supervisors may initiate targeted follow-up measures, such as on-site inspections.

Increasing transparency

It is important to us that the data we receive are also useful for the banks themselves. With this in mind, the benchmarking results from this project will be shared with banks in an anonymised format, enabling them to assess their positioning and performance relative to their peers. This will help banks strengthen their internal risk management practices and better understand where they stand compared with other institutions when it comes to evaluating and taking risks.

We assessed a sample of the information on credit underwriting that banks provide to their internal management. Banks create and use these information packs internally as a way of monitoring risk. In a review of information packs from 22 banks, we found substantial differences in the level of detail included, with many banks simply reporting new lending volumes and key risk indicators for maturity, repayment type and interest rate. For example, we found little evidence of key risk indicators for underlying lending quality and limited information on banks’ own risk positioning compared with peers.

A major reason for this is the lack, so far, of a common definition for new lending and new lending key risk indicators across banks. It would be beneficial for banks and supervisors if common European definitions of new lending and key priority underwriting metrics were established that properly capture the quality of new lending – for example, debt service coverage or debt to equity ratios.

Harmonised definitions of new lending and priority key risk indicators linked to the quality or risk of loans could improve the availability of data across euro area banks and the market more generally. This would enable more informed benchmarking and generate market intelligence. Banks could use this harmonised reporting to inform and enhance their own risk management and decision-making processes.

For supervisors, having regular, harmonised credit underwriting data would enable more effective risk monitoring and help identify emerging risks earlier in the credit cycle.

Check out The Supervision Blog and subscribe for future posts.

For topics relating to central banking, why not have a look at The ECB Blog?

See also ECB (2025), “Residential real estate (RRE) lending standards: determinants and financial stability implications”, Macroprudential Bulletin, 29 June.

See ECB (2025), Supervisory priorities 2026-28.

See ECB (2020) “Trends and risks in credit underwriting standards of significant institutions in the Single Supervisory Mechanism”, June.

See the euro area bank lending survey results for the fourth quarter of 2025.