- SPEECH

The bank-sovereign nexus: securing progress by completing the banking union

Speech by Claudia Buch, Chair of the Supervisory Board of the ECB, AFME European Financial Integration Conference 2026

Frankfurt am Main, 19 May 2026

Almost two decades after the global financial crisis, the bank-sovereign nexus has weakened, and it is not currently a source of prudential concern.[1] The reforms implemented after the crisis have clearly paid off. But as the European Commission is currently reviewing the state of the EU banking sector,[2] it is time to assess and secure the progress made.

Historically, banking crises have shown us time and again how closely bank and sovereign balance sheets may be interwoven.[3] Weak and fragile banks can make the financial system more crisis prone and weigh on growth, bringing high social and fiscal costs. Weak and highly indebted sovereigns, in turn, can negatively affect the banking system through higher risk premia and heightened macroeconomic uncertainty.

Breaking the bank-sovereign nexus has therefore been one of the main objectives of post-crisis financial sector reforms. In the euro area, where there is national responsibility for fiscal policy but a common monetary policy, the need to weaken the bank-sovereign nexus was a major reason for the creation of the banking union.

Two main factors have weakened the bank-sovereign nexus.

First, strong regulation, supervision and resolution powers have reduced the probability of banks failing and improved the ability to deal with failure. In Europe and globally, significant progress has been made to move from bailout to bail-in by establishing resolution regimes and filling up industry-financed resolution funds. Should losses occur, they should now be borne by banks’ shareholders and creditors and, where needed, industry funds – not taxpayers.

Second, bank balance sheets have strengthened over the past decade, asset quality has improved, and banks have become better capitalised. This reduces the probability and severity of potential future crises, which would carry high economic costs.

Looking ahead, the European Commission’s review of the state of the banking sector provides an opportunity to solidify the progress made and establish sound safeguards to prevent the nexus from tightening again.

The first safeguard is to maintain the institutional framework that governs the bank-sovereign nexus, and to strengthen it if needed. This implies maintaining strong standards in terms of regulation and supervision and closing remaining gaps in the resolution framework by completing the banking union and establishing a European deposit insurance scheme.

The second safeguard is the resilience of the banking sector itself. Clearly, the risk environment has become more challenging; geopolitical risks have materialised.[4] The resilience that has been achieved could be tested. Compared with the period after the sovereign debt crisis, today’s vulnerabilities cannot be mapped as easily onto country-specific macroeconomic imbalances or legacy exposures. Shocks linked to geopolitics, energy, trade or cyber risk can affect different parts of the banking union in different ways and at different times. Across countries, however, competing claims on budgets and often tighter fiscal space may reduce the capacity of sovereigns to absorb future shocks. That’s why the financial sector needs its own strength and resilience to cope with future risk scenarios.

Chart 1: Indebtedness of the government, corporate and household sectors

(percentages of GDP)

Sources: Eurostat, ECB (QSA, GFS, MNA) and ECB calculations.

Notes: Non-financial corporate debt on a consolidated basis. The horizontal lines represent the average for the period. The grey areas show euro area recessions as defined by the Centre for Economic Policy Research.

Tracking bank-sovereign linkages

Banks and sovereigns are linked through various channels. On the asset side, one direct link is in the form of bank holdings of government bonds, while a more indirect link is in the form of fiscal guarantees on loans to households and firms. On the liability side, expectations of government support in times of stress can link the pricing of bank liabilities to the sovereign’s strength. The credibility of the resolution regime has a key role to play here.

1. Direct exposures to sovereign debt

Banks hold government bonds for several economic reasons. Government bonds are widely used as collateral in repo and central bank operations and are a core component of bank liquidity buffers. They thus serve several purposes at once – liquidity, collateral and, in many cases, capital management. Under liquidity coverage rules, sovereign bonds are recognised as Level 1 high-quality liquid assets. Under the EU prudential framework, exposures to Member States’ central governments and central banks denominated and funded in domestic currency are generally assigned a 0% risk weight, and certain sovereign exposures are exempt from the large exposure limit.[5]

This concentration risk is addressed mainly through supervision: competent authorities assess concentration risk and can respond with qualitative measures to strengthen risk management, ask banks to reduce exposures that pose excessive risk, or reflect these risks when setting Pillar 2 capital requirements.[6]

Banks’ actual holdings of government bonds reflect the different functions that these bonds serve as well as shifts in the macroeconomic environment. At the beginning of the banking union in 2014, sovereign debt holdings reached nearly 9% of total assets, corresponding to 190% of CET1 capital.[7] During the period of quantitative easing from 2015 to 2022, sovereign holdings shifted from bank balance sheets to central bank balance sheets. The beginning of the ECB’s balance sheet normalisation in 2023 reversed this trend, also reflecting higher net debt issuance and rising yields on government bonds.

Currently, euro area bank holdings of government bonds are similar to their level at the beginning of the banking union, equivalent to 9.3% of their total assets. By comparison, US commercial banks held Treasury and agency securities equivalent to around 8% to 19% of total assets at the end of 2025, depending on whether a narrower or broader definition is used.[8] The ratio for euro area banks relative to CET1 capital is lower than before, at 170%.[9] Heterogeneity across banks largely reflects banks’ efforts to maintain liquidity ratios by replacing cash with government bonds.

In parallel, banks’ capital adequacy has improved significantly since the global financial crisis, with Tier 1 risk-based capital ratios nearly doubling.[10] After an initial build-up phase, capital requirements have broadly stabilised. EU capital requirements are broadly comparable to those in other jurisdictions, and the new Basel III requirements are manageable for EU banks.

The improved capitalisation of banks has two stabilising effects on government bond markets. First, while euro area banks continue to hold sovereign bonds as a similar share of total assets as at the beginning of the banking union, their loss absorption capacity has increased. Hence, bond holdings relative to total capital are lower. Second, during crises, well-capitalised banks tend to play a stabilising role in sovereign bond markets during periods of high volatility.[11]

The home bias in banks’ sovereign bond portfolios has decreased. The ratio of domestic sovereign bonds to total sovereign bond holdings has declined from 39% in 2014 to around 28% at the end of 2025. Differences across countries largely mirror the volume of government debt outstanding. But this relationship has weakened over time, as banks based in countries with historically high levels of debt have diversified their portfolios (Chart 2).

Chart 2: Euro area banks’ sovereign bond holdings

a) Euro area sovereign bond holdings of euro area banks and home bias, relative to total assets | b) Change in home bias by country, compared with historical average |

|---|---|

(Q4 2014 to Q4 2025, EUR trillions, percentages) | (Q1 2014 to Q4 2025, percentages of total sovereign bond holdings) |

|  |

Sources: ECB (supervisory data) and ECB calculations.

Notes: For a sample of 317 euro area banks with positive holdings. For panel b) the historical mean is the ratio of domestic government bond holdings over total government bond holdings between the fourth quarter of 2014 and the fourth quarter of 2025. Current share indicates the value for the fourth quarter of 2025.

Nonetheless, the reliance on sovereign bond portfolios introduces a trade-off: banks need to balance the benefits for liquidity against greater exposure to interest rate and credit risk.

Large bond portfolios make banks more sensitive to swings in bond markets. If sovereign bond prices fall and yields rise, banks can incur losses on those holdings. This can affect them in several ways: it can reduce the value of their assets, weaken the collateral they can use to obtain funding and put pressure on profits and capital.

The episode of bank distress in March 2023 illustrates this. Silicon Valley Bank showed how unrealised losses on bond portfolios can become a source of stress when confidence is lost and banks are forced to raise liquidity quickly. At the time, this was not a prudential concern for euro area banks.[12] But this episode was still an important reminder that, if banks do not adequately manage funding and liquidity risks, even high-quality assets can become a source of stress if market values fall, confidence weakens, and banks have to sell assets quickly.

To summarise, government bonds are important for banks’ liquidity and collateral management. Euro area banks’ sovereign exposures have remained roughly stable relative to total assets while home bias has fallen. Holdings relative to capital have declined, reflecting banks’ stronger capitalisation, while remaining sizeable. This can expose banks to adverse movements in sovereign markets, particularly if exposures are highly concentrated. To mitigate these risks, banks need to have diversified liquidity buffers and contingency plans to manage sudden liquidity pressures.

2. Loans to households and firms

Loans to households and firms are a second potential link between banks and sovereigns. In the absence of appropriate safeguards, loan losses that cannot be covered out of banks’ own funds can increase fiscal risks. This was a painful lesson learned during the European sovereign debt crisis.

Since the financial crisis, risk reduction has therefore been a main policy objective, and significant progress has been made. Non-performing loans stood at close to 8% in early 2015 and as high as 50% in some countries. Today, this ratio is around 2%, and ratios have largely converged across countries: non-performing loans have tended to increase in countries that started from low levels, while they have tended to decline in countries starting from higher levels.[13] Yet monitoring and addressing the potential effects of higher tariffs and higher energy prices on credit quality remains key.

But there is another, more indirect link between bank loan portfolios and the sovereign. Governments may incentivise banks to support broader policy objectives through their lending decisions, for example by encouraging lending to growing firms and sectors or by helping sustain credit to borrowers under pressure in order to contain employment losses.[14] Such lending is often supported through fiscal measures such as loan guarantees.

During the COVID-19 pandemic and subsequent energy crisis, this indirect bank-sovereign channel was quite active. Governments provided significant financial support to households and firms, which shielded banks from incurring losses and cutting back on lending. They deployed several measures, ranging from direct income support and tax deferrals to public guarantee schemes and liquidity backstops for firms. Direct fiscal support amounted to around 3-4% of euro area GDP in 2020.[15] Up to 35% of new bank lending to non-financial corporations during the pandemic was associated with fiscal support measures.[16] The take-up of guaranteed loans was rapid. By mid-2020, guaranteed lending to firms had reached around 11% of the stock of bank loans to non-financial corporations in Spain before the pandemic, around 5% in France, around 4% in Italy, and around 2% in Germany.

During the 2022-23 energy crisis, fiscal support was again relevant, albeit smaller and more targeted. Discretionary fiscal measures to cushion households and firms from higher prices amounted to around 1.8% of GDP in 2022 and 1.3% in 2023.[17] By 2024, most of the broad energy and inflation-related support measures had begun to be withdrawn.[18]

These fiscal interventions supported banks’ resilience. To some extent, the public sector provided ex post insurance against broader shocks which were difficult to forecast and for which there was limited private sector insurance ex ante.

This has two implications for banks’ risk assessments.

First, risk assessments need to take the effects of fiscal support into account. In a typical recession, loan losses increase. This correlation was partially broken during past recessionary periods because fiscal support measures reduced credit risk. In the short run, guarantees and support measures protected asset quality and helped sustain the flow of credit.[19] But they also embed contingent liabilities on the sovereign balance sheet and can leave a legacy stock of loans whose risk characteristics depend on the terms and duration of the public backstop. Looking ahead, banks’ risk models need to correct for the fact that historical correlations between macroeconomic stress, borrower defaults and bank losses may not hold.

Second, during recent shock episodes, fiscal policy thus acted as a short-term stabiliser. This highlights the intertemporal dimension of the bank-sovereign nexus: support today can reduce financial stress in the short run, while higher debt can constrain fiscal space going forward. Governments may become less able to act as shock absorbers during future downturns. As the IMF’s latest Global Financial Stability Report notes, sovereign risk can spill back into banks through weaker growth, higher funding costs and tighter public budgets.[20] The financial sector thus needs sufficient resilience to continue functioning under conditions of stress.

3. Deposit funding and deposit guarantees

Deposits remain the backbone of euro area bank funding. Over the past two decades, they have even gained in importance. The share of deposits has increased from around 30% in 2007 to 48% in 2025. Retail deposits from households and smaller corporates account for roughly 35% of total funding (Chart 3a).[21] Markets for bank deposits are largely domestic – euro area households hold less than 2% of deposits with banks outside of their home country.[22]

Chart 3: Funding structure of euro area banks

a) Share of deposits from the non-financial private sector and bond funding in banks’ total funding | b) Deposit types by insurance and counterparty, as a share of total deposits and total funding |

|---|---|

(1997 to 2025, percentages)  | (Q4 2025, percentages)  |

Sources: ECB (BSI, supervisory data) and ECB calculations.

Notes: Panel a) – total funding is the total assets of monetary financial institutions excluding the Eurosystem, adjusted by removing liabilities from capital and reserves, MMF shares and remaining liabilities. Panel b) – insured deposits are those covered under a deposit insurance scheme. Wholesale and other deposits are those non-financial private deposits not classified as retail deposits. The share of total funding is estimated by scaling numbers by the share of total deposits in total funding.

At present, around half of all deposits in the euro area are covered by national deposit guarantee schemes. Insured retail deposits thus account for a sizeable share of banks’ total funding (Chart 3b). Deposit insurance has been harmonised at EU level under the Deposit Guarantee Schemes Directive.[23] Eligible deposits are protected up to €100,000 per depositor per bank, and ex ante funds need to be built up to at least 0.8% of covered deposits in most cases. Contributions from banks follow common EBA guidelines designed to reflect differences in banks’ risk profiles.[24] Deposit guarantee scheme funds amount to around 0.92% of EU covered deposits (Chart 4b).

Chart 4: Size of the Single Resolution Fund and deposit insurance funds

a) Single Resolution Fund size | b) Deposit insurance funds |

|---|---|

(€ billions)  | (percentages of covered deposits in the EU)  |

Sources: Single Resolution Board (SRB) annual reports, SRB website, EBA Deposit Guarantee Schemes data and ECB staff calculations.

Despite this harmonisation, deposit guarantee schemes remain national, thereby contributing to the bank-sovereign nexus. This fragmentation can affect the credibility and stability of the system in two ways.

First, credibility depends on the legal promise to protect deposits as well as on the institutional framework behind that promise: whether the scheme is funded and backstopped nationally or jointly, and whether deposit insurance is fairly priced through genuinely risk-based contributions. The more deposit insurance is seen as being credibly pre-funded by the industry, the weaker the implicit link to the sovereign. The more it is seen as relying, in tail events, on national fiscal support, the stronger the link remains. Impact assessments show that, if covered deposits were backed at the European rather than the national level, confidence in deposits would become less dependent on the credit standing of the home sovereign.[25]

Second, the fragmentation of deposit insurance has practical consequences for the management of cross-border banking groups. As long as deposit protection remains national, confidence in deposits is still linked, in tail events, to national arrangements. This helps explain why local resilience remains important for host authorities and depositors, even within a banking union with common supervision and resolution.

At the same time, cross-border groups can manage capital and liquidity more efficiently when resources can move within the group and be used where they are needed. The current framework already allows cross-border liquidity waivers for subsidiaries, provided conditions on the transferability of resources within the group are met, and the ECB has made clear that banks can apply for such waivers. In practice, such waivers remain largely underused.[26]

This is why the Eurosystem’s recent response to the Commission’s targeted consultation on the competitiveness of the banking sector argued that progress on capital and liquidity waivers should proceed together with progress on EDIS:[27] more freedom for capital and liquidity to move across borders requires common safeguards that ensure fair and timely financial support within groups, especially in times of stress. The banking union rests on a single supervisor with a strong track record, and this has helped build trust among authorities and citizens in the safety of the banking system. The next step is to ensure that this trust is matched by a common framework for deposit protection.

4. Bond financing and implicit funding subsidies

Market-based debt finance is a key source of funding. For significant institutions in the banking union, debt securities issued are equivalent to roughly 16% of total liabilities and equity.[28] Bond funding is much less important for banks with assets below €30 billion: debt securities accounted for about 9% of total funding in 2025.

Unlike deposits, bondholders are not protected by explicit guarantee schemes. Yet, the pricing of debt can depend on the strength of the sovereign through another channel: banks that are too big, too connected and thus too systemically important to fail may enjoy undue funding cost advantages. Without appropriate safeguards, governments may be forced to provide financial support to such banks in times of crisis. The expectation of this happening can lead to lower risk premia for systemically important banks, which enjoy implicit funding subsidies as a result. The objective of the reforms has been to internalise these externalities by subjecting these important banks to stricter capital standards, closer scrutiny by supervisors, and by establishing resolution regimes that tilt the balance from bailout to bail-in.

Significant progress has been made since the global financial crisis, when only a few countries had dedicated resolution regimes in place. The Financial Stability Board (FSB) regularly tracks the progress of resolution regime implementation.[29] The FSB’s Key Attributes of Effective Resolution Regimes for Financial Institutions, first agreed in 2011, have become the global standard and have been transposed widely into national legislation, supported by the introduction of recovery and resolution planning, bail-in powers and requirements for additional loss-absorbing capacity for systemic banks.

Figure 1: Building blocks of the too-big-to-fail reforms

Source: FSB (2021), Evaluation of the Effects of Too-Big-To-Fail Reforms: Final Report, 31 March.

At the global level, the FSB standard for total gone concern loss absorbency capacity (TLAC) applies to global systemically important banks (G-SIBs). In the European Union, this global standard is implemented through MREL, the Minimum Requirement for Own Funds and Eligible Liabilities. MREL differs from TLAC in two respects: it applies not only to G-SIBs but to all banks that are expected to be resolved, and it is calibrated to the preferred resolution strategy and other characteristics of each institution. It ensures that banks have sufficient capital and bail-inable liabilities to absorb losses and be recapitalised in resolution, so that critical functions can continue without recourse to taxpayer support.

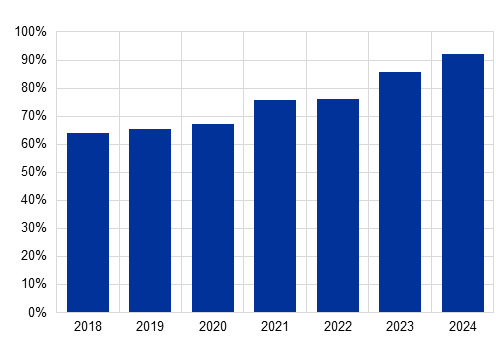

Today, a much larger portion of banks’ bond financing is explicitly designed to be loss-absorbing in resolution. The build-up of MREL is now largely complete for banks in the banking union. According to the Single Resolution Board’s latest monitoring, banks met their final MREL targets in the first half of 2025.[30] The average MREL target for resolution entities, including the combined buffer requirement, was close to 28% of the total risk exposure amount, reflecting this dual function – loss absorption and recapitalisation – of MREL. The aggregate shortfall against final targets has fallen to just below 0.01% and is limited to banks still in transitional periods.[31]

Furthermore, industry funding available for resolution purposes has strengthened significantly, reaching the levels originally envisaged. The Single Resolution Fund has grown to approximately €80 billion as of 2025, corresponding to about 1% of covered deposits in the banking union (Chart 4). This complements the stronger going-concern capital buffers that banks now maintain.

So have the post-crisis reforms worked? Have implicit funding subsidies been reduced? The most comprehensive assessment to date remains the FSB’s evaluation of the too-big-to-fail reforms, which was completed in 2020.[32] It shows the progress that has been made – but it also highlights some gaps.

First, reforms have compressed implicit funding subsidies relative to the crisis period, but not necessarily relative to their pre-crisis levels. In jurisdictions where resolution regimes have been implemented more faithfully and where loss-absorbing capacity requirements are more advanced, funding advantages appear smaller. More recent empirical work confirms that implicit fiscal guarantees for the largest institutions remain economically relevant.[33] Evidence from the 2023 US regional banking stress episode illustrates that, in turbulent times, market participants may still perceive the largest banks as being safer, whether due to stronger fundamentals or expectations of public support.[34]

Second, risks are better priced. The pricing of debt reflects expected losses along the intended bail-in hierarchy under resolution frameworks, credit default spreads have become more sensitive to risks, and credit rating agency practices have reduced rating “uplifts” for expected government support. Evidence for European banks shows that the probability of bail-in is priced, consistent with stronger market discipline.[35]

Third, although crisis management frameworks have been significantly strengthened, gaps remain. In Europe, the recently adopted crisis management and deposit guarantee package is a welcome step, as it should make resolution more workable for a wider set of banks and strengthen the role of industry-funded solutions.[36] But it does not remove the case for completing the banking union, including through a common deposit guarantee framework and credible resolution and post-resolution liquidity arrangements.

In sum, the better pricing of risk is important to align incentives. The more credible the resolution framework, the less banks can bet on future fiscal support in a gone-concern scenario, and the less incentivised they are to take undue risks in the going concern. Credible supervision and resolution are thus two sides of the same coin: they align the incentives of banks with those of society and they enable banks to take risks – but not at the expense of others.

5. Bank recapitalisation by the government – the channel of the past?

The most direct bank-sovereign channel arises when public authorities inject capital into banks in an acute crisis situation. This is when banking sector losses migrate from private to public balance sheets.

The global financial crisis and the euro area crisis illustrate the scale this channel can reach. Between 2008 and 2014, EU Member States committed substantial public resources to stabilise banking systems through capital injections, asset protection schemes and, in some cases, nationalisations.[37] Relative to general government expenditure, support for banks amounted to about 9%, of which around two-thirds was used for recapitalisation measures and one-third for impaired-asset measures. Output losses and higher unemployment added to these direct fiscal costs of banking crises.

These interventions restored confidence, preventing a disorderly deleveraging and failure of undercapitalised banks. Without such interventions, undercapitalised banks facing losses would otherwise have had to cut lending, further dragging down growth. But at the same time, the interventions contributed materially to an increase in government debt. Public recapitalisation is not a sound long-term strategy, as it can distort incentives for bank owners and creditors.

This explains why post-crisis reforms sought to make public recapitalisation the exception rather than the default response to bank distress. Higher capital requirements, more intrusive supervision and the creation of resolution frameworks are designed to ensure that banks can absorb losses privately and, if a bank does fail, it can be resolved without drawing on taxpayers’ money.

Yet the recapitalisation channel has not disappeared entirely. The relevant European framework provides narrowly defined exceptions – most notably precautionary recapitalisation for a solvent institution to remedy a serious disturbance in the economy and preserve financial stability.[38] Any use of public money to recapitalise banks remains exceptional and subject to strict safeguards.

6. Taxing bank profits

A final bank-sovereign channel can run through the taxation of bank profits. Facing higher fiscal debt and tighter budgets, a few governments have introduced extraordinary levies or “windfall” taxes on bank profits.[39]

Bank taxes can strengthen the nexus in two ways. First, they can make public finances more directly reliant on the banking sector as a revenue source and thereby increase the political relevance of banks’ profits and balance-sheet choices. Second, if such taxes materially reduce retained earnings, they can weaken banks’ capacity to build capital organically – thereby weakening the first line of defence against shocks.

The ECB has thus cautioned that extraordinary bank profit taxes should be carefully designed and assessed from a financial stability perspective.[40] Such taxes require a thorough analysis of potential negative consequences on bank resilience and lending, including the risk of market fragmentation. Similarly, the IMF stresses a basic trade-off: while such taxes can raise revenue, they may make it harder for banks to accumulate buffers that are crucial when conditions turn.[41]

Beyond banks: new forms of finance-sovereign linkages?

The channels discussed so far reflect the role banks play in credit creation, deposit-taking and sovereign debt markets. But the underlying mechanisms can arise elsewhere in the financial system. Private financial liabilities can become linked to the sovereign whenever confidence in those liabilities depends, directly or indirectly, on public-sector assets, public guarantees or public backstops.

This matters because financial intermediation has changed since the global financial crisis. While banks remain central to the European financial system, non-bank financial intermediation has grown in importance. This can support more diversified sources of finance and a broader allocation of risk. But vulnerabilities can emerge outside the banking perimeter, especially where financial institutions engage in liquidity transformation, rely on public-sector assets as safe and liquid collateral, or engender expectations of public intervention in times of stress.

The channels differ across financial institutions. A bank holding domestic sovereign bonds has a different risk profile from a money market fund investing in government securities or a stablecoin issuer backing its liabilities with short-term public debt. The policy issues also differ. Banks perform a distinctive role in money creation, lending and payments, and they are subject to specific prudential and resolution frameworks. Still, these examples raise a common question: how resilient are private liabilities when confidence depends on the liquidity, valuation or perceived safety of public-sector assets?

This broader perspective is relevant for crisis preparedness. Recent episodes of stress have shown that liquidity strains in non-bank finance can spread quickly across markets, including sovereign bond markets. This can affect markets that are central to monetary policy transmission and to the financing of governments. Where public authorities are expected to provide emergency liquidity or market backstops, the boundary between private risk-taking and public support can become less clear.

As financial intermediation evolves, resilience thus needs to be built beyond the banking sector, and potential adverse consequences for financial stability need to be addressed. This is particularly important in those parts of the system where liquidity transformation, leverage and reliance on public-sector assets could amplify stress. Otherwise, the interaction between financial institutions and the sovereign may reappear in new forms.

Summing up

The balance sheets of banks and sovereigns are closely interlinked, and both reflect the strength of the economy. Many of these linkages are unavoidable if the economy and banks are to function well. But there is one link that can and should be cut: a bank-sovereign nexus through which weak banks can infect public-sector balance sheets, or vice versa.

Significant progress has been made here. Banks are better capitalised than they used to be, and institutional frameworks to deal with bank distress without drawing on taxpayers’ money have improved. Supervision and regulation have been strengthened. Resolution frameworks have been established, including industry-financed funds and bail-in tools.

The resilience of sovereign debt markets is, of course, no less important in the current fiscal environment.[42] In this regard, the governance of the euro area’s fiscal architecture was strengthened – through the Six-Pack legislation and Two-Pack legislation, which reinforce the multilateral surveillance framework, as well as the establishment of the European Stability Mechanism to provide financial assistance in crises.

All of this weakens the bank-sovereign nexus, and the progress made should not be underestimated.

But could the bank-sovereign nexus re-emerge? Clearly, risks have risen – geopolitical risks have materialised and are weighing on the growth outlook. The full effects of recent shocks on credit quality will materialise only over time. Fiscal capacity is becoming more strained. In an adverse scenario, this could strengthen the bank-sovereign nexus.

The ongoing review of the EU banking sector by the European Commission provides an opportunity to prevent the bank-sovereign nexus from re-emerging and to further strengthen the framework.

Maintaining strong regulatory and supervisory standards is key to preserving the resilience that has been built. Strong, effective supervision, regulation and resolution are the foundation of the credible promise not to use taxpayers’ money to bail out financial institutions. This foundation ensures that banks can absorb shocks from a position of strength and provide services to the economy at all times. It also supports citizens’ trust in the stability of banks.

Closing the remaining gaps in resolution frameworks and completing the banking union remain essential. The euro area lacks a European deposit insurance scheme, which would reassure savers that their deposits enjoy the same level of protection in every country, irrespective of the strength of the respective sovereign.

Not least, crisis preparedness beyond banking is important to maintain financial stability. Banks and non-banks play different roles in the economy, but the underlying mechanisms are the same: resilience needs to be built before stress emerges, especially where liquidity transformation, leverage or reliance on public-sector assets could amplify shocks.

I would like to thank Patrick Amis, Karen Braun-Munzinger, Sharon Donnery, Maciej Grodzicki, Asen Lefterov, Pierre Marmara, Allegra Pietsch, John Roche, Kallol Sen, Sebastian Scheffler, Panagiota Tsioutsia, Roberto Ugena, and Florian Weidenholzer for their most helpful input and comments on an earlier version. All remaining errors and inaccuracies are my own.

See European Commission (2026), Targeted consultation on the competitiveness of the EU banking sector, 11 February.

For a historical account, see Calomiris, Charles W. and Haber, Steven (2014), Fragile by Design; the Political Origins of Banking Crises and Scarce Credit, Princeton University Press.

The IMF’s Global Financial Stability Report, issued in April 2026, has a clear message: the current level of resilience in the financial system is not the endpoint but a reminder of what needs to be preserved. See IMF (2026), “Global Financial Markets Confront the War in the Middle East and Amplification Risks”, Global Financial Stability Report, April.

Under Article 114 of the Capital Requirements Regulation (CRR), exposures to central governments and central banks are in principle assigned a 100% risk weight, unless one of the preferential treatments in that Article applies. But under Article 114(4), exposures to Member States’ central governments and central banks receive a 0% risk weight where they are denominated and funded in the domestic currency of that sovereign or central bank. Under Articles 395 and 400 of the CRR, the general large exposure limit is 25% of Tier 1 capital, but exposures to central governments and central banks that would receive a 0% risk weight under the standardised approach may be exempted from that limit. On the liquidity side, Article 10 of Commission Delegated Regulation (EU) 2015/61 recognises claims on, or guarantees by, central governments and central banks as Level 1 assets subject to eligibility conditions.

See Articles 81, 97, 98(1)(b), 104 and 104a of Directive 2013/36/EU. Article 81 requires competent authorities to ensure that concentration risk is addressed and controlled by institutions, including through written policies and procedures. Article 98(1)(b) includes the exposure to and management of concentration risk among the technical criteria for the supervisory review and evaluation process. Articles 104 and 104a provide the basis for supervisory measures, including additional own funds requirements and measures to reduce excessive risks. See also EBA (2022), Guidelines for common procedures and methodologies for the supervisory review and evaluation process (SREP) and supervisory stress testing, March.

These data are for the fourth quarter of 2014 and are taken from ECB supervisory banking statistics for a sample of 155 euro area banks that reported exposures to any sovereign of at least €10,000, including less significant and significant institutions.

Based on Federal Reserve H.8 data. In December 2025, US commercial banks held around USD 4.65 trillion in Treasury and agency securities, compared with total assets of around USD 24.58 trillion. The category is broader than euro area government bond holdings, as it includes US Treasury securities, US government agency obligations and agency/GSE mortgage-backed securities. A narrower non-MBS Treasury and agency measure stood at around USD 1.96 trillion, or around 8% of total assets.

These data are for the fourth quarter of 2025 and are taken from ECB supervisory banking statistics for a sample of 317 euro area banks that reported exposures to any sovereign of at least €10,000, including less significant and significant institutions.

Dzezulskis, S., Libertucci, M. and McPhilemy, S. (2026), “Understanding the banking sector capital framework in the European Union”, Occasional Paper Series, No 387, ECB.

ECB (2023), “Sovereign bond markets and financial stability: examining the risk to absorption capacity”, Financial Stability Review, November.

Following the turmoil in the United States, the ECB and European Banking Authority (EBA) collected ad hoc data on the bond portfolios of euro area banks. In so doing, they found that the losses were contained relative to banks’ capital and liquidity buffers

At the end of 2025, 2.2% of loans and advances, excluding cash balances at central banks and other demand deposits, were classified as non-performing. See ECB (2026), Supervisory banking statistics for significant institutions – Fourth quarter 2025, March.

The interaction between banks and broader policy objectives in terms of supporting the economy has been described by Hellwig, Martin (2000), “Banken zwischen Politik und Markt: Worin besteht die volkswirtschaftliche Verantwortung von Banken?“, Perspektiven der Wirtschaftspolitik, Vol. 1, No 3, pp. 337-356.

Haroutunian, S., Hauptmeier, S. and Leiner-Killinger, N. (2020), “The COVID-19 crisis and its implications for fiscal policies”, Economic Bulletin, Issue 4, ECB.

This and the following information has been taken from Falagiarda, M., Prapiestis, A. and Rancoita, E. (2020), “Public loan guarantees and bank lending in the COVID-19 period”, Economic Bulletin, Issue 6, ECB.

Ferdinandusse, M. and Delgado-Téllez, M. (2024), “Fiscal policy measures in response to the energy and inflation shock and climate change”, Economic Bulletin, Issue 1, ECB.

ECB (2025), Economic Bulletin, Issue 4.

Gabriel Jiménez, Luc Laeven, David Martinez-Miera, José-Luis Peydró (2022) “Public guarantees, private banks’ incentives, and corporate outcomes: evidence from the COVID-19 crisis”, Working Paper Series, No 2913, ECB.

International Monetary Fund (2026), “Global Financial Stability Report: Global Financial Markets Confront the War in the Middle East and Amplification Risks”, Global Financial Stability Report, April.

See ECB (2026), Supervisory banking statistics for significant institutions – Fourth quarter 2025, March; and ECB (2026), MFI aggregated balance sheet statistics, February.

1.8% as at March 2026. See Rumpf, M. (2024) “Cross-border deposits: growing trust in the euro area”, the ECB Blog

Directive 94/19/EC of the European Parliament and of the Council of 30 May 1994 on deposit-guarantee schemes (OJ L 135, 31.5.1994, p. 5) and Directive 2014/49/EU of the European Parliament and of the Council of 16 April 2014 on deposit guarantee schemes (OJ L 173, 12.6.2014, p. 149).

See the European Commission’s webpage on “Deposit guarantee schemes”.

See European Commission (2016), Effects analysis on the European deposit insurance scheme (EDIS).

While the Bank Recovery and Resolution Directive provides for the conclusion of intra-group financial support agreements, these have been very rarely used and have been insufficient to foster cross-border integration. See Enria, Andrea (2020), “Fostering the cross-border integration of banking groups in the banking union”, The Supervision Blog, ECB, 9 October.

ECB (2026) “Eurosystem response to the EU Commission’s targeted consultation on the competitiveness of the EU banking sector”, April

Data for the fourth quarter of 2025.

FSB (2025), G20 Implementation Monitoring Review – Interim Report, 13 October.

Single Resolution Board (2025), SRB MREL Dashboard, H1 2025.

MREL ensures that banks have sufficient capital and bail-inable liabilities to absorb losses and be recapitalised in resolution, so that critical functions can continue without recourse to taxpayer support. This two-part function – loss absorption and recapitalisation – explains why MREL requirements are higher than going-concern capital requirements.

FSB (2021), Evaluation of the Effects of Too-Big-To-Fail Reforms: Final Report, 31 March.

The study considered evidence from 19 jurisdictions over the period 2002-2021. See Vasconcelos, L.N.C., Schiozer, R.F. and Giacomini, E. (2024), “Do Bank Resolution Reforms Reduce Banks’ Funding Costs Advantage?”, SSRN Working Papers, No 4625058, SSRN. See also Cetorelli, Nicola and Traina, James (2021), “Resolving ‘Too Big to Fail’”, Journal of Financial Services Research, Vol. 60, pp. 1-23, which finds that living-will regulation increased large banks’ cost of capital and thus reduced too-big-to-fail subsidies in the United States.

Caglio, Cecilia; Dlugosz, Jennifer; Rezende, Marcelo (2025), “Flight to Safety in the Regional Bank Stress of 2023”. Board of Governors of the Federal Reserve System

Velliscig, Giacomo; Floreani, Juri; Polato, Matteo (2022), “How do bail-in amendments in Directive (EU) 2017/2399 affect the subordinated bond yields of EU G-SIBs?”, Journal of Empirical Finance, Vol. 68, pp. 173-189. The paper studies the yield reaction of subordinated bonds around the implementation of Directive (EU) 2017/2399, which entered into force on 28 December 2017.

See European Parliament (2026), “New rules to address bank failures protecting taxpayers and depositors”, press release, 26 March.

According to Annex 5 of the European Commission’s State Aid Scoreboard 2017, recapitalisation measures amounted to about €688 billion, of which around €353 billion was actually used, while impaired asset measures amounted to roughly €148 billion used.

See Article 32(4)(d)(iii) of Directive 2014/59/EU – the Bank Recovery and Resolution Directive – and Article 18(4)(d)(iii) of Regulation (EU) No 806/2014 – the Single Resolution Mechanism Regulation. Precautionary recapitalisation is also subject to approval under the EU State aid framework, in particular Article 107(3)(b) TFEU.

European Parliament (2025), The taxation of the EU’s financial sector – options and experiences, June. Note that bank taxes are conceptually different from banks’ ex ante contributions to resolution funds and deposit guarantee schemes, which are intended to support financial stability rather than to raise general fiscal revenue.

ECB (2023), “Opinion of the European Central Bank of 15 December 2023 on the imposition of an extraordinary tax on credit institutions”. A similar set of concerns has been raised more recently in the context of a new Spanish tax on net interest and fee and commission income. See Banco de España (2025), “The new tax on financial institutions”, Financial Stability Report, Spring 2025, citing ECB (2024), “Opinion of the European Central Bank of 17 December 2024 on a tax on the net interest and commission income of certain financial institutions”.

Maneely, M. and Ratnovski, L. (2024), “Bank Profits and Bank Taxes in the EU”, IMF Working Papers, No 143, International Monetary Fund.

See Schnabel, I. (2026), “The quiet erosion of central bank independence”, speech at the Fifth Annual Charles Goodhart Lecture, Frankfurt am Main, 7 May.

Europos Centrinis Bankas

Komunikacijos generalinis direktoratas

- Sonnemannstrasse 20

- 60314 Frankfurtas prie Maino, Vokietija

- +49 69 1344 7455

- media@ecb.europa.eu

Leidžiama perspausdinti, jei nurodomas šaltinis.

Kontaktai žiniasklaidai