- 25 January 2019

- Press release

ECB publishes supervisory banking statistics for the third quarter of 2018

- Capital ratio increases slightly in the third quarter of 2018, with total capital ratio at 17.83%.

- NPL ratio down to 4.17%, lowest level since time series first published in 2015.

- Liquidity coverage ratio stable at 140.93%.

Capital adequacy

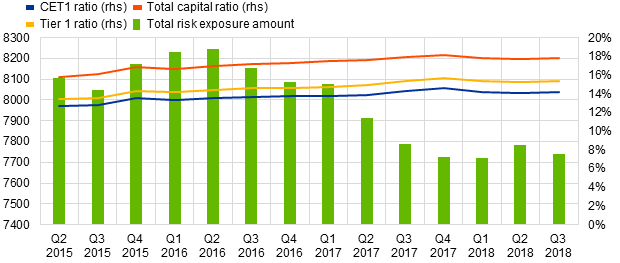

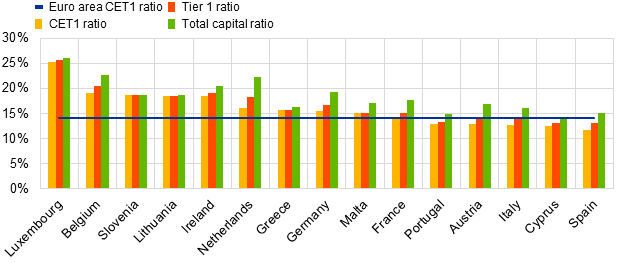

All capital ratios for the group of significant institutions, i.e. the banks supervised by the ECB, have slightly increased in the third quarter of 2018 compared with the previous quarter. The Common Equity Tier 1 (CET1) ratio stood at 14.18%, the Tier 1 ratio at 15.40% and the total capital ratio at 17.83%. Average CET1 capital ratios at participating Member State level range from 11.75% in Spain to 25.27% in Luxembourg.

Chart 1

Total capital ratio and its components by reference period

(EUR billions, percentages)

Source: ECB.

Chart 2

Capital ratios by country

(Percentages)

Source: ECB.

Note: Data for some countries are not displayed either for confidentiality reasons or because there are no significant institutions at the highest level of consolidation.

Asset quality

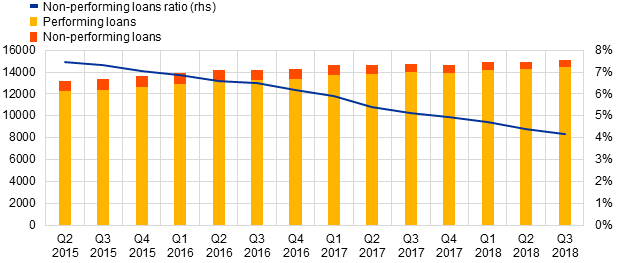

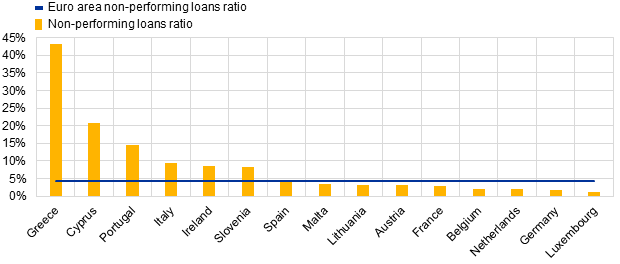

The non-performing loans ratio (NPL ratio) fell further to 4.17% in the third quarter of 2018, which was the lowest level since supervisory banking statistics were first published in the second quarter of 2015. The lowest average ratio is at 1.04% in Luxembourg, the highest at 43.36% in Greece.

Chart 3

Non-performing loans by reference period

(EUR billions, percentages)

Source: ECB.

Chart 4

Non-performing loans ratio by country

(Percentages)

Source: ECB.

Note: Data for some countries are not displayed either for confidentiality reasons or because there are no significant institutions at the highest level of consolidation.

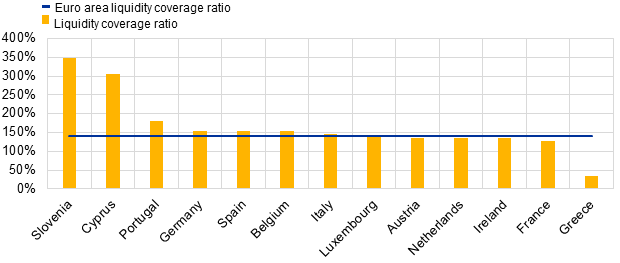

Liquidity

The liquidity coverage ratio stood at 140.93% in the third quarter of 2018, stable compared to the second quarter (140.91%). Among the countries with a sufficient number of institutions, the average values range from 33.09% in Greece[1] to 347.54% in Slovenia.

Chart 5

Liquidity coverage ratio by reference period

(EUR billions, percentages)

Source: ECB.

Chart 6

Liquidity coverage ratio by country

(Percentages)

Source: ECB.

Note: Data for some countries are not displayed either for confidentiality reasons or because there are no significant institutions at the highest level of consolidation.

Factors affecting changes

Supervisory banking statistics are calculated by aggregating data reported by banks that report COREP (capital adequacy information) and FINREP (financial information) at that point in time. Changes in the amounts shown from one quarter to another can be influenced by the following factors:

- Changes in the sample of reporting institutions;

- Mergers and acquisitions;

- Reclassifications (e.g. portfolio shifts where certain assets are reclassified from a particular accounting portfolio to another).

For media queries, please contact Stefan Ruhkamp, tel.: +49 69 1344 5057.

Notes

- The complete set of Supervisory banking statistics with additional quantitative risk indicators is available on the ECB’s banking supervision website.

- The figures for Greek banks are affected by external factors that temporarily hinder the use of the LCR as an appropriate liquidity risk indicator.