Keynote speech by Frank Elderson, Member of the Executive Board of the ECB and Vice-Chair of the Supervisory Board of the ECB, at the 7th World Congress of Environmental and Resource Economists

Lisbon, 2 July 2026

In my speech today, I will talk about two factors that have recently contributed to inflation volatility and economic uncertainty in the euro area: war in the Middle East and risks arising from the climate and nature crises. These factors themselves have a common cause: continued overreliance on burning fossil fuels and, in Europe’s case, on imported fossil fuels in particular. Accelerating the transition to net zero carbon helps insulate Europe from these shocks. It is tempting, then, to say we can kill two birds with one stone. While that is not necessarily the most apt idiom to use at a congress of environmental economists, I also think it oversimplifies the task at hand. As I will discuss today, arriving at net zero carbon requires a complementary range of policies if it is to be delivered in an orderly and relatively low-cost fashion.

Costs of energy insecurity

Fossil fuels once again cast a pall over Europe’s economic prospects at the start of this year, just a few years after the one caused by Russia’s invasion of Ukraine. While the energy crisis triggered by the war in the Middle East has so far been less severe, it has pushed up oil prices again, threatened the supply of certain products and generated a substantial degree of uncertainty. Europe’s continued reliance on imported fossil fuels makes the region especially vulnerable to such events.

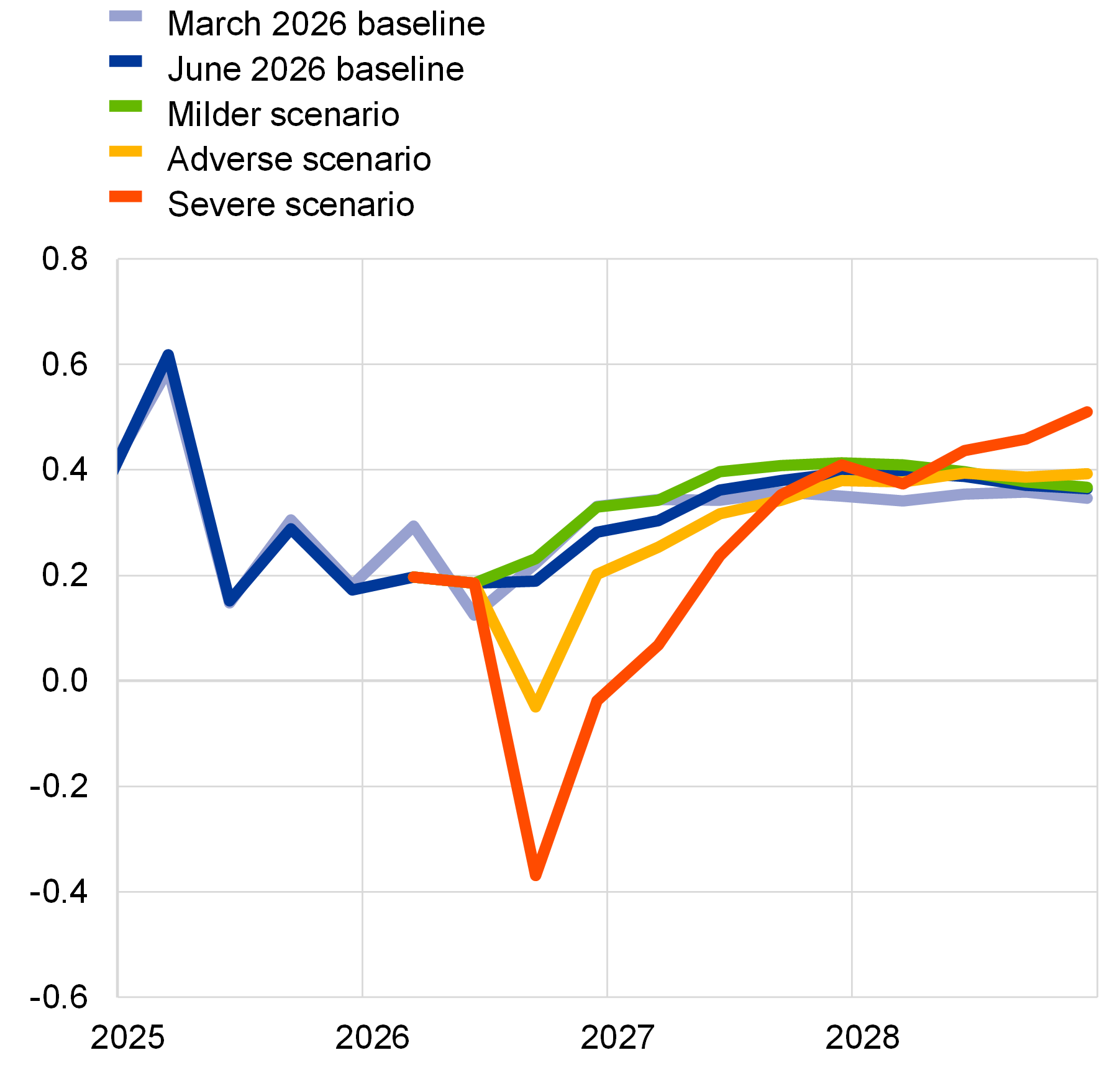

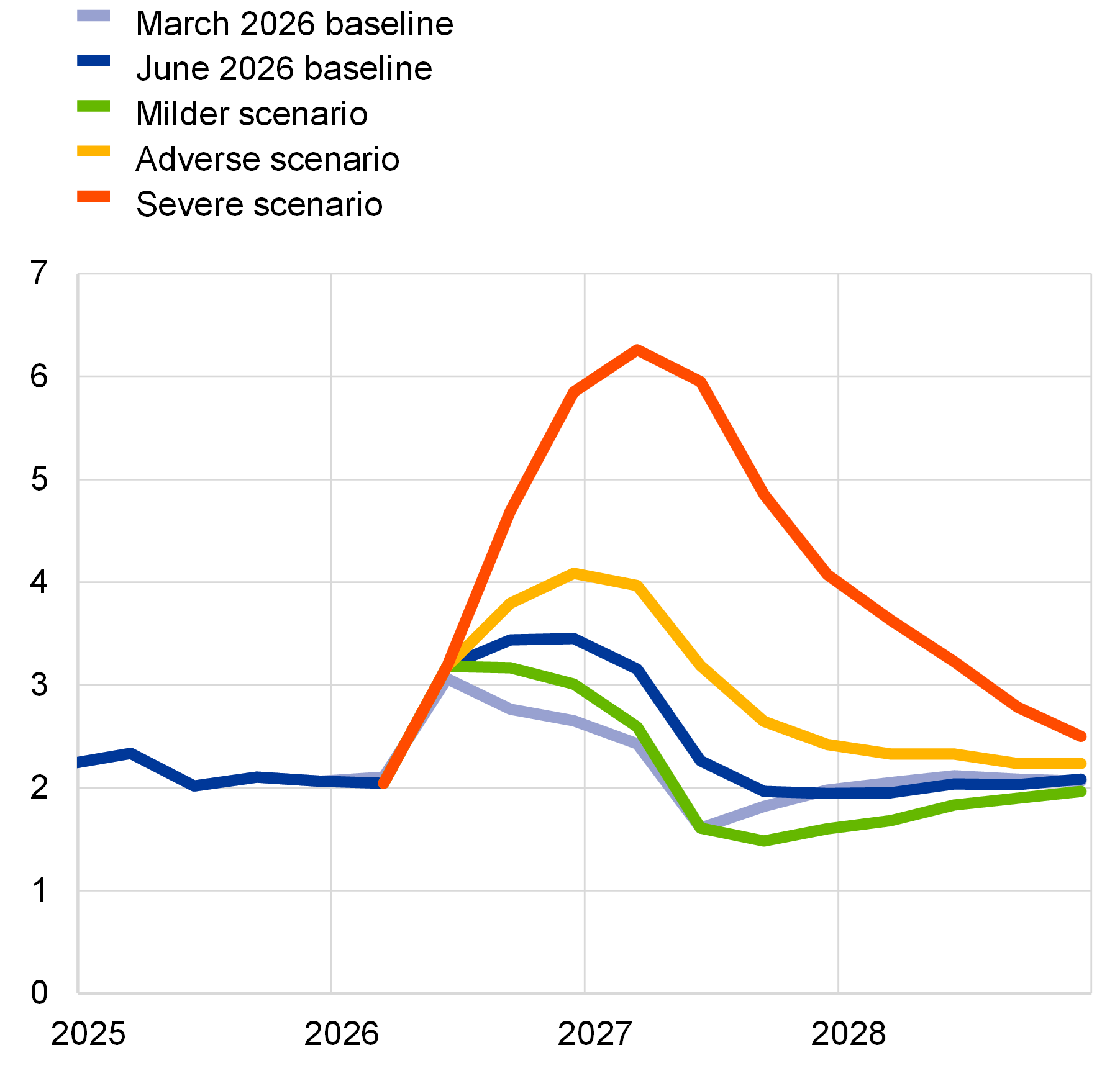

The June Eurosystem staff projections revised the baseline outlook for growth down in both 2026 and 2027 and revised inflation up over that same period compared with the March projections. Yet the impact of the war incorporated into our baseline is just one of the many possible outcomes. We discussed a range of scenarios where the macroeconomic impact could be much more severe or possibly milder than in our baseline (Chart 1). Under the adverse scenario, energy price increases would be stronger and more persistent and the propagation of the shock greater than in the baseline. In this scenario, economic growth in 2027 would be 0.3 percentage points lower and inflation 0.7 percentage points higher than in the baseline. The severe scenario assumed even stronger and more persistent pressures on energy prices, with HICP inflation peaking over 6% in early 2027. We also considered a milder scenario, which may be more relevant if the recent moderation in oil prices persists.

Chart 1

Impact of Middle East conflict on macroeconomic outlook in the euro area across different scenarios

Real GDP growth | HICP inflation |

|---|---|

(quarter-on-quarter growth rate) | (year-on-year growth rate) |

|  |

Policymaking under such an unusually high degree of uncertainty is difficult, and so too are the decisions made by companies and households. Higher input costs and lower demand weigh on consumption[1] and investment, with ECB research finding that European companies cut back on capital spending and research and development following oil price shocks.[2] The same research finds that US companies do not typically react in the same fashion, in no small part owing to the greater reliance of the European economy on imported fossil fuels.

The global economic disruption caused by the closure of the Strait of Hormuz goes beyond higher energy prices. A large share of world production of helium and fertiliser also passes through the Strait, affecting the production of computer chips and food worldwide.

Costs of climate and nature risks

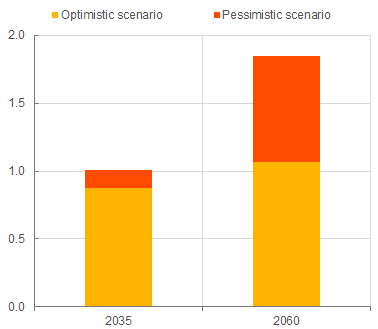

And it’s not just the situation in the Gulf that is affecting food production. Climate change is also having an increasing impact on food prices worldwide. Several recent spikes in the prices of foods such as olive oil, cocoa and coffee have been linked to historically unprecedented weather extremes.[3] As shown in the left-hand panel of Chart 2, ECB research estimates that the 2025 summer heatwave could increase unprocessed food prices in the euro area by 0.4 to 0.7 percentage points after one year.[4] The heatwave in Europe that occurred over the past fortnight could exacerbate the impact on food prices.

Continued climate change could further worsen outcomes. The impact of heatwaves on food prices is non-linear and larger when the absolute temperature is hotter. A recent study finds that food prices in Europe could rise by as much as 1.8 percentage points after an extreme summer in the climate that is expected to prevail in the 2060s, relative to a hypothetic scenario without any climate change (Chart 2, right-hand panel).[5] Nature degradation also poses risks to food prices. Eurosystem research based on French data has found that an acute loss in the provision of ecosystem services, such as a decline in pollination, could increase headline HICP inflation by as much as 0.5 percentage points.[6] Central banks therefore need to account for the ongoing climate and nature crises when preparing their inflation forecasts, or risk underestimating the degree of inflationary pressures.

Chart 2

Impact of summer heatwaves on food prices

a) Impact of the 2025 heatwave on euro area unprocessed food prices after 12 months | b) Estimated impact of a typical summer heatwave on food prices in Europe under future projected climate |

|---|---|

(percentage points) | (percentage points) |

|  |

Sources: ECB analysis based on Kotz, M., Kuik, F., Lis, E. and Nickel, C. (2024), “Global warming and heat extremes to enhance inflationary pressures.” Commun Earth Environ 5, 116.

Notes: Both charts show the cumulative deviation of prices from baseline after 12 months due to extreme June/July/August temperatures. The charts are based on combining elasticities of a 1°C increase in temperatures with realised 2025 summer temperatures (Chart a) and results from 21 global climate models (Chart b). Elasticities are estimated with a global panel regression approach, using monthly prices and high-resolution climate data. Chart b: Projected temperatures of an extreme summer (i.e., in the upper tail of the temperature distribution) in future climates are retrieved from climate model results under an optimistic (“below 2°C by 2100”, Representative Concentration Pathway 2.6) and a pessimistic (“hot house world”, Representative Concentration Pathway 8.5) emissions scenario. The estimates can be understood as the additional impact on food inflation attributed to future higher temperatures. The approach does not make any assumptions about future inflation dynamics, macroeconomic factors or adaptation to climate change and can therefore be understood as a stylised sensitivity analysis.

Beyond the direct impact on prices, two further channels matter for monetary policy and central banks: disruption to economic activity and risks to financial stability, which can in turn impair the transmission of monetary policy to the real economy.

The European Environment Agency estimates that extreme climate and weather events caused over €200 billion worth of damage in Europe between 2021 and 2024.[7] Yet this is just a partial estimate, capturing only the direct physical damage caused at the time of the event. Extreme events can have a durable impact on economic activity. Looking at European regions, output is on average 1.5 percentage points lower two years after a summer heatwave, 3 percentage points lower four years after a drought and 2.8 percentage points lower four years after a flood.[8] Over a longer horizon, there are a number of sectors at risk from continued climate change, notably tourism and agriculture.[9] These risks are further compounded by nature degradation, as climate extremes place further stress on ecosystems already suffering from over-exploitation.[10]

Climate and nature risks are widespread across sectors, with a once-in-a-hundred-years drought event putting a quarter of the euro area’s output at risk.[11] Lower economic activity and higher unemployment in sectors exposed to climate and nature shocks reduce the capacity of businesses and households to repay loans, exposing banks to potential defaults on top of potentially degraded collateral. These risks may also reduce firms’ and households’ access to new bank loans owing to higher credit risks and standards, potentially further weakening investment.[12] Some 75% of all corporate loans in the euro area granted to non-financial corporations are critically dependent on at least one ecosystem service.[13] With these financial consequences in mind, ECB Banking Supervision has engaged extensively with banks since as early as 2020 to ensure that climate and nature-related risks are fully embedded within their governance, strategy and risk management, including in their stress-testing frameworks.[14] While banks have made progress and we are seeing more widespread good practices, more still needs to be done to ensure that banks apply sound practices across all material portfolios, exposures and risk categories.[15]

Benefits of the green transition

Merely managing the risks related to energy insecurity, climate and nature is not enough. By taking action to accelerate the transition to net zero carbon, it is possible to bolster Europe’s resilience to these risks and lessen their economic impact.

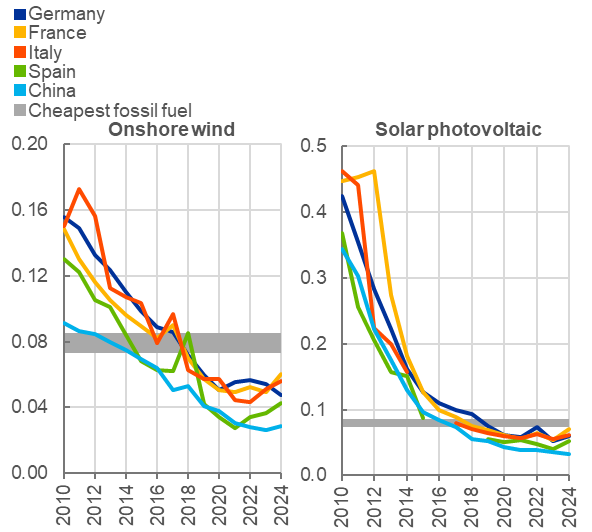

Fortunately, progress in key transition technologies such as wind, solar, batteries and electric vehicles has provided efficient and competitive low-carbon alternatives to fossil fuels. On a levelised cost basis, which takes into account the costs of building, financing and operating a new plant over its projected lifetime, renewable sources of energy are now cheaper than the cheapest fossil fuel equivalent across all major European economies (Chart 3, panel a). Between 2010 and 2024, worldwide total installed costs plummeted – by 87% for solar photovoltaic, by 55% for onshore wind and by 93% for battery energy storage systems. In many regions, batteries are enabling large-scale intra-day transfer, reducing the need for fossil fuels to meet peak demand.

Chart 3

Costs of renewable energy

a) Plummeting costs of renewable sources of electricity | b) Worldwide additions of utility scale renewable electricity |

|---|---|

(2024 USD/kWh, levelised costs) | (gigawatts) |

|  |

Sources: Parker, M. and Rodriguez, S.P. (2026), “Overcoming structural barriers to the green transition”, Economic Bulletin, Issue 1, ECB, based on International Renewable Energy Agency (IRENA).

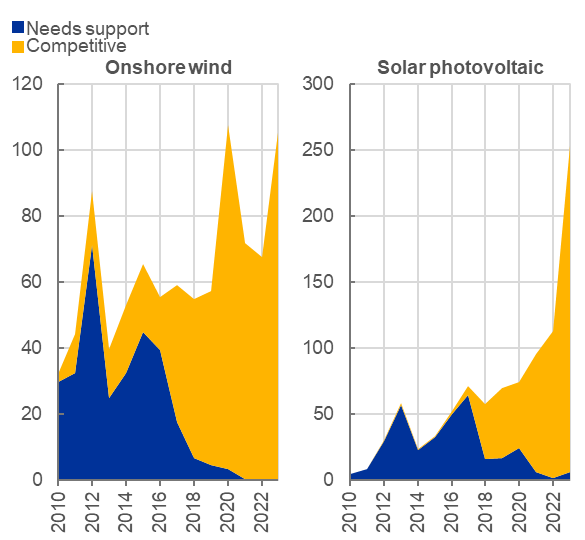

Notes: Panel a) levelised costs incorporate the cost of financing, building and operating a new power plant over the course of its projected lifespan. The fossil fuel range shown in the chart incorporates the worldwide average levelised costs of coal and combined-cycle gas turbines. Panel b) for each year, the project-level levelised cost of electricity generation for newly deployed renewable energy is compared with the counterpart country or regional-weighted average from fossil fuel sources. Where the levelised cost for renewable sources is below that of fossil fuels, the project is labelled competitive, whereas it is labelled as needing support when it is above such levels.

The green transition is starting to bear fruit. While a decade ago renewable energy often required policy support, nearly all renewable capacity now installed is competitive with fossil fuels (Chart 3, panel b). Wholesale electricity prices in Spain are estimated to have already been 40% lower in the first half of 2024 than they would have been if the renewables share of generation had remained at 2019 levels.[16] Higher shares of low-carbon generation cushioned the impact of the Middle East war on electricity prices in several countries – average monthly wholesale prices in Spain and France between March and June this year were less than half those in Italy. Indeed, the passthrough of gas prices to electricity prices in Spain has halved over recent years.[17] According to one study, electric vehicles in Europe avoided 67 million barrels of oil consumption in 2025, lowering oil import costs by €4.1 billion.[18] With higher oil prices and a greater share of electric vehicles, the benefit over the first half of this year is likely to be even greater in comparison. Further afield, as from yesterday some eligible households in Australia started benefiting from free electricity in the middle of the day.[19]

In the longer run, the benefits of a worldwide transition to net zero carbon in terms of climate damage avoided far outweigh the costs of the transition.[20] For Europe, lower reliance on imported fossil fuels boosts our energy security and limits one of the main causes of inflation volatility.[21] And the benefits of a transition go beyond pure economics. The European Environmental Agency estimates that 182,000 deaths in 2023 were attributable to exposure to air pollution above the World Health Organisation’s guidelines. While still far too high, that number fell by 57% between 2005 and 2023 as particulate emissions from heating, electricity generation and transport fell. If the annual rate of premature deaths over the entire period had been at the current rate, 2.2 million fewer Europeans would have died prematurely – equivalent to the population of Greater Lisbon.

Barriers to the green transition

Given these benefits, the obvious question is: why hasn’t Europe made faster progress? The short answer is that there are a range of economic, financial and institutional barriers that reinforce each other, hampering progress. There are costs in the near term which still need to be paid, even if these are vastly outweighed by the longer-term benefits. I will now outline some of the major barriers to the green transition and what policymakers can do to swiftly and decisively alleviate them. Just as these barriers reinforce each other, so do the policies designed to break them down. Implementing an array of policies to jointly address the various barriers to the transition will be far more effective than a few isolated policies.

Of course, that will require many different actors to play their role. Central banks are not climate and nature policymakers, but climate and nature policy takers. We operate within the context of the policy decisions taken by those who are policymakers in these fields. As I have already illustrated, overcoming the barriers to the transition diminishes key sources of inflation volatility, in turn helping us to deliver our price stability mandate.

Barrier one: insufficient pricing of carbon emissions

The first such barrier is the uneven playing field and unfair competitive advantage derived by carbon-intensive firms from explicit fossil fuel subsidies and the implicit subsidy of unpriced carbon emissions. Burning fossil fuels worsens climate change globally and causes air pollution locally. If high emitting firms do not pay for the externality – the costs resulting from that environmental and economic damage – they are in effect receiving an implicit subsidy relative to low-emission firms. The size of that subsidy is staggering, estimated by the International Monetary Fund to have totalled USD 6.7 trillion in 2025, just under 6% of world GDP.[22] While the implicit subsidy in the EU is smaller due to the existence of carbon pricing, notably the EU Emissions Trading System (ETS), it still reached an estimated 0.7% of GDP. Further EU progress on pricing carbon emissions is expected via the introduction of ETS2, covering buildings, road transport and smaller industries, in 2028.

Naturally, incumbent firms are reluctant to give up the subsidy that helps to protect them from new competitors using low-carbon technology, and consequently lobby to water down the ETS. But that punishes firms who have made progress in decarbonising their operations and generates further uncertainty. It is essential for the EU to preserve the ETS as a credible, market‑based instrument for carbon pricing. By the same token, the carbon border adjustment mechanism is necessary to protect European businesses from the greater rate of implicit subsidy prevalent in the rest of the world.

Barrier two: regulatory uncertainty and complexity

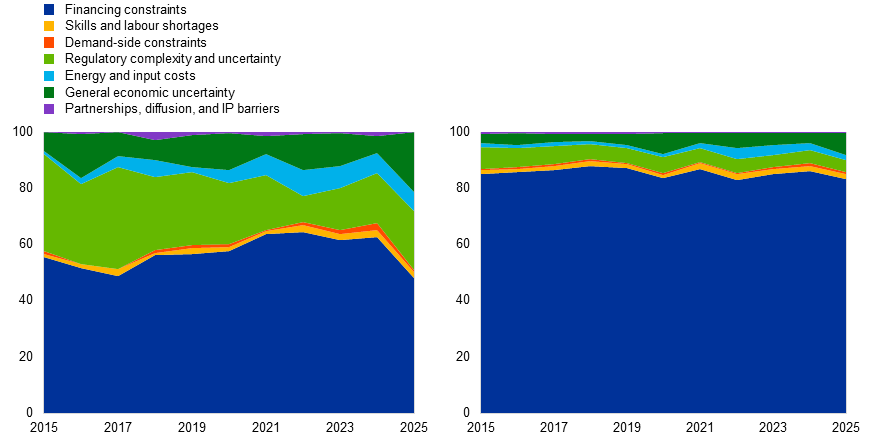

Even with carbon pricing levelling the playing field, the estimated additional investment needs for the transition in the EU are massive – between 2.7% and 3.7% of EU GDP each year until 2030 – and will likely be greater still beyond that date.[23] Yet investing in new technologies tends to be riskier than investing in marginal improvements of existing technologies. As a result, the factors that companies cite as barriers to green investment differ in importance from barriers to investment in general. Chart 4 compares the factors mentioned as barriers to investment in earnings calls to investors made by large European businesses, distinguishing between green investment in panel a) and all types of investment in panel b). As you can see, regulatory uncertainty and complexity, as well as general economic uncertainty, are much larger barriers to green investment than they are for all types of investment. That is why it is important to lay out a clear path forward with regulation; frequently changing regulations and backtracking on agreed targets and dates generates regulatory uncertainty and hinders green investment.

Chart 4

Barriers to green investment and all investment perceived by firms

a) Green investment | b) All investment |

Sources: Parker, M. and Rodrigues, C. (2026), “Overcoming structural barriers to the green transition”, Economic Bulletin, Issue 1, ECB, based on NL Analytics and ECB staff calculations.

Notes: Panel a): The contribution of each barrier is measured as the average number of sentences in earnings calls containing at least one term related to the barrier and one term related to green investment. Panel b): The contribution of each barrier is measured as the average number of sentences in earnings calls containing at least one term related to the barrier and one term related to investment. The data cover 17 EU countries (Belgium, Denmark, Germany, Ireland, Greece, Spain, France, Italy, Cyprus, Luxembourg, Netherlands, Austria, Poland, Portugal, Romania, Finland and Sweden) from 1 January 2015 to 31 December 2025.

New technologies require scale to lower costs and become competitive. A major impediment to European companies growing is the incomplete Single Market, which is fragmented by a plethora of national regulations. Replacing 27 national sets of regulations with a common, single European standard would reduce the regulatory burden faced by firms trying to expand. Similarly, tackling the time and costs required to grant permits for renewable energy projects will also boost investment in new capacity. Following a series of reforms in Germany in 2023 and 2024, the average time taken to grant a permit for onshore wind projects dropped from 25.6 months in 2023 to 16.8 months in 2025, while newly permitted capacity almost tripled from 7.6 gigawatts (GW) to a record 20.8 GW over the same period.[24] Further progress in reducing permit processing times would help speed up the green transition and structural change more generally.

That is not to say that regulation is a bad thing. Regulations have been put in place over time to help achieve a range of societal goals, including health and long-run environmental viability. Regulations can help address a range of market failures, such as asymmetric information, externalities and market power, all of which lead to sub-optimal outcomes. Within the EU, regulatory quality has been shown to be positively correlated with investment in high-technology sectors, including AI-intensive industries.[25] Having the right regulatory framework helps Europe stay competitive. And that matters for central banks. Low growth and loss of competitiveness can increase inflationary pressures and reduce the space for monetary policy to manoeuvre.[26] Losing competitiveness can also increase unemployment and bankruptcies, resulting in higher default rates on bank loans.

With these benefits of regulation in mind, it is important to distinguish between regulatory simplification and deregulation. Simplification is a process of ensuring that regulations deliver on their societal aims while minimising the costs of doing so. Deregulation may lower some costs in the short term, but at the expense of generating other social and economic costs over longer time horizons. Nature degradation, for example, carries the risk of massive costs to the economy and to human health. It is important, then, to find the right balance between conflicting societal goals and to ensure that regulation delivers that balance appropriately.

Barrier three: access to finance

Another frequently cited barrier to green investment is access to finance. Because green technologies, like all new technologies, are risky, equity and venture capital may be better placed to finance the early stages. Indeed, there is evidence that countries with deeper capital markets decarbonise faster.[27] Yet this is an area where Europe lags behind other regions of the world. Making swift progress on the savings and investments union is crucial to unlocking the finance necessary for technological progress, green and otherwise. Integrated capital markets give households better opportunities to build wealth, while helping firms finance growth. Deeper and more sophisticated equity and venture capital markets would help innovative EU firms gain access to risk capital and expand within Europe. Well-designed savings products would also incentivise households to channel savings away from low-return deposits towards longer-run, higher-return investments in the EU.

Given the importance of finance, the role of the ECB often comes into focus. Green technologies regularly involve substantial upfront capital spending, making their long-run profitability particularly sensitive to changing financing conditions over the life of the project. So, I would like to take a few moments to consider the evidence on what is happening to the credit conditions faced by green firms.[28]

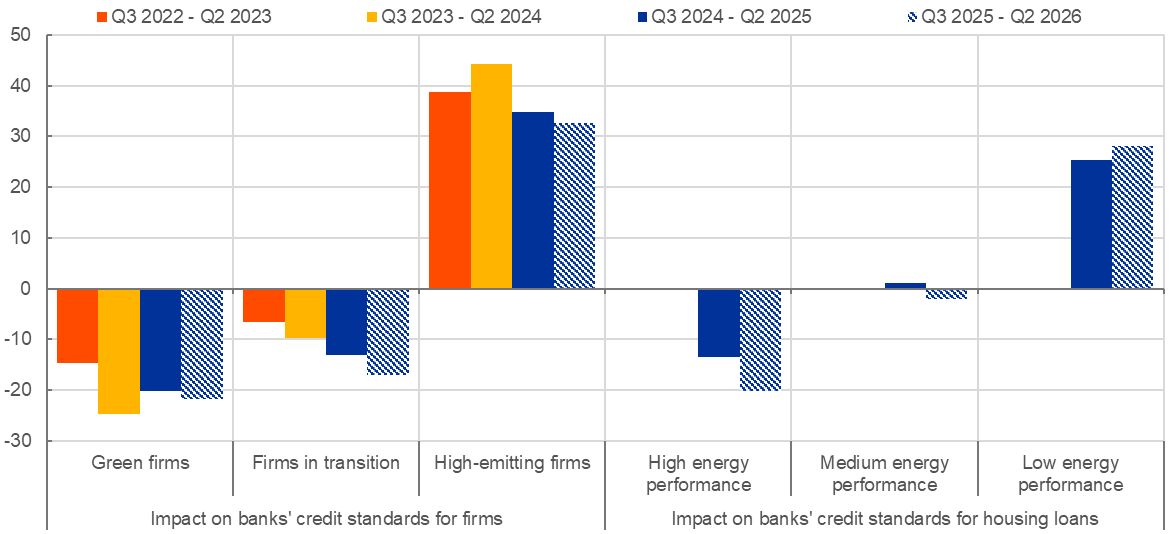

Since the Paris Agreement, and since ECB Banking Supervision started focusing on how banks are managing climate and nature risks, it appears that banks have been increasingly differentiating between companies based on their carbon emissions. Low-emission companies, and those with credible transition plans to reduce their emissions, benefit from more favourable lending conditions compared with higher-emission firms without credible transition plans (Chart 5). A similar dynamic is visible for housing loans, where households investing in energy efficient houses tend to enjoy more favourable credit conditions.

Chart 5

Impact of climate change on banks’ credit standards

(net percentages of banks; over the past 12 months and the next 12 months)

Sources: ECB Bank Lending Survey and Köhler-Ulbrich, P., Schuster Y. and Tushteva, N. (2025), "Climate performance matters for bank credit in the euro area", The ECB Blog, ECB, 10 November.

Notes: Net percentages are defined as the difference between the percentages of banks responding “contributed considerably/somewhat to tightening” and the percentages of banks responding “contributed somewhat/considerably to easing”. The striped bars denote expectations indicated by banks in the latest round.

Using comprehensive loan-level data for the euro area, research has similarly identified lower lending rates for greener firms and those in transition.[29] So in a practical sense, dual lending rates already exist in the euro area. Moreover, these comprehensive data show that the impact of higher policy rates on lending is milder for low-emission firms, in terms of both credit standards and loan volumes, while banks expand the climate credit risk premium more for high-emission firms in response to monetary policy tightening.[30] Other recent evidence finds that the stock prices of high-emission firms are also more affected by increases in policy rates.[31]

More broadly on financing conditions, long-run interest rates – which are crucial for investment spending – are comprised of three main factors: expectations of future real interest rates, average expected inflation and a risk premium. If the central bank fails to act against inflationary pressures in good time, economic agents may start to doubt its commitment to its inflation target. Lower monetary policy credibility leads to higher inflation expectations and risk premia, pushing up long-run interest rates.

So from the perspective of the green economy too, maintaining price stability is the most valuable contribution a central bank can make. Moreover, by continuing to credibly deliver on its mandate for price stability, the ECB helps reduce general economic uncertainty, which, as I showed earlier, is a greater barrier to green investment than to other types of investment.

Barrier four: visible upfront costs and invisible benefits

The last barrier to the green transition that I wish to highlight today concerns the question of who bears the visible upfront costs, particularly when the principal benefit – future climate damage avoided – is invisible: a classic public goods problem. Building political momentum involves distributing the benefits and ensuring that the burden of costs does not fall disproportionately on certain sectors or households. Yet even the tangible benefits that already exist today have not always reached households.

Take the lower electricity generation costs that come from renewable sources of electricity. Higher system costs have slowed the pass-through of lower wholesale costs of electricity generation to residential customers. These system costs currently include paying legacy fossil fuel plants to stand idle in case of need and paying renewables to curtail the generation of almost free electricity. Investment in grid infrastructure has lagged behind the increase in potential renewable capacity, resulting in long waiting times for connections, and the costs of those upgrades that have been completed have fallen on current consumers.

Several concurrent steps are required to lower household electricity bills. Electricity needs to move efficiently from where it can be cheaply made to where it is needed. That requires upgrades to continent-wide grid infrastructure, greater use of battery storage and improved use of technology to balance the grid. Achieving a genuine European Energy Union by considering the challenge from a continental perspective would help deliver greater energy security and lower electricity bills for all.[32]

But the demand side also requires attention. Specifically, greater demand flexibility can help balance the grid, too. Of course, this requires a faster rollout of smart meters to reward consumers for beneficial behaviour. Moreover, increasing electricity demand helps spread the costs of new grid infrastructure over more units of electricity, reducing its average cost. Policies that encourage the take-up of electric vehicles and heat pumps can enable households to switch to energy sources that are cheaper over the long run. These cost savings in turn help bolster support for the transition. At the same time, consistent and growing demand provides profitable opportunities and hence incentives for businesses to invest in these new technologies, supporting their own transition and overall economic activity.

More generally, putting in place a consistent set of policies that complement each other to support the transition enables households and companies across Europe to synchronise their actions. By minimising disjointed actions and economic frictions, an orderly green transition can minimise the overall costs and hence maximise the net benefit of reaching net zero carbon.

I believe there is an important role here for academia. Research that helps to quantify the range of economic and social costs of the climate and nature crises can improve public perceptions of the benefits of actions to accelerate the transition. Similarly, academics possess the tools to establish the true counterfactuals which are needed to properly assess the benefits of individual policies. I strongly encourage the academic community to engage with policymakers, businesses and households to create further momentum in greening the economy.

Conclusions

Let me conclude.

Accelerating the green transition provides substantial economic, environmental and social benefits. Eliminating Europe’s dependence on imported fossil fuels removes a source of economic volatility whose negative effects have been all too visible in recent years. It also reduces the extent of future climate change. Reducing the future impact of these two sources of shock will help lower future inflation volatility and aid the delivery of price stability.

Importantly, the economic benefits are much broader. Simply put, the green transition is a technological transformation of the economy, requiring innovation and the adoption of new technologies. Steps to swiftly complete the Single Market and the savings and investments union also ease the uptake of other new technologies, such as digitalisation and artificial intelligence. In the context of ongoing structural trends, including an ageing population, the adoption of new, more productive technologies is vital to maintaining Europe’s standard of living.

Gareis, J. (2026), “Higher oil prices from the war in the Middle East: assessing the headwinds for euro area growth”, Economic Bulletin, Issue 4, ECB.

Anaya Longaric, P., Kostakis, V., Parisi, L. and Vinci, F. (2025) “Oil shocks and firm investment on the two sides of the Atlantic”, Working Paper Series, No 3116, ECB.

Kotz, M., Donat, M.G., Lancaster, T., Parker, M., Smith, P., Taylor A. and Vetter, S.H. (2025),“Climate extremes, food price spikes, and their wider societal risks”, Environmental Research Letters, Vol. 20, July.

Bates, C., Kuik, F., Wieland, E. and Zekaite, Z. (2025), “Inside the food basket: what is behind recent food inflation?”, Economic Bulletin, Issue 8, ECB. See also NGFS (2026), NGFS Note on the economic and financial impacts of extreme weather events, for further examples of impacts of extreme events on food prices.

Kotz, M., Kuik, F., Lis, E. and Nickel, C. (2024), “Global warming and heat extremes to enhance inflationary pressures”, Communications Earth & Environment, Vol. 5, No 116.

Wegner, O., Dees, S., Boitout, A., Boullot, M., Gabet, M., Lesterquy, P., Serfaty, C., Thubin, C., and Ulgazi, Y. (2025), “Seeds of inflation: macro modelling of nature-related risks through agricultural prices”, Working Paper, No 1006, Banque de France.

European Environment Agency (2025), Economic losses from weather- and climate-related extremes in Europe, 14 October.

Usman, S., González-Torres Fernández, G. and Parker, M. (2025), “Going NUTS: the regional impact of extreme climate events over the medium term”, European Economic Review, Vol. 178. See also Andersson, M., Battistini, N. and Bobasu, A. (2026), “Heatwaves, coldwaves, floods, and droughts: the short-term impact of extreme weather events on economic activity”, Working Paper Series, No 3203, ECB, for a detailed analysis of short-term sectoral impacts of these events.

See Parker, M. (2023), “How climate change affects potential output”, Economic Bulletin, Issue 6, ECB for a more detailed discussion of how climate change affects output over the long run.

Ceglar, A., Parker, M., Pasqua, C., Boldrini, S., Gabet, M. and van der Zwaag, S. (2024), “Economic and financial impacts of nature degradation and biodiversity loss”, Economic Bulletin, Issue 6, ECB.

Ceglar, A. et al. (2025), “Nature at risk: Implications for the euro area economy and financial stability”, Occasional Paper Series, No 380, ECB.

See Köhler-Ulbrich, P., Schuster, Y. and Tushteva, N. (2025), “Climate performance matters for bank credit in the euro area”, The ECB Blog, November.

Boldrini, S., Ceglar, A., Lelli, C., Parisi, L. and Heemskerk, I. (2023), “Living in a world of disappearing nature: physical risk and the implications for financial stability”, Occasional Paper Series, No 333, ECB.

ECB (2020), Guide on climate-related and environmental risks. Supervisory expectations relating to risk management and disclosure, November.

Elderson, F. (2026), “Good practices for advancing climate and nature-related risk management”, The Supervision Blog, ECB.

Quintana, J. (2024), “The impact of renewable energies on wholesale electricity prices”, Economic Bulletin, Banco de España, September.

Box 1.3 in Banco de España (2026), Annual Report 2025.

EMBER Energy (2026), A clean break: leaving fossil volatility for clean tech security.

Australian Government, Solar Sharer Offer.

See, for example, Alogoskoufis, S. et al. (2021), “ECB economy-wide climate stress test”, Occasional Paper Series, No 281, ECB; IPCC (2022), “Climate Change 2022: Mitigation of Climate Change”, Report of Working Group III, IPCC Sixth Assessment Report; NGFS (2024), NGFS Climate Scenarios for central banks and supervisors - Phase V.

See Domínguez-Díaz, R. and Hurtado, S. (2024), “Green energy transition and vulnerability to external shocks”, Working Papers, No 2425, Banco de España and Section 3.3 in Nickel et al. (2025), A strategic view on the economic and inflation environment in the euro area, Occasional Paper Series, No 371, ECB; Chafwehé, B., Colciago, A. and Priftis, R. (2025), “Reallocation, productivity, and monetary policy in an energy crisis”, European Economic Review, Vol. 173(C).

Black, S., Celniak, W., Garcia Huitron, A., Parry, I., Schulz Antipa, P. and Vernon-Lin, N. (2025), “ Underpriced and Overused: Fossil Fuel Subsidies Data 2025 Update”, IMF Working Paper, 2025/270. The International Monetary Fund calculates explicit subsidies based on the estimated monetary value of the untaxed environmental impact of burning fossil fuels, both in terms of climate change and local air pollution.

Nerlich et al. (2025), “Investing in Europe’s green future – Green investment needs, outlook and obstacles to funding the gap”, Occasional Paper Series, No 367, ECB.

FA Wind und Solar (2026), Status of Onshore Wind Energy Development in Germany in the Year 2025.

Bothner, J., Lopez-Garcia, P., Momferatou, D. and Setzer, R. (2026), “Why is Europe lagging behind in high tech sectors? The role of institutional and regulatory quality”, Working Paper Series, No 3185, ECB.

Filip, M.-D., Momferatou, D. and Parraga-Rodriguez, S. (2025), “Why a more competitive economy matters for monetary policy”, The ECB Blog, ECB, 11 February.

De Haas, R. and Popov, A. (2023), “Finance and green growth”, The Economic Journal, Vol. 133, No 650, pp. 637-668.

For a more detailed discussion of credit conditions and the implications for the transmission of monetary policy, see Lane, P. (2026), “Climate change and monetary policy”, Keynote Speech at the Climate, Nature and Monetary Policy Conference, 5 May.

Altavilla, C., Boucinha, M., Pagano, M. and Polo, A. (2024), “Climate risk, bank lending and monetary policy”, Working Paper Series, No 2969, ECB.

Banks do indeed respond to monetary policy tightening by increasing monitoring efforts and restricting lending to riskier borrowers, but the dimensions of risk taken into consideration also now include those related to climate.

Bauer, M., Offner, E.A. and Rudebusch, G.D. (2025), “Green stocks and monetary policy shocks: Evidence from Europe”, European Economic Review, Vol. 177.

Grynberg, C., Vinci, F. and De Sanctis, A. (2026), “Energy security and industrial competitiveness: the case for a European Energy Union”, Occasional Paper Series, No 388, ECB.

Den Europæiske Centralbank

Generaldirektoratet Kommunikation

- Sonnemannstrasse 20

- 60314 Frankfurt am Main, Tyskland

- +49 69 1344 7455

- media@ecb.europa.eu

Eftertryk tilladt med kildeangivelse.

Pressekontakt