- PRESS RELEASE

ECB publishes supervisory banking statistics for the second quarter of 2021

6 October 2021

- Aggregate Common Equity Tier 1 ratio stood at 15.60% in second quarter of 2021, up from 15.49% in previous quarter

- Aggregate non-performing loans ratio fell further to 2.32% (down from 2.54% in previous quarter), with stock of non-performing loans declining to €422 billion (down from €455 billion in previous quarter)

- Aggregated annualised return on equity stood at 6.92% (compared with 7.21% in first quarter of 2021, and up from 0.01% one year ago)

- The aggregate loan-to-deposit ratio decreased further to 104.74% in second quarter of 2021, down from 106.07% in previous quarter, despite second consecutive quarter-to-quarter increase in loans and advances to non-financial corporations and households

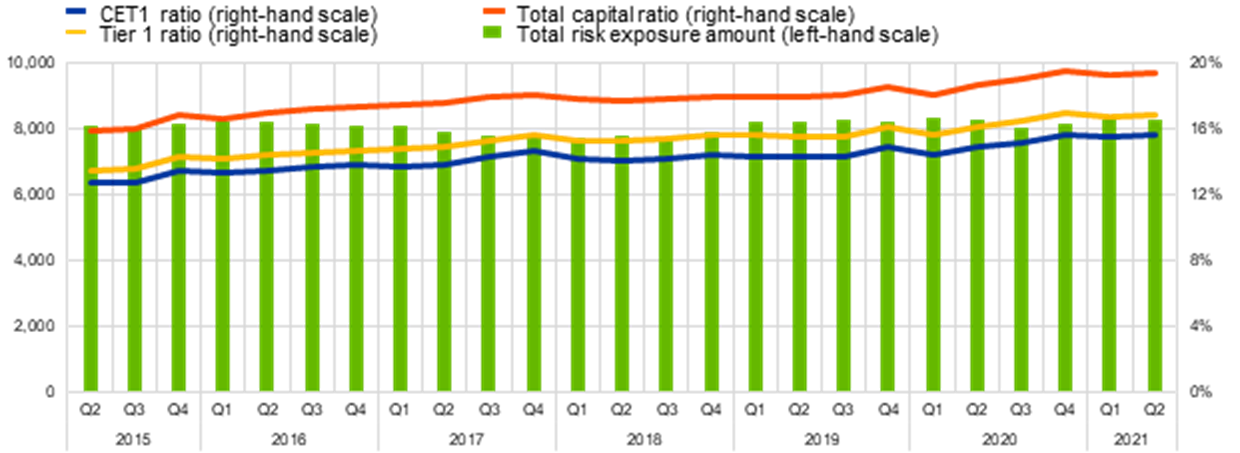

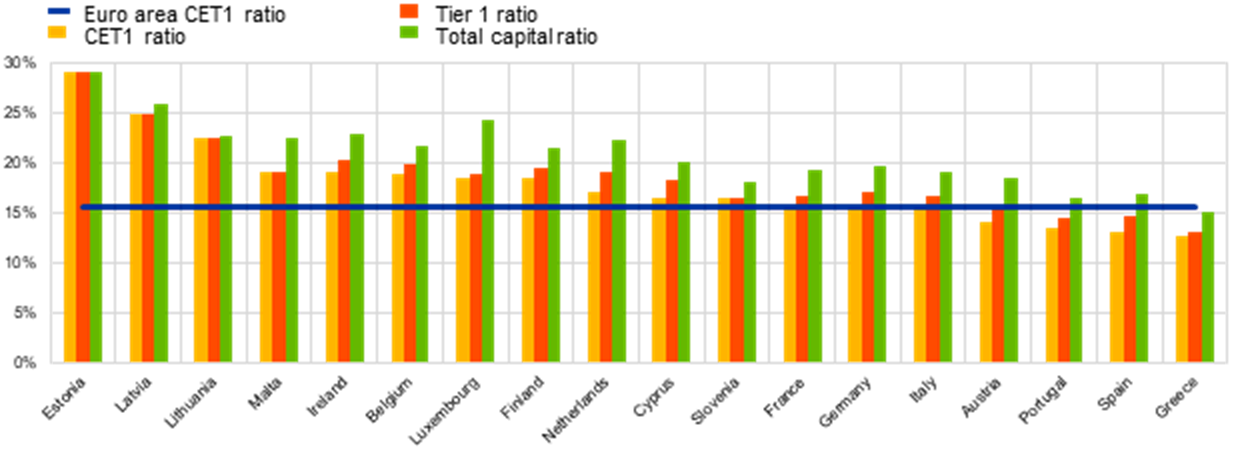

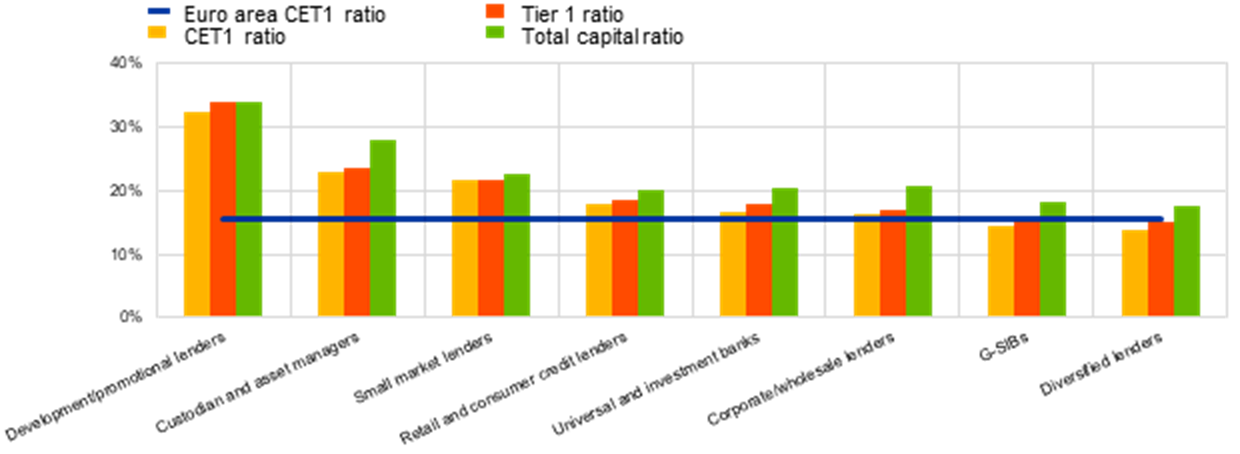

Capital adequacy

The aggregate capital ratios of significant institutions (i.e. banks that are supervised directly by the ECB) increased slightly in the second quarter of 2021. The aggregate Common Equity Tier 1 (CET1) ratio stood at 15.60%, the aggregate Tier 1 ratio stood at 16.87% and the aggregate total capital ratio stood at 19.41%. Aggregate CET1 ratios at the country level ranged from 12.66% in Greece to 29.26% in Estonia. Across Single Supervisory Mechanism business model categories, diversified lenders reported the lowest aggregate CET1 ratio (13.91%) and development/promotional lenders reported the highest (32.55%).

Chart 1

Capital ratios and their components by reference period

(EUR billions; percentages)

Source: ECB.

Chart 2

Capital ratios by country for the second quarter of 2021

(percentages)

Source: ECB.

Note: Some countries participating in European banking supervision are not included in this chart, either for confidentiality reasons or because there are no significant institutions at the highest level of consolidation in that country.

Chart 3

Capital ratios by business model for the second quarter of 2021

(percentages)

Source: ECB.

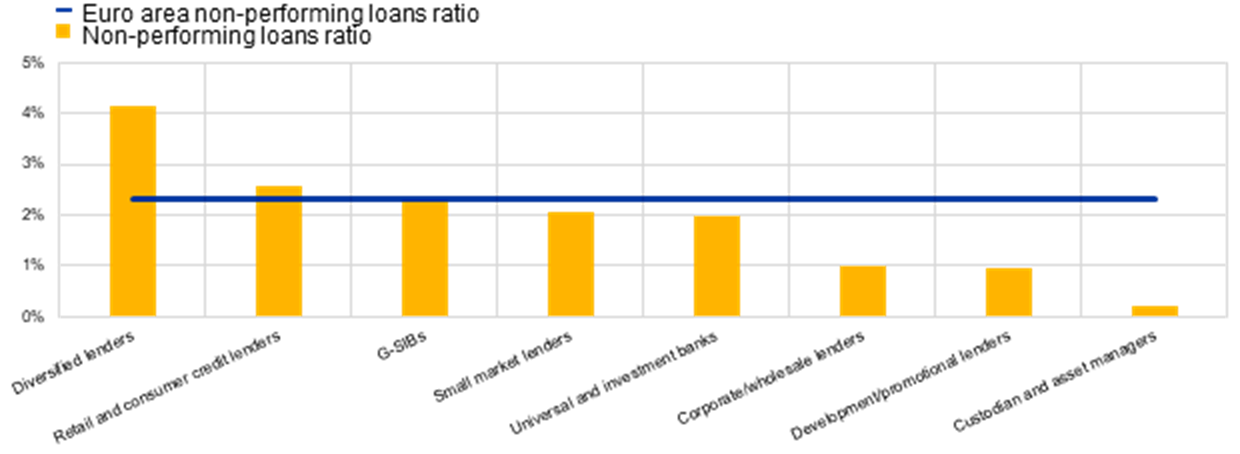

Note: G-SIBs stands for global systemically important banks.

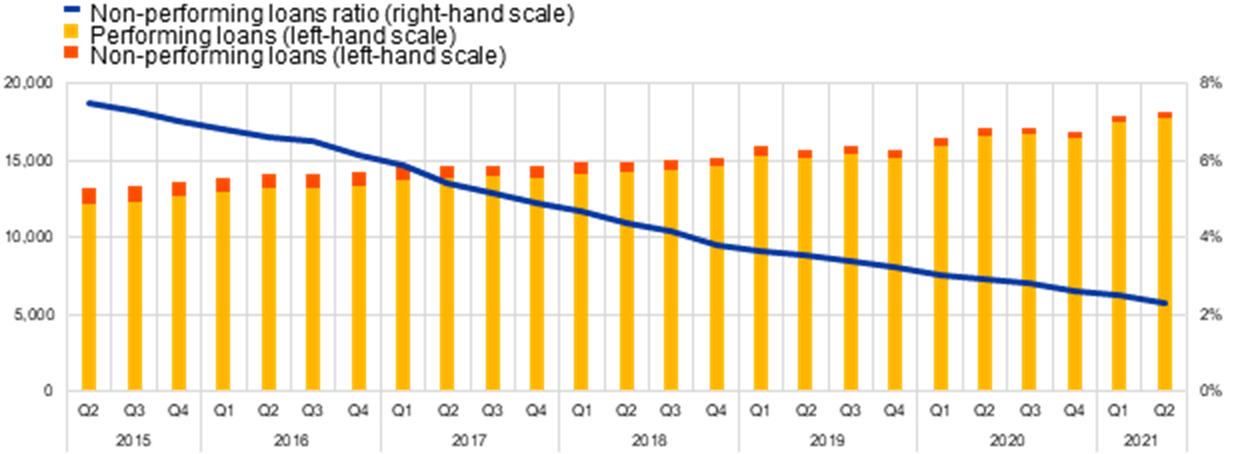

Asset quality

The aggregate non-performing loans (NPL) ratio decreased further to 2.32% in the second quarter of 2021, the lowest level recorded since supervisory banking statistics were first published in the second quarter of 2015. The decrease was driven by the combination of a declining stock of NPLs and an increase in the stock of total loans. At the country level, the average NPL ratio ranged from 0.68% in Luxembourg to 14.84% in Greece. Across business model categories, custodians and asset managers reported the lowest aggregate NPL ratio (0.22%) and diversified lenders reported the highest (4.16%).

Chart 4

Non-performing loans by reference period

(EUR billions; percentages)

Source: ECB.

Chart 5

Non-performing loans ratio by country for the second quarter of 2021

(percentages)

Source: ECB.

Note: Some countries participating in European banking supervision are not included in this chart, either for confidentiality reasons or because there are no significant institutions at the highest level of consolidation in that country.

Chart 6

Non-performing loans ratio by business model for the second quarter of 2021

(percentages)

Source: ECB.

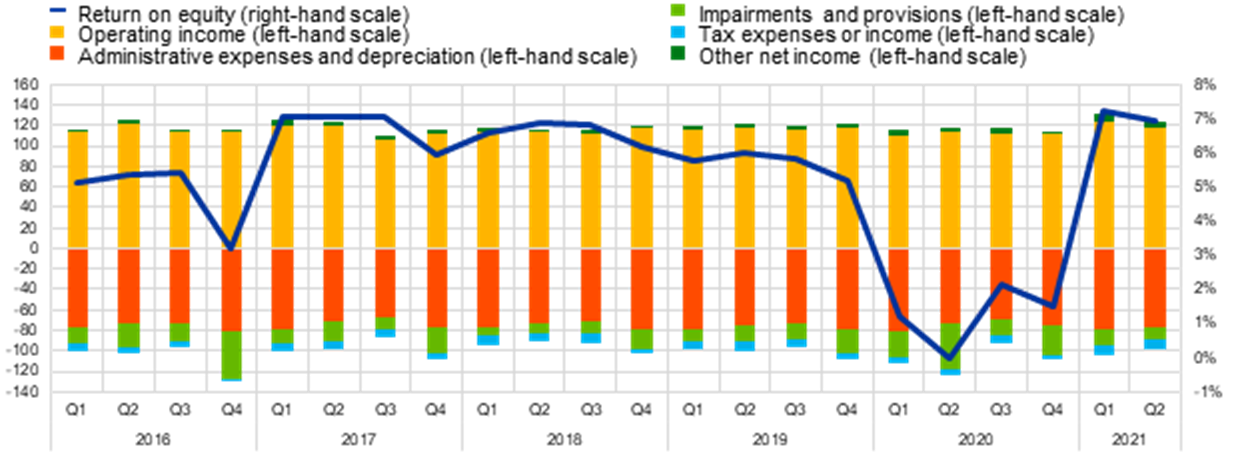

Return on equity

The aggregated annualised return on equity stood at 6.92% (compared with 7.21% in the first quarter of 2021, and up from 0.01% one year ago). Compared with the first quarter of 2021, the generation of operating income slowed (€118 billion in the second quarter of 2021, down from €123 billion). Nevertheless, the aggregate return-on-equity levels of significant institutions continued to be well above 2020 levels.

Chart 7

Return on equity and composition of net profit and loss by reference period

(EUR billions; percentages)

Source: ECB.

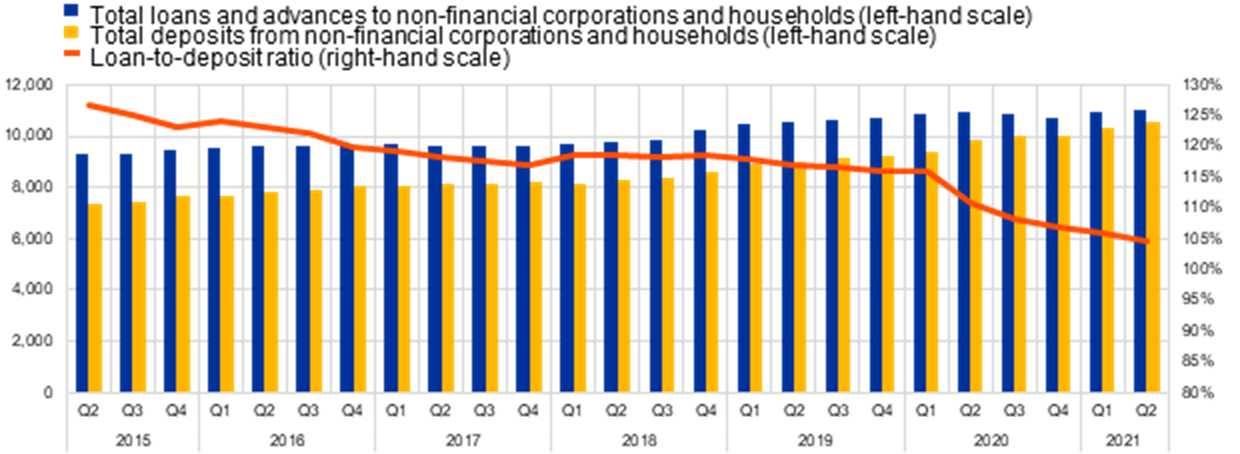

Funding

The aggregate loan-to-deposit ratio decreased to 104.74% in the second quarter of 2021, down from 106.07% in the previous quarter. The second consecutive quarter-to-quarter increase in loans and advances to non-financial corporations and households (+€41 billion compared with the first quarter of 2021) was overcompensated by another significant increase in deposits from non-financial corporations and households (+€170 billion compared with the first quarter of 2021).

Chart 8

Loan-to-deposit ratio by reference period

(EUR billions; percentages)

Source: ECB.

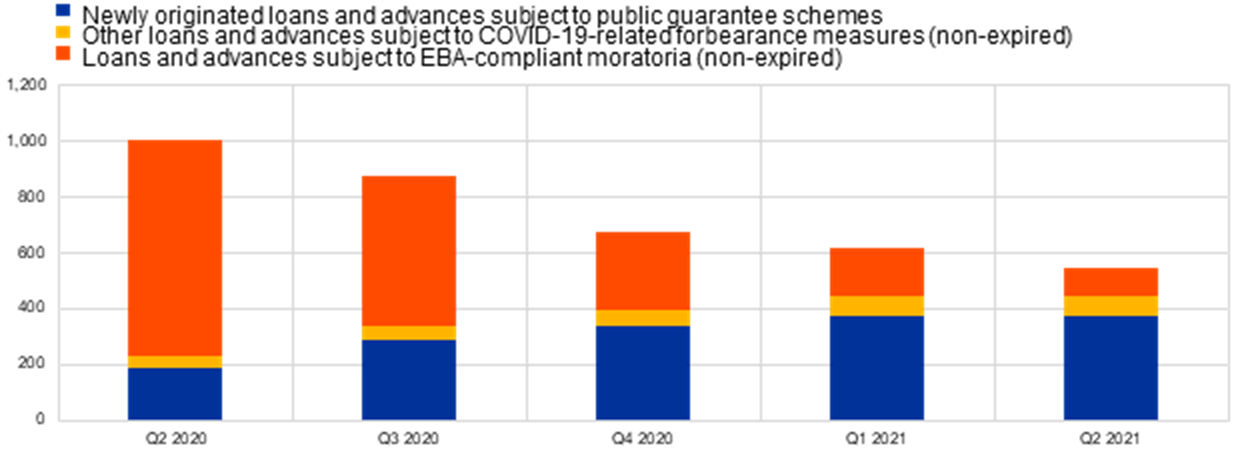

Loans and advances subject to COVID-19-related measures

In the second quarter of 2021 the total loans and advances subject to COVID-19-related measures decreased to €548 billion, from €619 billion in the previous quarter. The decrease was driven by loans and advances subject to non-expired European Banking Authority-compliant moratoria, which declined to €101 billion from €178 billion in the first quarter of 2021.

Chart 9

Loans and advances subject to COVID-19-related measures by reference period

(EUR billions)

Source: ECB.

Factors affecting changes

Supervisory banking statistics are calculated by aggregating the data that are reported by banks which report COREP (capital adequacy information) and FINREP (financial information) at the relevant point in time. Consequently, changes from one quarter to the next can be influenced by the following factors:

- changes in the sample of reporting institutions;

- mergers and acquisitions;

- reclassifications (e.g. portfolio shifts as a result of certain assets being reclassified from one accounting portfolio to another).

For media queries, please contact Philippe Rispal, tel.: +49 69 1344 5482.

Notes

- The complete set of Supervisory banking statistics with additional quantitative risk indicators is available on the ECB’s banking supervision website.

Europeiska centralbanken

Generaldirektorat Kommunikation och språktjänster

- Sonnemannstrasse 20

- 60314 Frankfurt am Main, Tyskland

- +49 69 1344 7455

- media@ecb.europa.eu

Texten får återges om källan anges.

Kontakt för media