- THE SUPERVISION BLOG

Our supervisory priorities for a healthier banking sector after the pandemic

Blog post by Andrea Enria, Chair of the ECB’s Supervisory Board and Mario Quagliariello, Director of Supervisory Strategy and Risk

Frankfurt am Main, 7 December 2021

ECB Banking Supervision has today published the SSM Supervisory Priorities for 2022-2024.

In this blog post, we look at the concrete areas we want to focus on over the next three years to ensure that banks: (1) emerge from the pandemic healthy, (2) seize the opportunity to address structural weaknesses through digitalisation strategies and enhanced governance, and (3) tackle emerging risks, including climate-related and environmental risks, IT and cyber risks.

Credit risk remains high on our agenda as we exit the pandemic

Our first priority is to ensure that supervised banks emerge healthy from the coronavirus (COVID-19) pandemic. Banks have proven resilient so far, also owing to unprecedented public support. While our initial expectations on asset quality might have been overly pessimistic, we remain convinced that caution is needed in monitoring and managing credit risk.

A possible deterioration in asset quality, linked to the progressive withdrawal of public support measures along with downside risks to the economic recovery, calls for supervisory attention.

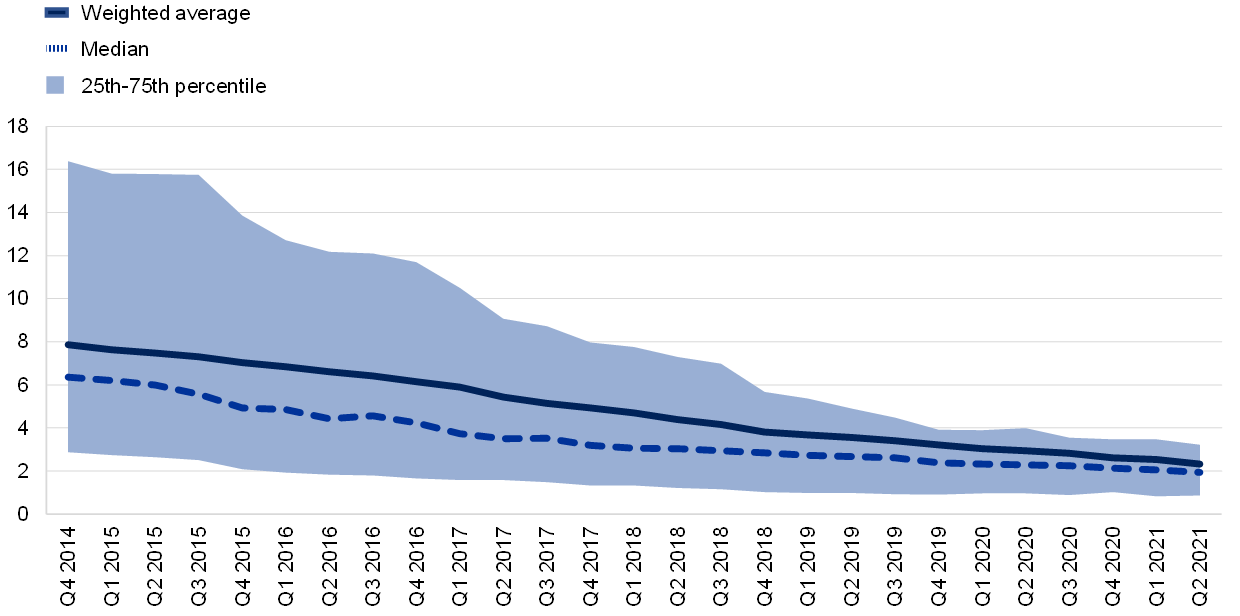

At first glance, the dynamic of the aggregate non-performing loan (NPL) ratio of banks under European banking supervision provides grounds for optimism. The ratio fell from 3.1% in March 2020 to 2.3% in June 2021 (Chart 1), with a drop of nearly €80 billion in NPL volumes.

Chart 1:

Gross NPL ratio – evolution in the banking union

(percentages)

Source: ECB and ECB staff calculations.

Note: Changing sample of all significant institutions at the highest level of consolidation within the Single Supervisory Mechanism (SSM).

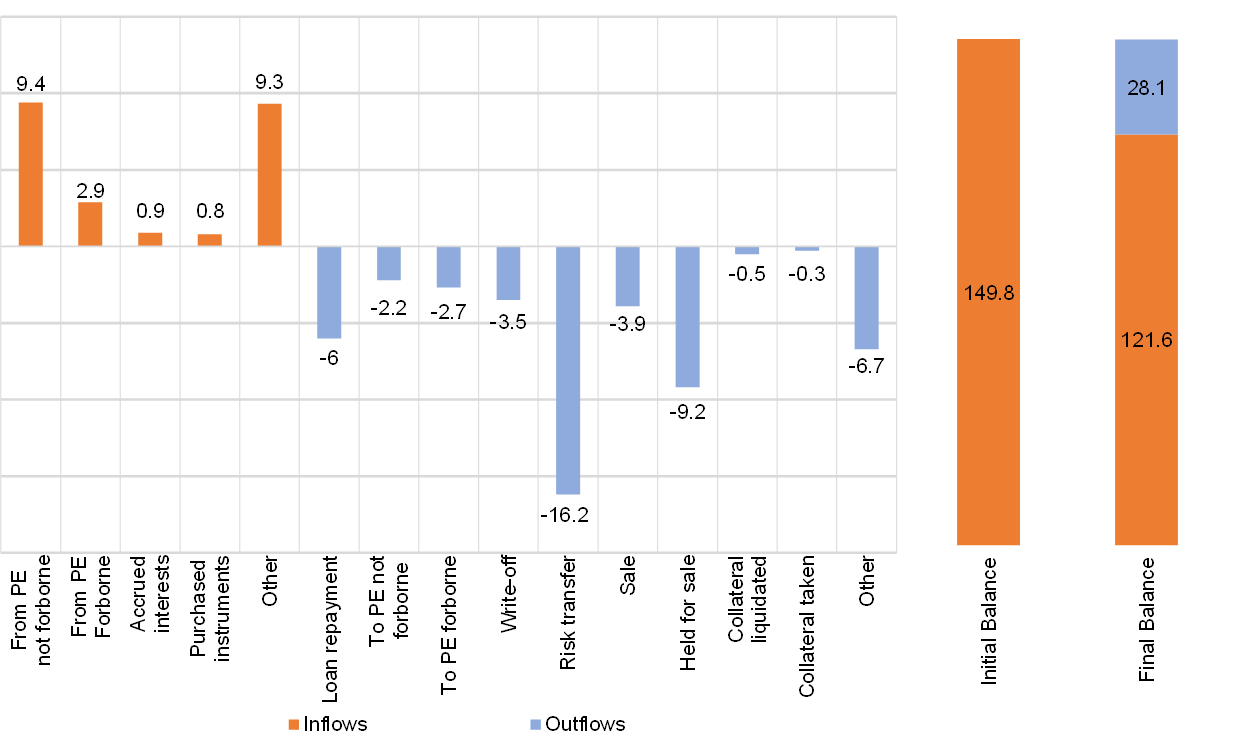

Similarly, it is encouraging that high-NPL banks, which are institutions with a large legacy of NPLs from the last financial crisis, have managed to successfully reduce their stock of legacy assets through risk transfers, sales, and loan repayments (Chart 2).

Chart 2:

Flows for high-NPL banks in the first half of 2021

€ billions

Source: ECB staff calculations.

Note: PE stands for performing exposures.

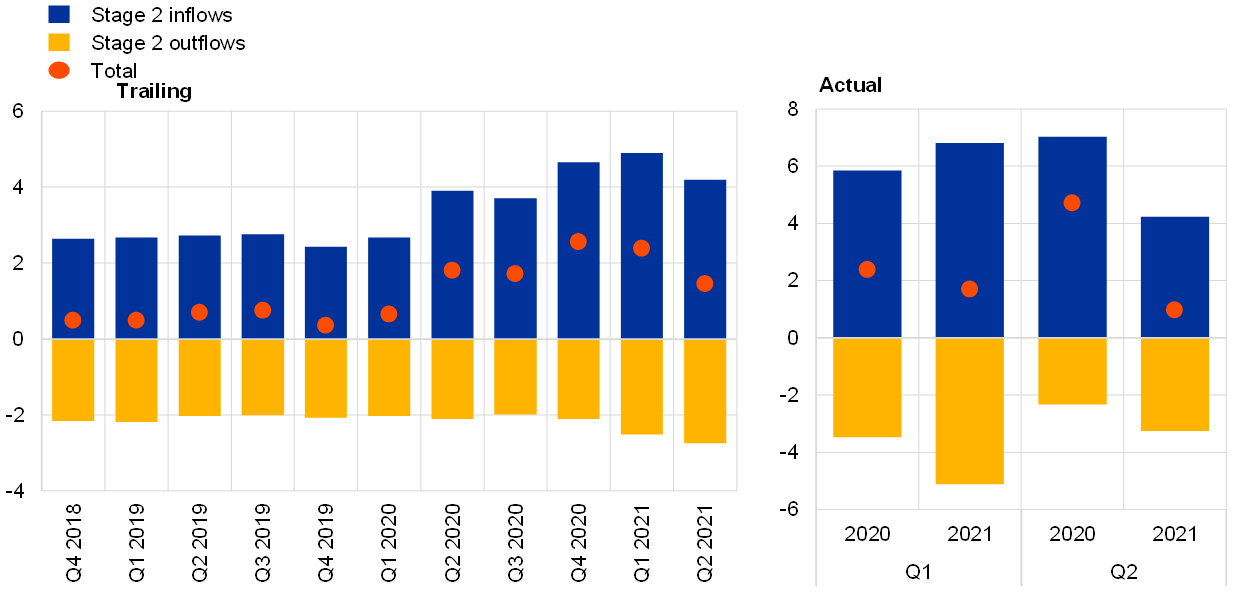

However, several early indicators point to potential asset quality deterioration in the future. For example, inflows of Stage 2 loans, which are loans characterized by a significant increase in credit risk, have risen during the pandemic. Although this inflow slows down during the second quarter of 2021, it remains twice as high as pre-pandemic levels (Chart 3). The percentage of total forborne loans also increased from 2.4% in the second quarter of 2020 to 2.7% one year later. In addition, while loans under moratoria only account for 0.7% of total loans during the second quarter of 2021, they tend to be riskier and could possibly turn into non-performing status.

NPL ratios in sectors more vulnerable to the impact of the pandemic have also started increasing. This is especially noticeable in accommodation and food services, and the air transport and travel-related sectors.

Chart 3:

Loan inflows to and outflows from IFRS Stage 2 assets

(percentages of total loans)

Source: ECB Financial Stability Review November 2021 – ECB and ECB staff calculations.

Note: Based on a balanced sample of 92 significant institutions. Left chart: the total refers to the difference between actual inflows and outflows as observed in the trailing four quarters and is expressed as a share of total loans. Right chart: inflows and outflows as observed in the respective quarter and expressed as a share of total loans.

Despite these early signs of asset quality deterioration, some banks have already started releasing provisions while others are planning to do so. Although this boosted profitability in the first half of 2021, as supervisors we need to ensure that banks remain vigilant and have robust risk controls in place to tackle these risks proactively.

To this end, we will continue to push banks to correctly classify loans and timely recognise deteriorating asset quality.

Last year, we sent letters to the CEOs of the banks under our direct supervision asking them to follow good practices in the identification, measurement and management of credit risk. In the Supervisory Review and Evaluation Process (SREP), we focused on the weak practices we had identified in areas such as the reporting of forbearance measures, reclassification of loans into different stages of IFRS 9 and unlikely-to-pay assessments. Our supervisors will rigorously follow up on these findings and will perform in-depth assessments of banks’ material exposures to COVID-19 vulnerable sectors, including commercial real estate.

Signs of market exuberance call for continued vigilance

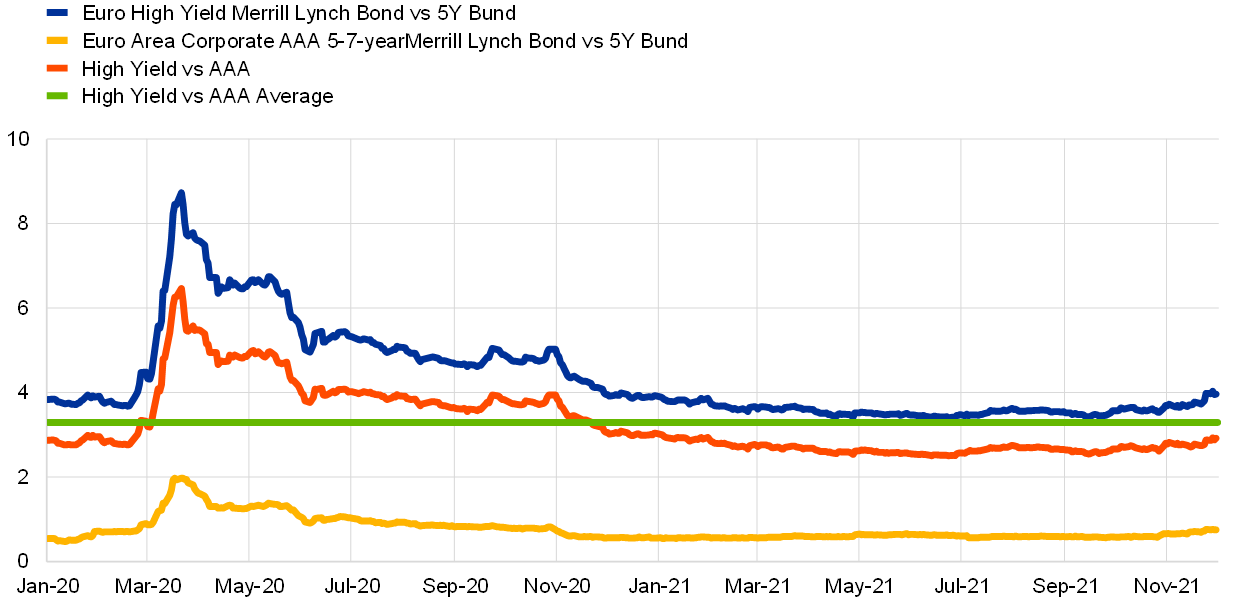

The unprecedented levels of public support have prolonged the low interest rate environment and materially increased liquidity in the system. This has led market participants to adopt a complacent attitude which is becoming increasingly evident. Funding conditions are benign, sovereign and corporate spreads are low, and spread differentials are more compressed than they were prior to the pandemic (Chart 4). Equity valuations are also high.

Chart 4:

Corporate bond spreads

(yield spreads in percentage)

Sources: Bloomberg Finance L.P. and ECB staff calculations.

Note: The latest observation is for 2 December 2021.

The search for yield has led to stretched valuations in several market segments, sometimes disconnected from economic fundamentals. This has also fed into banks’ appetite for riskier assets, including during 2020 and 2021, contributing to the build-up of risks in the leveraged loans and equity derivatives markets. It has also driven up exposures to riskier counterparties, in particular non-bank financial institutions (NBFIs), in an environment characterised by insufficient transparency.

Although it is difficult to predict how events will unfold, this situation could exacerbate the likelihood of a repricing in the debt or equity markets even further. A sudden adjustment in yields, triggered by changing investor expectations about inflation and interest rates, could cause asset price corrections. We are also concerned about possible interlinkages between credit, market and counterparty risks and spillovers to the banking sector from shocks hitting NBFIs.

We are closely monitoring this situation, especially considering banks’ sensitivities to some of the corresponding risk factors and in particular interest rates and credit spreads.

To ensure that banks are adequately prepared to withstand such market shocks, we will increase our supervisory attention to risks posed by the excessive search for yield. Our Joint Supervisory Teams (JSTs) will monitor the build-up of unmitigated risks in the area of leveraged finance and banks’ strict adherence to the supervisory expectations laid down in the related ECB Guidance[1]. Targeted on-site inspections will also look at how banks are managing counterparty credit risk, including in prime brokerage and leveraged lending business, with a focus on underwriting standards, alignment with the risk appetite and impact on capital.

Tackling emerging risks, including climate-related and environmental risks and cyber risk

Climate risk was on our radar in previous years, but as a slower-burning risk. However, we need to move faster on this front and must not ignore the warning signals calling for prompt action on climate-related and environmental risks.

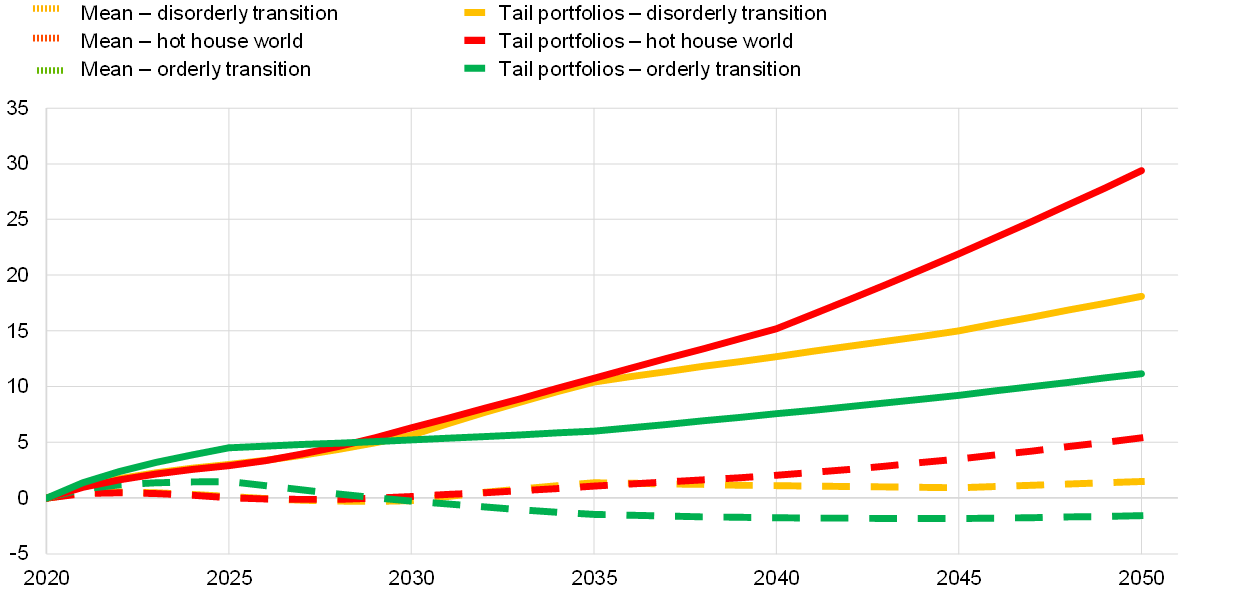

Whatever combination of physical and transition risks materialises, the economic consequences and financial risks of the climate and environmental crisis will be profound for banks (Chart 5). It is key that banks build up capacity to address these emerging risks and proactively incorporate them into their business strategies and their governance and risk management frameworks.

Chart 5:

Evolution of banks’ credit portfolio probabilities of default between 2020 and 2050

(percentages)

Source: ECB calculations based on NGFS scenarios (2020), AnaCredit, Orbis, Urgentem and Four Twenty-Seven data (2018)

Note: For a full description, please see ECB (2021), “ECB economy-wide climate stress test”, Occasional Paper Series, No 281, September.

This is why the ECB has significantly increased its efforts to systematically integrate climate and environmental considerations into all its activities.

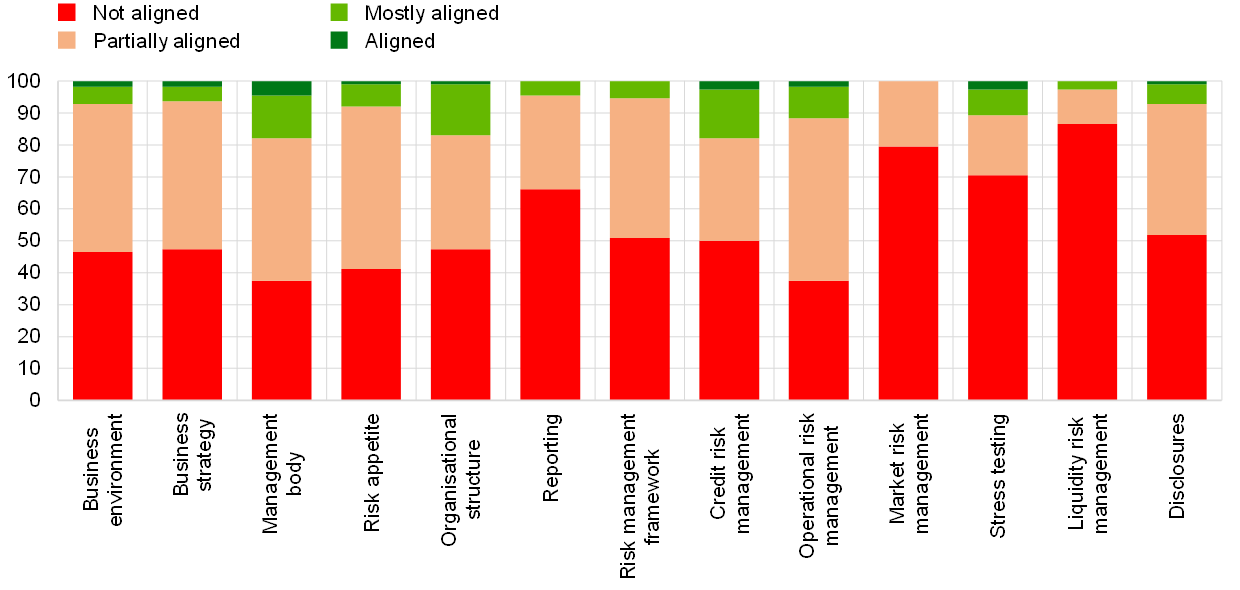

In November 2021 we published a report covering the state of climate and environmental risk management in the banking sector.[2] Although the report shows that banks have made some strides in adapting their practices, it also clearly stresses that none are close to fully aligning their practices with supervisory expectations (Chart 6).

Chart 6:

Significant institutions’ alignment with supervisory expectations on climate-related and environmental risk

(percentages)

Source: “The state of climate and environmental risk management in the banking sector”, ECB Banking Supervision, November 2021.

Note: For a full description of the 13 supervisory expectations, please see the “Guide on climate-related and environmental risks”.

In the light of these results, we are convinced that more work is needed, and a number of concrete supervisory measures are already planned for next year and beyond.

In particular, in 2022 we will carry out a thematic review on risk management practices as well as a climate-risk stress test covering all banks under our supervision. Based on a pioneering methodology, this test will assess how extreme weather events might affect banks in the next year, how vulnerable banks are to sharp increases in the price of carbon emissions, and how banks can respond to different transition scenarios over the next 30 years. It is extremely important that banks make progress in collecting and analysing available data on climate-related and environmental risks. For banks and supervisors alike, next year activities in this area will entail a learning process, which won’t proceed fast enough unless maximum effort is deployed on the analytical side.

Last but not least, the increasingly fast pace of digitalisation in financial services has given rise to an increasing number of IT and cyber risks. These risks, and the vulnerabilities that make banks susceptible to these risks, warrant a stronger supervisory focus. Among these vulnerabilities, supervisors have observed deficiencies in banks’ management of IT outsourcing arrangements as well as an increased reliance on third-party IT providers such as a cloud service providers. The number of cyber incidents reported to the ECB in 2020 compared with 2019 has increased by 54%.[3] Although not all of these reported incidents had an element of malicious intent, this clear increase in cyber risk merits particular attention. Against this backdrop, our supervisors will conduct targeted reviews and on-site inspections on cyber resilience and IT outsourcing arrangements and follow up on any detected material deficiencies.

Conclusion

Amid a risk landscape which continues to be shaped by the impact of the COVID-19 pandemic and uncertainty about how it will develop, the supervisory priorities are an important mechanism for coordinating supervisory actions across the SSM. They allow us to concentrate resources to address key vulnerabilities and set a clear course of action towards safeguarding the resilience of the European banking sector. They are also a transparency and accountability tool which makes our activity more predictable and its expected outcome clearer.

We have established new internal processes to make sure that our supervisory resources are deployed in a risk-focused manner, rather than regularly following standardised, recurrent administrative procedures. The experience of the pandemic taught us that by concentrating our supervisory work on fewer, clearer priorities we could be more effective in our communication to banks and make good progress towards achieving our objectives.

Greater, more focused supervisory pressure on the most important risk drivers could effectively combine with the strong market pressure on European banks to re-establish their business models on a more sustainable basis. Banks need to tackle the structural weaknesses that have kept profitability and market valuations at depressed levels for too long. The overall, shared objective is that the European banking sector emerges from the pandemic crisis stronger and healthier and able to contribute constructively to the digital and green transformation of our economies.

- Guidance on leveraged transactions, European Central Bank, 2017.

- “The state of climate and environmental risk management in the banking sector”, ECB Banking Supervision, November 2021.

- “IT and cyber risk: a constant challenge”, ECB Banking Supervision Newsletter, August 2021.