- THE SUPERVISION BLOG

A catalyst for greening the financial system

Blog post by Frank Elderson, Member of the Executive Board of the ECB and Vice-Chair of the Supervisory Board of the ECB, and Isabel Schnabel, Member of the Executive Board of the ECB

8 July 2022

The ECB is taking action to reduce the carbon footprint in its portfolio and push banks to better manage climate and environmental risks. Within our mandate, we are incorporating climate change considerations into our monetary policy and banking supervision.

Climate change matters for central banks. It is not only an existential threat to civilisation, it also entails severe risks for the economy. Floods, storms and wildfires have become more frequent. Extreme weather events damage infrastructure, destroy harvests and raise food prices.

To secure a liveable future, the European Union is committed to achieving climate neutrality by 2050. This will require enormous investment and innovation, and it has implications for inflation during the transition phase. It also makes parts of the capital stock redundant and creates financial risks.

So the ECB cannot ignore climate change. It has direct effects on price stability and is therefore at the core of the ECB’s primary mandate. It creates financial risks, which matter for both the ECB’s risk management of its own operations and for banking supervision. And with climate change being a priority for European lawmakers, the ECB shall take climate change into account, with reference to its objective to support the EU’s general economic policies without prejudice to price stability.

By doing so, the ECB can, within its mandate, act as a catalyst for greening the financial system. It can support the development of green capital markets, which are necessary to finance the transition to a low-carbon economy. And it can ensure that banks properly take climate-related risks into account in their lending decisions.

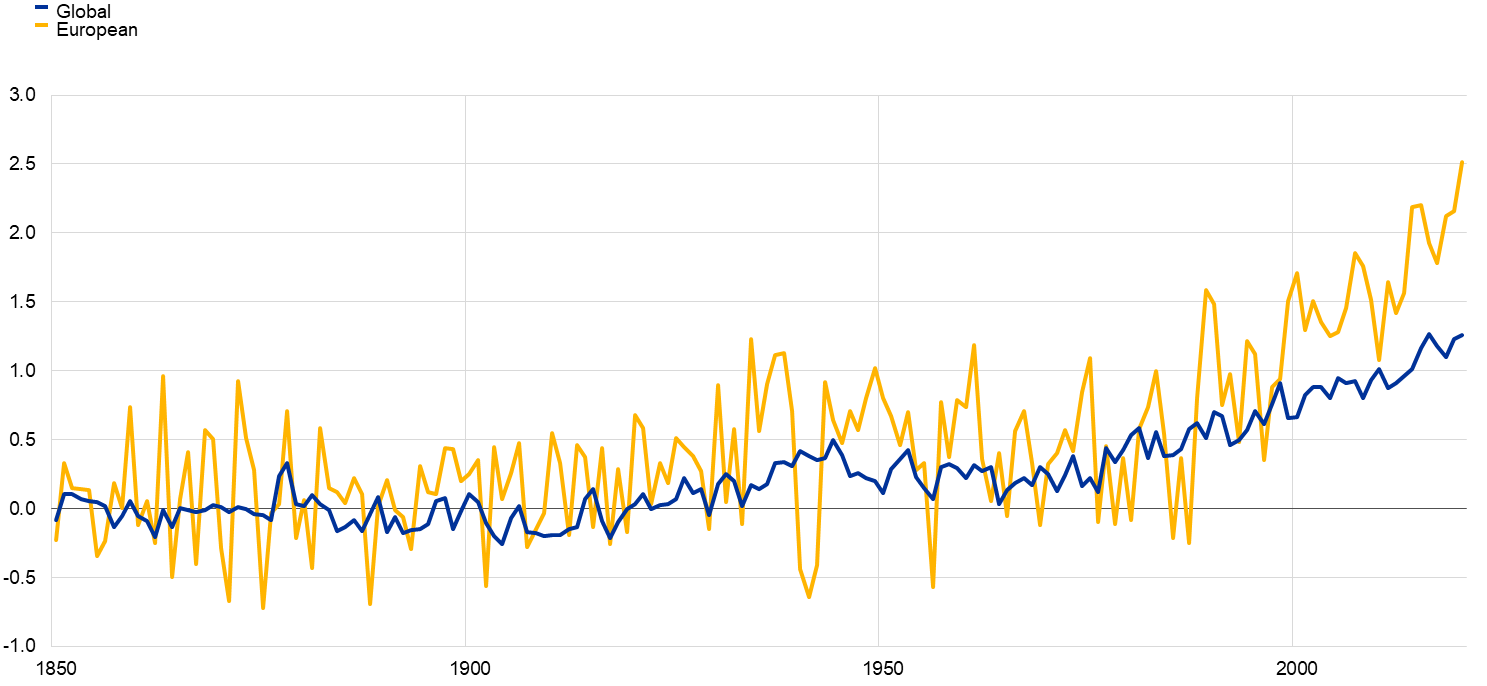

Chart 1

Global and European temperatures

(difference in degrees Celsius compared with pre-industrial levels)

Source: Annual global (land and ocean) temperature anomalies – HadCRUT (degrees Celsius) provided by Met Office Hadley Centre observations datasets.

Notes: Temperature anomalies are shown compared with the pre-industrial period between 1850 and 1899. The latest observation is for 2020.

From market neutrality to carbon neutrality

This week, the ECB presented the first milestone for incorporating climate change considerations into its monetary policy. One important measure concerns our private sector asset purchases. The ECB’s corporate bond portfolio has so far been guided by market neutrality and thus reflects the existing bond universe. However, it is companies from carbon-intensive sectors in particular that issue such bonds. This has led to a carbon bias in our portfolio and an accumulation of climate risks on our balance sheet. To reduce these risks, we will start tilting the reinvestments from maturing corporate bonds – around €30 billion every year – towards assets issued by companies with a better climate performance. This will gradually bring our corporate bond holdings onto a path that is aligned with the Paris Agreement and the EU climate neutrality objectives.

Additionally, we will limit the share of assets of high-carbon companies that can be pledged by a bank as collateral when borrowing from us. In the future, we will limit collateral to companies and debtors that are compliant with EU sustainable reporting standards.

These measures have two effects: first, they reduce our own climate-related financial risks and, second, they motivate bond issuers to improve their disclosures and reduce their carbon emissions. This will ultimately help steer capital towards supporting the green transition.

Testing banks’ resilience to climate stress

Climate change also plays a major role in our supervisory activities. Over the past few years, we have started to look much more closely at how climate change affects the banks under our supervision. Since we clarified our supervisory expectations in 2020 we have been pushing banks to improve how they manage and disclose climate and environmental risks.

As part of these efforts, we have now concluded a pioneering “bottom-up” climate stress test. We found that three in five banks still do not have a climate stress test framework in place. Only one in five banks consider climate risks when granting loans. And most banks rely heavily on proxy data to quantify their customers’ emissions with, on aggregate, half of banks’ income currently coming from heavy greenhouse gas emitters. This might be profitable today, but it won’t be tomorrow. So we will not stop reminding banks that they must take decisive action to address shortcomings and prepare for a timely transition to a carbon-neutral economy, while engaging closely with their clients.

Towards a greener financial system

Everyone involved in financial markets will need to prepare for the green transition and tackle the resulting risks. Our climate stress test proves, once again, that banks need to act boldly and urgently to better manage the risks from climate change. Our actions on the monetary policy side will not only reduce our own exposures to these risks, they will also encourage companies and banks to be more transparent about their carbon emissions – and ultimately to reduce them.

These efforts will make our financial system more resilient to the climate and environmental crises and better equipped for the green transition. There is still much more work to be done. This is only the beginning of a long journey. While the ECB’s actions are no substitute for ambitious and decisive action from governments and parliaments, within our mandate we have a duty to play our part, and we will do so.

This blog post appeared as an opinion piece in various newspapers and websites across Europe.