What happens when a bank is failing or likely to fail?

One of the big risks of the financial crisis of 2008 was that a failing bank would pull others down with it. To counter this, from October 2008 to December 2012 European Union (EU) governments mobilised more than €590 billion of taxpayers’ money for capital support to bail out banks. This was a heavy burden on economies that were already struggling to overcome the challenges of a deep recession.

To prevent a similar blow to public finances in the future, the EU institutions embarked on creating the EU banking union. The first two pillars of the banking union provide for a coordinated, single mechanism for the supervision and, if necessary, resolution of banks in the euro area.

In its role as direct supervisor of significant banks in the euro area, the ECB is responsible for assessing whether a bank is failing or likely to fail. In the first four years of the banking union, ECB Banking Supervision determined that five banks were failing or likely to fail – one in Spain, two in Italy, one in Latvia, and one (a subsidiary of a significant institution) in Luxembourg.

As banking supervisor, the ECB closely monitors how individual banks deal with the risks they face. Supervisors raise critical issues in the supervisory dialogue with the bank. They discuss possible weaknesses with the bank and set out their expectations regarding the action it should take. With due regard to proportionality, the ECB also uses its supervisory powers to ensure that banks comply with regulatory requirements. However, supervisors cannot – and should not try to – prevent each and every bank from failing. The possibility of failure is inherent to any kind of business, and is a core element of well-functioning market economies.

| Authorisation | The bank is infringing (or will infringe in the near future) the requirements for continuing authorisation in a way that would justify the withdrawal of its authorisation |

|---|---|

| Assets | The bank’s assets are less than its liabilities, or will be in the near future |

| Debts | The bank is unable to pay its debts as they fall due, or will be in the near future |

| Public financial support | The bank requires extraordinary public financial support (subject to certain exceptions) |

| In its assessment, the ECB considers all relevant information available to it in its role as banking supervisor and also whether there are any other actions that could remedy the bank’s adverse situation. | |

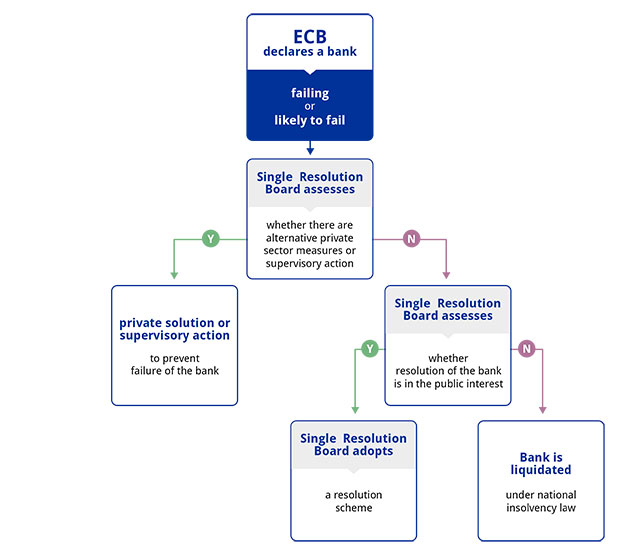

Once the ECB declares a bank failing or likely to fail, the Single Resolution Board (SRB) assesses whether it meets the remaining conditions for resolution. The SRB first evaluates whether there are any alternative private sector measures or supervisory actions that would prevent the bank’s failure within a reasonable timeframe. These might include, for instance, a merger with another bank or an investor stepping in and providing new capital. The SRB then assesses whether a resolution action is necessary in the public interest. Resolution is treated as being in the public interest if it is necessary for the achievement of the resolution objectives and if winding up the bank under normal insolvency proceedings would not meet those objectives to the same extent.

If there are no alternative measures and resolution is in the public interest, the SRB will apply a resolution action. For instance, it could (partly) sell the business of the bank or create a “bridge bank” to which to transfer its critical functions. It could create a “bad bank” to take certain assets and liabilities off the balance sheet of the “good” bank. If needed, a bail-in would impose losses on the bank’s investors and creditors. While the SRB is the single resolution authority, the ECB remains the bank’s supervisor for as long as the bank holds a banking licence. As such, it cooperates closely with the SRB.

The new framework was tested successfully for the first time with the resolution of a Spanish bank, Banco Popular. After ECB Banking Supervision had declared the bank failing or likely to fail, its capital instruments were written down and Banco Santander purchased the bank and its obligations.

If there are no alternative measures and resolution is not in the public interest, the SRB will decide not to take resolution action and the entity should then be wound up in an orderly manner in accordance with national law. Any further proceedings will thus depend specifically on the national insolvency frameworks, which are not harmonised at EU level.

For instance, in the case of the two Italian banks, Veneto Banca and Banca Popolare di Vicenza, the SRB concluded that the public interest condition had not been met. The two banks were subsequently liquidated under Italian insolvency law, which also provided for the sale of part of their business to another Italian bank.

In the more recent case of ABLV Bank, both the parent bank and its subsidiary were declared failing or likely to fail but the SRB determined that the public interest condition had not been met. In such a case, the EU resolution framework considers that the entity should be wound down in an orderly manner but relies fully on the applicable national law for this purpose. The parent bank submitted an application for voluntary liquidation to Latvia’s Financial and Capital Market Commission. For the subsidiary bank, the statutory liquidation proceeding was not initiated because the relevant conditions under national law had not been met.

This case shows that a misalignment can exist between the trigger for resolution (i.e. failing or likely to fail) as laid down in the EU resolution framework, and the trigger for liquidation under national law. It therefore underscores the need to harmonise at least the trigger events of liquidation proceedings under national law to include the case of a bank which has been declared failing or likely to fail but is not resolved because the public interest condition has not been met.

The EU banking union has laid the groundwork for a much improved toolbox for dealing with banks that are deemed failing or likely to fail. Addressing the reality of failing banks highlights where improvements could be made to further reinforce the European banking framework, especially by preventing any misalignment between the resolution and insolvency triggers.

Den Europæiske Centralbank

Generaldirektoratet Kommunikation

- Sonnemannstrasse 20

- 60314 Frankfurt am Main, Tyskland

- +49 69 1344 7455

- media@ecb.europa.eu

Eftertryk tilladt med kildeangivelse.

Pressekontakt