- THE SUPERVISION BLOG

Credit risk: Acting now paves the way for sound resilience later

Blog post by Elizabeth McCaul, Member of the Supervisory Board of the ECB

Frankfurt am Main, 19 July 2021

What a difference a few months can make. As people flock to beer gardens and cafes, return to shopping and plan their holiday travels, things are slowly returning to normal. An improving macroeconomic outlook is replacing months of uncertainty. The mood is buoyant, and we seem to be entering a more benign situation than the dire one just behind us. One could be tempted to think that this upbeat trend is also reflected in developments in the banking sector. On the surface it certainly is. But we wouldn’t be doing our jobs as supervisors if we didn’t look beneath the calm surface for any undercurrents. Indeed, based on our recent work assessing bank credit practices, the picture that emerges when we take a closer look reveals some cautionary signs.

ECB Banking Supervision introduced a range of measures to help banks support households and businesses and to cushion citizens from the economic effects of the pandemic. These were coordinated with fiscal and monetary support, such as loan moratoria and public guarantees. We are also watching closely how banks manage the cushioning effects on credit risk and how they are preparing to deal with an increase in distressed debtors after the support measures are gradually withdrawn.

In my blog post on credit risk published in December and in two letters to CEOs last year, we called on banks to put in place strong credit risk practices to maintain a clear picture of borrower creditworthiness. The pandemic environment presents unique challenges for managing credit risk. In particular, the important public support measures and flexibility put in place can mask true underlying creditworthiness. Robust risk controls allow banks to gain a line of sight into potential credit deterioration, pandemic-induced or otherwise. We want banks to be performing “look-through” credit analysis so that they aren’t lulled into a sense of complacency by any masking effects. What does the underlying creditworthiness of their borrowers look like when public support measures are withdrawn? What will be the effect on the credit performance of their borrowers after the pandemic ends? Will some borrowers have more permanent damage from the pandemic because of structural changes to the economy? Were some borrowers already weak when the pandemic began, and time hasn’t helped them improve their overall creditworthiness? This kind of inquiry needs to be built into credit risk management practices and translated into appropriate staging and classification actions straight away. This action is of paramount importance for having healthy banks when we finally emerge from the pandemic to fully enjoy the economic recovery. During the long months of lockdowns, a large number of banks did indeed move in the right direction, adjusting their practices and strengthening their controls to take developments related to COVID-19 into account.

However, following up on the letters, our assessment of bank practices shows that not all the banks we supervise have sufficiently strong credit risk practices in place to make the European banking sector resilient. What worries us beyond the immediate effects is that some of these issues seem structural, relevant not just in the context of the pandemic but also in the future when we are back to business as usual. They also affect those banks that have not suffered significant credit risk impacts in previous years. We’re asking banks to act now to avoid lasting problems down the road to ensure the economic recovery is as strong as possible.

Mixed picture

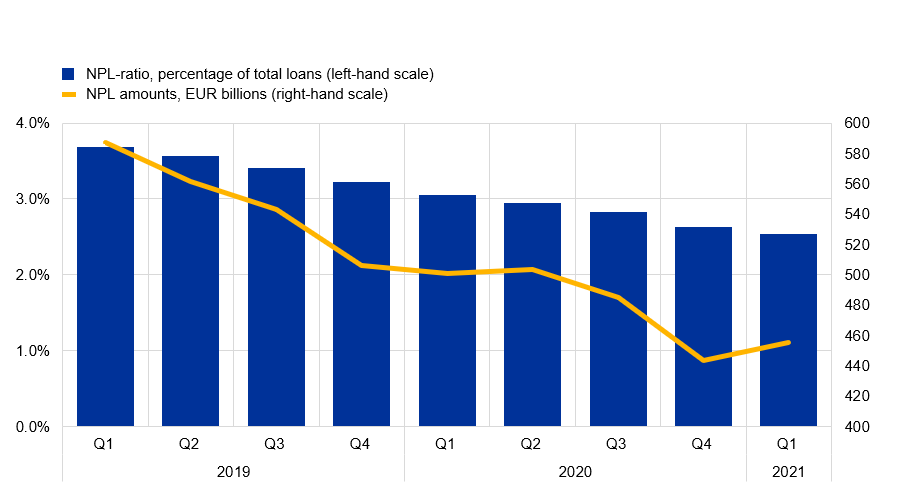

At first glance things may look rosy: many banks are reporting rising profits, while some are even beginning to release loan loss provisions (which translates to booking a profit) and others are transferring exposures back to stage 1 (the first stage of a loan when it is originated and considered fully performing) based on the economic outlook. On the positive side, the non-performing loan (NPL) ratio of banks in the euro area fell from 3.1% in March 2020 to 2.5% in March 2021 (see Chart). However, this drop disguises a slight increase in the amount of euro area banks’ non-performing loans, which rose from €444 billion in December 2020 to €455 billion in March 2021. This would appear to be an initial sign that some credit risk deterioration built up during the pandemic may not yet have peaked.

Chart

Evolution of non-performing loans among significant institutions in the euro-area

Another worrying sign is that the number of euro area non-financial corporate defaults dropped 17% in 2020 compared with 2019. This paradox for a crisis year can be explained primarily by the effects of strong support measures taken by the fiscal and monetary authorities. It can also be indicative of the masking effect I mentioned earlier. During the pandemic, support measures were necessary as well as effective in delivering much needed relief for immediate borrower liquidity issues. But they also have the effect of contributing in the near future to higher indebtedness, and as a result, to potential solvency issues being postponed. As support measures are phased out, there is the potential for increasing non-financial corporate insolvencies coinciding with the timing of support withdrawals, notably in sectors hit hardest by the crisis. The effects of the pandemic will only translate into corporate defaults with some delay once support measures are phased out, so banks need to remain prudent and recognise financial difficulties and indications of unlikeliness-to-pay at an early stage. It is still too soon to release provisioning.

As banking supervisors, we focus our assessments on the risk management practices of banks to make sure that they recognise and address credit risks in a timely manner. A third data point provides some additional clarity to the overall picture. Preliminary data from our supervisory review and evaluation process (SREP) indicate that while credit risk portfolios are not yet showing increased deterioration, risk controls are pointing towards weaknesses. Broadly speaking, credit risk is trending to levels similar to those in 2019, while in 2021 we are seeing a continued shift towards weaker risk controls.

While we observed that most banks are fully or broadly compliant with our expectations and some others are employing good practices that will enable them to be better equipped to identify and manage emerging credit risk as these unusual times move into the rear-view mirror, our goal is to provide transparency about both, i.e. areas in need of improvement and those representing best practices. We want to encourage supervised institutions to make the necessary enhancements to their risk control frameworks which are the most important safeguard against a significant deterioration in asset quality in the future. This will enable them to be more resilient as support measures are withdrawn.

Let me first describe some of the best practices that are worth noting and replicating that we would like to see more broadly adopted. Below are examples of what we observed in some banks:

- Including behavioural indicators in early warning systems for retail portfolios, building additional and pandemic-specific indicators, using machine learning tools and assessing the effectiveness of their early warning systems annually.

- Carrying out wide and structured client outreach programmes to gather relevant information such as employment status, public support measures and the impact of the pandemic on revenues.

- Increasing the frequency of credit assessment reviews and incorporating sectoral and stressed corporate client analysis into unlikely-to-pay assessments.

- Conducting targeted COVID-19 updates of collateral valuations, applying additional haircuts as a temporary solution when questions arose, and adjusting appraisals of external providers to account for effects on real estate assets.

- Performing granular forecasting based on a portfolio/geography matrix and vulnerable sector analysis.

Nevertheless, all is not rosy. Our detailed assessment revealed the need for action so that banks have credit risk management practices that are fit for purpose. Based on our assessment, we are convinced more work is needed: certain banks, including some that now have fairly low levels of credit risk, show considerable gaps in relation to supervisory expectations regarding how they should be managing credit risk. Many banks have inadequate early warning systems, are continuing to drag their feet when it comes to classifying loans as forborne or unlikely-to-pay, and/or are applying unconvincing practices for provisioning, valuing collateral and making financial forecasts.

There are eight areas of deficiencies in a number of banks giving cause for concern emerging from our detailed assessment:

- We found early warning systems that are not sufficiently granular, where indicators are mainly backward-looking, thresholds are frequently not well calibrated and regular back-testing of indicators and triggers is not being performed as frequently as required. We observed policies that provide excessive discretion in dealing with breaches leading to inconsistencies in the evaluation, management and treatment of credit.

- When it comes to flagging forbearance correctly, we observed that a significant number of banks do not always include clear and granular criteria in their policies to effectively identify financial difficulties. A significant number of banks are not including all relevant regulatory criteria in their policies, are ignoring embedded forbearance clauses and/or covenant breaches in their credit portfolios or are not following through and putting into practice good policies they have in place.

- We found banks that have not collected updated information in a structured way or adopted additional unlikely-to-pay (UTP) triggers that would make it possible to capture pandemic specificities. Others are not considering additional support measures granted by governments that may be masking the actual risk. And in some cases, UTP triggers are being removed or ignored. We also see cases where appropriate UTP assessment is being performed but is not translated into an NPL classification. And we see some structural issues, such as a lack of specific sectoral UTP indicators or of proper methodologies for the assessment of payment capacity.

- We observed cause for concern about whether banks are assigning loans consistently to stage 2 whenever there is evidence of a significant increase in credit risk. In some cases, debtors in stage 1 are re-rated, reflecting higher risk, but transfers to stage 2 are postponed. A delayed recognition of stage 2 exposures may lead to inadequate coverage in terms of provisioning. Even in the presence of provisioning overlays, belated management responses to deterioration of individual loans may lead to a build-up of NPLs.

- We found some banks using biased approaches which artificially stabilise provisions by using, for example, a limited number of scenarios predicting future losses which are not regularly updated with the relevant macroeconomic data and which do not reflect the full range of uncertainty. Other banks have adjusted triggers to reduce the number of stage transfers. And sometimes, these triggers are not adequately set to capture significant increases in credit risk.

- We also found that a number of banks lack the robust governance and high-quality risk management frameworks needed to properly estimate overlays. We observe that some banks do not have a formalised process, lack justification for decisions, do not have independent internal validation or adequate escalation and involvement of their supervisory board.

- We observed banks not complying with our NPL guidance on frequently monitoring and updating immovable collateral valuations when warranted and lacking a clear linkage between their market risk reviews and effective collateral revaluations.

- Finally, we observed some inadequate practices in the way banks include the potential impact of COVID-19 in their strategic and business planning, which could have an impact on their preparation for an increase in distressed debtors. For example, we observed cases where scenarios are too optimistic, and updates were not frequent enough.

History has taught us that in good times and in bad, strong credit risk management pays off. It provides for a resilient banking sector that can continue to support households and businesses and contribute to the overall health of the economy. Broader adoption of good credit risk management practices is needed. The remediation of deficiencies is needed even more, and as quickly as possible.

Every crisis is an opportunity

Our assessment clearly shows that there are a variety of practices when it comes to credit risk management. It is important that banks remediate credit risk management control shortfalls. We will continue to pay close attention to this. As noted, we are observing some good practices, and some banks are already in the process of remediating the gaps identified. The outcomes of our assessments are incorporated in the 2021 SREP. The outcome of the SREP will first be communicated in a dialogue between the joint supervisory teams and the banks, followed by a SREP decision letter later this year.

With the lifting of COVID-19 restrictions, we will also launch on-site inspections targeted at credit risk in the coming months, and our supervisory teams will closely monitor and challenge the implementation of remedial actions. In the second half of 2021 we will conduct a sectoral analysis of commercial real estate portfolios, with further sectors following.

If we want the real economy to keep gathering steam, we need to ensure that banks keep lending. Bad loans can pile up if banks don’t apply existing accounting and prudential rules properly and if they recognise deteriorating loans too late. This can amplify the depth of the pandemic shock, hamper economic recovery and create lasting problems. In every crisis lies an opportunity. Let’s use this one to usher in credit risk management best practices across the board.