- PRESS RELEASE

ECB publishes supervisory banking statistics on significant institutions for the first quarter of 2026

19 June 2026

- Common Equity Tier 1 ratio at 15.99% in first quarter of 2026, compared with 16.26% in previous quarter and 16.02% one year ago

- Annualised return on equity at 10.02% in first quarter of 2026, up from 9.52% in previous quarter and from 9.85% one year ago

- Non-performing loans ratio (excluding cash balances) at 2.18% in first quarter of 2026, unchanged from previous quarter and down from 2.24% one year ago

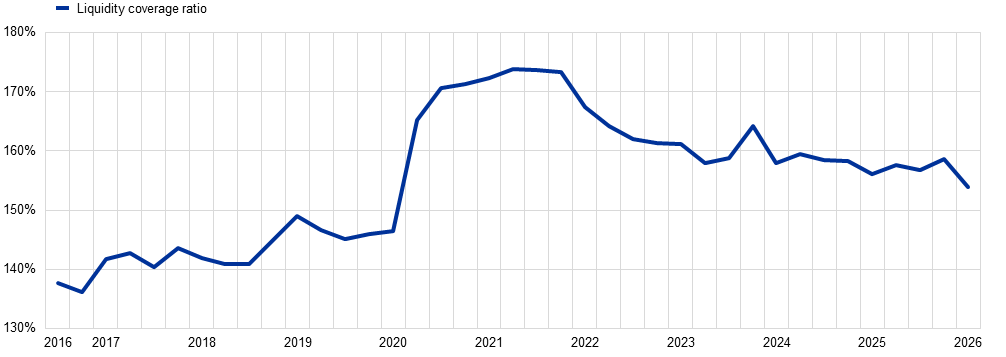

- Liquidity coverage ratio at 153.93% in first quarter of 2026, down from 158.60% in previous quarter and 156.16% one year ago

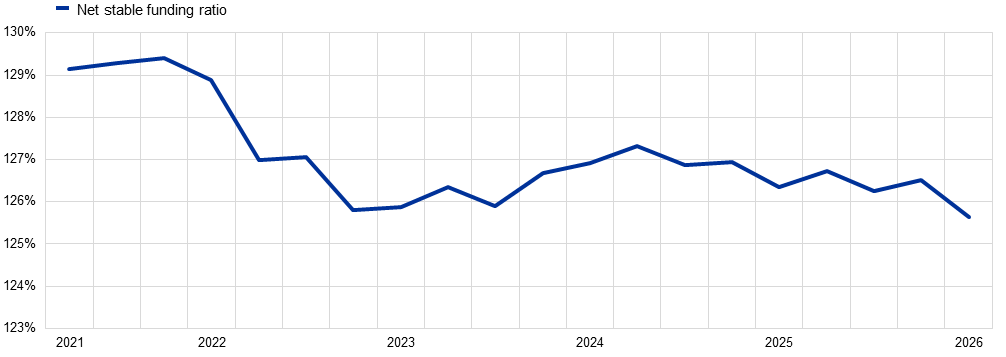

- Net stable funding ratio at 125.63%, the lowest level since series began in 2021, down from 126.51% in previous quarter and 126.34% one year ago

- Supervisory banking statistics now include new breakdown of liquidity buffer

Capital adequacy

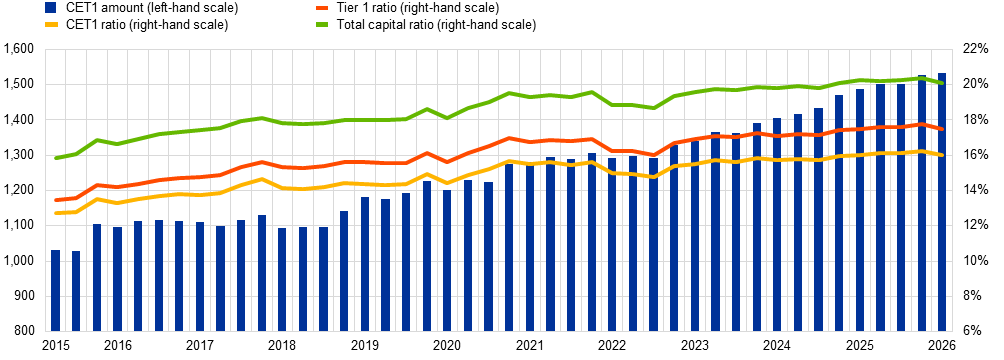

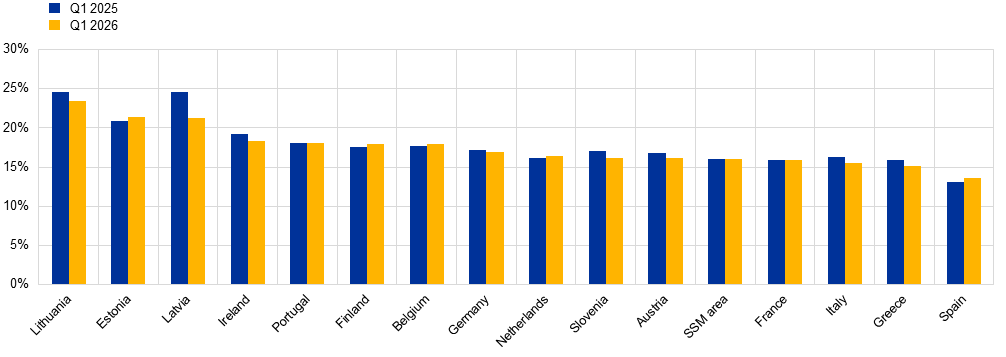

Capital ratios interactive reportIn the first quarter of 2026, the aggregate capital ratios of significant institutions (banks supervised directly by the ECB) were down from the previous quarter and from the same period last year. The aggregate Common Equity Tier 1 (CET1) ratio stood at 15.99%, compared with 16.26% in the previous quarter and 16.02% one year ago. The aggregate Tier 1 ratio stood at 17.51%, compared with 17.76% in the previous quarter and 17.50% one year ago. Meanwhile, the aggregate total capital ratio stood at 20.11%, compared with 20.40% in the previous quarter and 20.26% one year ago. Across countries, the CET1 ratio ranged from 13.67% in Spain to 23.44% in Lithuania.

Chart 1

CET1 amount and capital ratios

(EUR billions)

Source: ECB.

Chart 2

CET1 ratios by country

Source: ECB.

Notes: SSM stands for Single Supervisory Mechanism. Some countries participating in European banking supervision are not included in this chart, either for confidentiality reasons or because there are no significant institutions at the highest level of consolidation in that country.

Asset quality

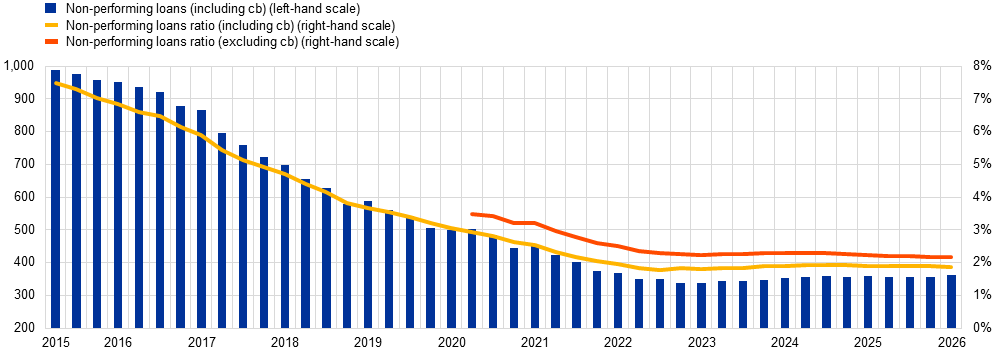

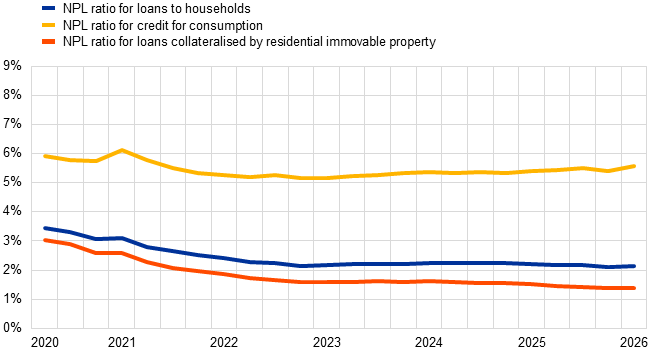

Non-performing loans interactive reportThe non-performing loans (NPL) ratio excluding cash balances at central banks and other demand deposits stood at 2.18% in the first quarter of 2026. The stock of NPLs (numerator) increased by €7.92 billion (2.2%), and at the same time the total amount of loans and advances (denominator) rose by €424.48 billion (2.6%). As a result, the ratio remained unchanged compared with the previous quarter.

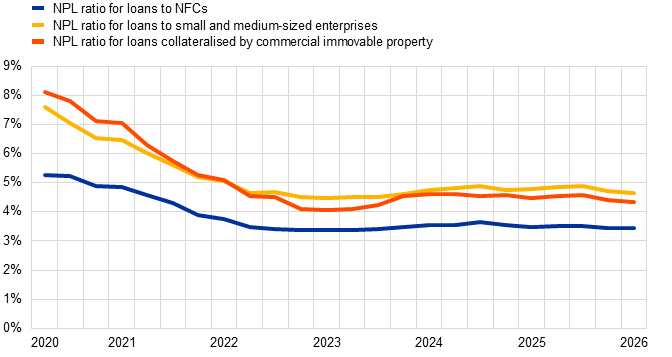

At sector level, the NPL ratio for loans to households stood at 2.14%, compared with 2.11% in the previous quarter and 2.21% a year ago. For loans to non-financial corporations (NFCs), the ratio stood at 3.44%, compared with 3.45% in the previous quarter and 3.49% one year ago. Considering the NFC portfolio by segment, the NPL ratio for loans collateralised by commercial immovable property stood at 4.35%, down from 4.43% in the previous quarter and from 4.48% one year ago. The NPL ratio stood at 4.66% for loans to small and medium-sized enterprises, compared with 4.73% in the previous quarter and 4.78% one year ago.

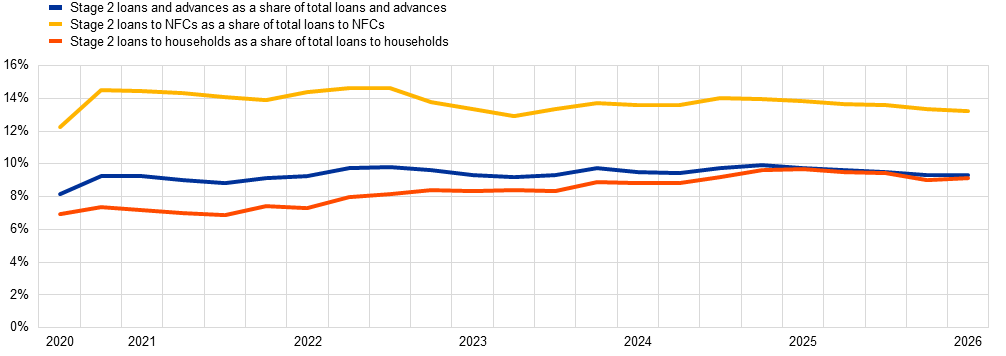

Aggregate stage 2 loans as a share of total loans decreased to 9.29% from 9.33% in the previous quarter and 9.76% one year ago. The ratio for loans to NFCs decreased to 13.23% and the ratio for loans to households increased to 9.13% from 13.32% and 9.03% in the previous quarter, respectively.

Chart 3

Non-performing loans

(EUR billions)

Source: ECB.

Note: cb stands for cash balances at central banks and other demand deposits.

Chart 4

Non-performing loans by counterparty sector

a) Breakdown of NFC portfolio by segment | b) Breakdown of household portfolio by segment |

|---|---|

|  |

Source: ECB.

Chart 5

Stage 2 loans and advances as a share of total loans and advances subject to impairment review

Source: ECB.

Note: Stage 2 assets are those that have shown a significant increase in credit risk since initial recognition. Loans and advances subject to impairment review are loans and advances at amortised cost and fair value through other comprehensive income, classified in Stage 1, Stage 2, Stage 3, or as purchased or originated credit-impaired.

Profitability

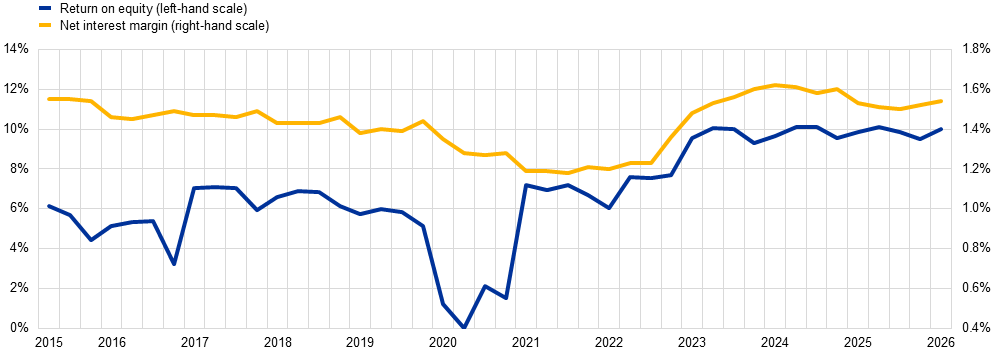

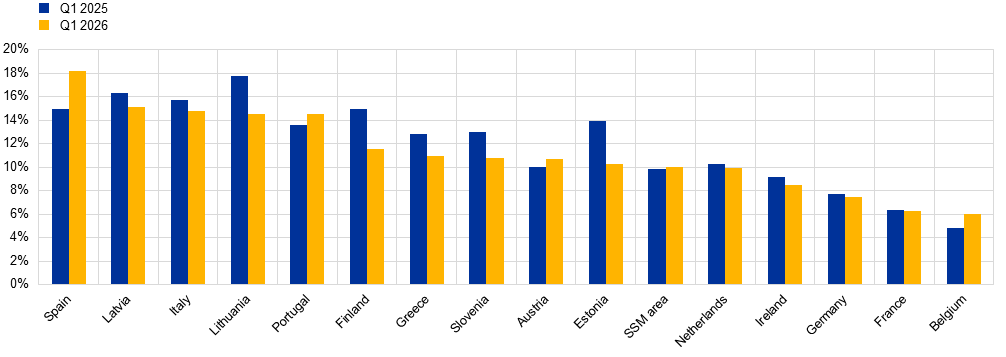

Profitability interactive reportThe aggregate annualised return on equity stood at 10.02% in the first quarter of 2026 compared with 9.52% in the previous quarter and 9.85% one year ago. The return on equity across countries ranged from 6.02% in Belgium to 18.16% in Spain in the first quarter of 2026. At the same time, the aggregate net interest margin stood at 1.54% compared with 1.52% in the previous quarter.

Chart 6

Return on equity and net interest margin

Source: ECB.

Chart 7

Return on equity by country

Source: ECB.

Notes: SSM stands for Single Supervisory Mechanism. Some countries participating in European banking supervision are not included in this chart, either for confidentiality reasons or because there are no significant institutions at the highest level of consolidation in that country.

Liquidity

Liquidity interactive reportThe aggregate liquidity coverage ratio decreased to 153.93% in the first quarter of 2026, down from 158.60% in the previous quarter and from 156.16% one year ago. This downward trend was driven mainly by an increase of €128 billion (4.0%) in the net liquidity outflow compared with the previous quarter. The supervisory banking statistics now include a new breakdown of the liquidity buffer, providing more detailed information on the composition of Level 1 assets.

Chart 8

Liquidity coverage ratio

Source: ECB.

Net stable funding ratio

Net stable funding ratio interactive reportIn the first quarter of 2026, the net stable funding ratio was 125.63%, the lowest level recorded since the start of the time series in 2021. This represents a decrease from 126.51% in the previous quarter, driven mainly by an increase of €185 billion (1.4%) in the required stable funding.

Chart 9

Net stable funding ratio

Source: ECB.

Factors affecting changes

Supervisory banking statistics are calculated by aggregating the data reported by banks which report COREP (capital adequacy information) and FINREP (financial information) data at the relevant point in time. Consequently, changes from one quarter to the next can be influenced by the following factors:

- changes in the sample of reporting institutions;

- mergers and acquisitions;

- reclassifications (e.g. portfolio shifts as a result of certain assets being reclassified from one accounting portfolio to another).

For media queries, please contact Lise Handal, tel.: +491711775875.

Notes

- The complete set of supervisory banking statistics with additional quantitative risk indicators is available on the ECB’s banking supervision website. The time series are also available for download from the ECB Data Portal.

Evropská centrální banka

Generální ředitelství pro komunikaci

- Sonnemannstrasse 20

- 60314 Frankfurt am Main, Německo

- +49 69 1344 7455

- media@ecb.europa.eu

Reprodukce je povolena pouze s uvedením zdroje.

Kontakty pro média