TRIM: reviewing internal models

Banking regulation requires institutions to hold a minimum amount of capital to absorb unexpected losses. To determine this amount, banks may use either standardised formulas or internally developed, risk-sensitive models (“internal models”) to reflect their individual risk profile, subject to a number of regulatory requirements and prior approval from the competent authorities.

In the wake of the financial crisis, criticism of internal models surged as a result of their increasing complexity and the perceived high variability in capital requirements as calculated by different banks with similar portfolios, using their own internal models.

In spite of these limitations, the ongoing work of the Basel Committee, supplemented in Europe by the additional detailed guidance provided by the European Banking Authority through regulatory technical standards and guidelines, confirms the central role of risk-sensitive models in ensuring that risk and capital are managed efficiently.

From a supervisory perspective, and in conjunction with these regulatory initiatives, in December 2015 the ECB launched the targeted review of internal models (TRIM). Key objectives of this multi-year project, conducted in close cooperation with the national competent authorities (NCAs), are to reduce unwarranted variability (i.e. variability not justified by different risk profiles) in capital requirements and to ensure consistent supervisory practices across the euro area.

Supervision. Explained. What is the targeted review of internal models?

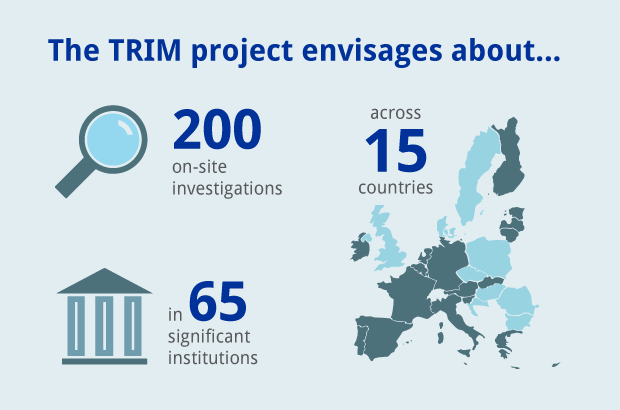

The TRIM reviews significant institutions’ most critical and material internal models for credit risk, market risk and counterparty credit risk. TRIM on-site investigations started in 2017, following preparatory work in 2016, and will continue throughout 2019.

Given the magnitude and complexity of the project, a comprehensive and multi-layered quality assurance framework has been put in place to ensure consistent and comparable outcomes across banks and to promote and maintain a level playing field in all countries that are part of the Single Supervisory Mechanism.

A first layer of quality assurance in the TRIM project was to establish a common, standardised methodological framework to serve as the basis for the harmonised execution of TRIM on-site investigations. This includes the following elements.

- ECB guide to internal models. The key objective of the guide is to foster transparency on how the ECB understands the regulatory requirements for internal models and how it intends to apply them when assessing whether banks meet these requirements. The guide was recently issued for public consultation.

- Public consultation on the ECB guide to internal models – risk-type-specific chapters

- Common inspection techniques and tools. Each assessment team conducting TRIM on-site investigations is required to adopt these to ensure uniform approaches to and coverage of pre-defined areas of investigation.

- Close interaction between the assessment teams and the central risk-specific teams during the execution of each on-site investigation, to ensure that the inspection techniques and tools are applied consistently.

To facilitate the adoption of this common methodological framework, extensive training sessions have been carried out over time for the assessment teams. These are complemented by “question and answer” support for banks and assessment teams.

A second layer of quality assurance is implemented on an ongoing basis, after each on-site investigation is completed. The report produced by the assessment team to document their reviews is checked for consistency by internal model experts from different NCAs and the ECB, who have a horizontal view of the TRIM investigations for each risk type. The aim here is to ensure that similar shortcomings give rise to similar findings.

Finally, a third layer of quality assurance is applied ex post, when a supervisory decision is prepared on the basis of the findings of each on-site investigation. The preparation of the decisions is supported by regular exchange and alignment sessions for the model experts, who also benefit from access to a comprehensive overview of past cases. In addition, multiple layers of managerial review and challenge are applied within the ECB before the decision is sent to the bank.

As of October 2018, more than half of the banks participating in TRIM have received their first supervisory decisions. In addition to 21 decisions relating to general topics (such as model governance or internal validation), more than 50 decisions stemming from TRIM on-site investigations have been shared with the banks so far.

In this context, and to foster transparency, in June 2018 the ECB published an overview of the outcomes of the general topics review and a preliminary update on the outcomes that have emerged so far from the TRIM on-site investigations, with a focus on credit risk.

Further details on examples of key findings observed up to May 2018.

As a next step, the execution of the TRIM project will continue with a focus on reviewing models for low-default portfolios (which include, for example, exposures to mid-sized/large corporates or financial institutions). The objective is to finalise all on-site activities in the course of 2019. Further updates on TRIM will be shared with the industry in due course, through the regular communication processes that have been established.

European Central Bank

Directorate General Communications

- Sonnemannstrasse 20

- 60314 Frankfurt am Main, Germany

- +49 69 1344 7455

- media@ecb.europa.eu

Reproduction is permitted provided that the source is acknowledged.

Media contacts