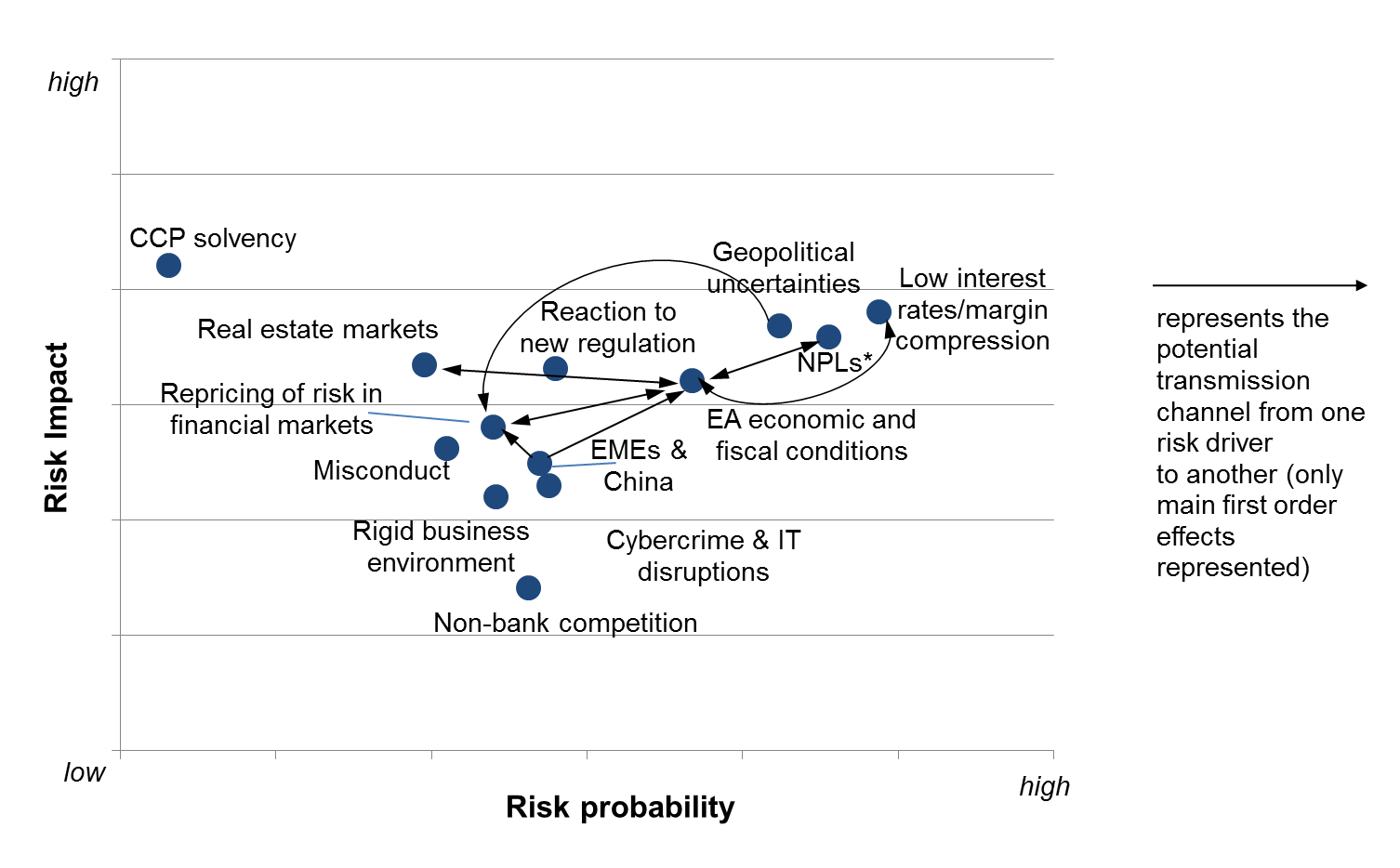

Mapping the key risks to euro area banks for 2018

Every year, ECB Banking Supervision – in close cooperation with national supervisors – updates the Single Supervisory Mechanism (SSM) risk map that ranks key risk drivers affecting the euro area banking system. The map reflects the judgement of European banking supervision experts and draws on a variety of sources, including our own analysis and discussions with banks and relevant authorities. Following its latest update, the SSM risk map also serves as a basis for defining the ECB’s supervisory priorities for 2018, which will be published by the end of this year.

The economic environment within which euro area banks operate continued to improve over the last year amid supportive ECB monetary policy measures. Moreover, some banks made relevant progress in strengthening their balance sheets and tackling non-performing loans (NPLs). At the same time, work on completing the euro area regulatory agenda has also advanced, which helps to reduce regulatory uncertainty. These developments contributed to a certain reduction in some risks surrounding supervised institutions. However, other substantial risks persist and the risk constellation has not changed considerably since the publication of the SSM risk map for 2017.

The prolonged period of low interest rates continues to challenge banks’ profitability. Low interest rates reduce funding costs and are supportive to the economy, but they also play a role in compressing net interest margins and thus weigh on banks’ profitability. While banks may need to adapt their business models and cost structures as a result, we must ensure that pressure to increase profitability does not trigger excessive risk taking. The results of this year’s profitability forecast exercise show that banks expect a return to moderate profitability levels after 2017, with their aggregate return on equity projected to reach 7.4% in 2019.

High levels of NPLs constitute another major concern for a significant number of banks in the euro area. Compared to last year, banks have made some progress in tackling NPLs. This is reflected in a decline in the aggregate NPL ratio from 6.5% in the second quarter of 2016 to 5.5% in the second quarter of 2017. Nevertheless, the number of high-NPL banks in the euro area remains substantial. Persistently high levels of NPLs cripple banks’ profitability as they lock up their capital in unproductive assets and hinder their lending capacity. It is thus of the utmost importance that banks step up their efforts to build and implement ambitious and credible NPL strategies. Moreover, further reforms are needed to address structural impediments to NPL workout. This includes improving the efficiency of secondary markets for distressed assets, collateral enforcement mechanisms and insolvency and restructuring frameworks.

Improving economic conditions in the euro area are expected to support banks’ asset quality and profitability in the future. However, the current economic situation and the growth outlook differ across euro area countries. Moreover, debt sustainability concerns are still high in some Member States, which remain vulnerable to a potential repricing in bond markets – especially if such a repricing were not accompanied by a sufficient rise in GDP growth.

Continuing very low levels of risk premia in financial markets create potential space for a sudden reversal. This is particularly relevant in the current context of historically high geopolitical uncertainty that could result in sudden changes in financial markets’ risk appetite and affect banks via the repricing of their mark-to-market holdings and funding costs.

Uncertainty around the final outcome of the UK’s negotiations to leave the European Union creates additional challenges. Brexit-related concerns encompass not only business continuity and transitional risks for the euro area and UK banks, but also macroeconomic and regulatory risks, including potential regulatory arbitrage.

As the post-crisis regulatory agenda is being finalised, banks need to further adjust their business models to the new regulatory environment. While the process of finalising and fine-tuning the regulatory framework is conducive to banking sector stability in the medium term, the transition to the new regulatory landscape may involve short-term costs and risks for banks, including failure to adapt in time. These risks have somewhat decreased since last year as more details about current regulatory initiatives have become known.

Finally, euro area banks face a number of risks that deserve supervisory scrutiny, including cybercrime and IT disruptions, growing non-bank competition, especially from “fintech” companies, turbulence in real estate markets or misconduct risk. Moreover, structural rigidities in the business environment in which banks operate may prevent them from making the adjustments needed to function efficiently.

SSM risk map 2018 for euro area banks

Source: ECB and national supervisory authorities.

Notes: The risk map shows the probability and the impact of risk drivers that range between low and high.

*NPLs: this risk driver is only relevant for euro area banks with high NPL ratios.

European Central Bank

Directorate General Communications

- Sonnemannstrasse 20

- 60314 Frankfurt am Main, Germany

- +49 69 1344 7455

- media@ecb.europa.eu

Reproduction is permitted provided that the source is acknowledged.

Media contacts