Foreword by Christine Lagarde, President of the ECB

The cut-off date for the foreword by the President and the interview with the Chair of the Supervisory Board was 28 February 2023.

2022 was a challenging year for people in the euro area. The economy was well on the way to recovering from the pandemic but was negatively affected by Russia’s unjustified invasion of Ukraine. While the immediate impact of the war on banks was limited, as few of them had significant exposures to the afflicted regions, banks faced an environment marked by profound economic uncertainty and historically high inflation.

The war-induced energy crisis, combined with supply chain bottlenecks and pent-up demand from the pandemic, led to strong inflationary pressures. In such a setting, it is the task of monetary policymakers to ensure that inflation does not become entrenched and that it returns to target in a timely manner. The ECB acted accordingly and embarked on monetary policy normalisation by ending net asset purchases and then raising interest rates.

Rising interest rates affected the performance of supervised banks in 2022. Profitability, which serves as banks’ first line of defence against shocks, was supported by net interest income, which increased for the first time in several years. This, together with the continued improvement in asset quality, with non-performing loans having fallen to their lowest level since 2015 when banking union data measurements began, ensures that our monetary policy impulses are transmitted smoothly by banks to the euro area economy.

However, in an environment where funding conditions are tightening, banks must continue to tackle concerns about their governance and their internal risk control frameworks. European banking supervision is therefore keeping a close eye on the build-up of risks.

Meanwhile, even before 2022, banks needed to adapt their business models to the structural challenges posed by digitalisation and climate change, which have been exacerbated by Russia’s unjustified war in Ukraine. The war has further heightened the risk of cyberattacks, and as Europe weans itself off Russian oil and gas, transition risks are accelerating. These, and increasing physical risks, require a proactive and comprehensive approach from banks to become more resilient to climate and transition shocks.

The ECB has already undertaken a number of significant steps to make sure banks are up to the challenge. We will not relent in our efforts and will keep on playing our part in ensuring that Europeans continue to rely on a robust banking sector.

Introductory interview with Andrea Enria, Chair of the Supervisory Board

The cut-off date for the foreword by the President and the interview with the Chair of the Supervisory Board was 28 February 2023.

A lot happened in 2022. How was it for ECB Banking Supervision?

In one sense, 2022 was a year in which we went from one crisis to another. At the beginning of the year, all signs pointed to a steady recovery from a pandemic that had turned our lives and economies upside down. I vividly remember that, for the first time in a long while, banks and analysts were looking to the near future with some optimism, which was just when Russia unjustifiably invaded Ukraine. First and foremost, Russia’s war has put Ukrainians through untold suffering. It has also brought economic and financial turmoil to Europe and right across the globe, gradually turning into a fully fledged macroeconomic shock.

We had to react quickly and be agile in our supervision in order to address the fast-changing economic circumstances and the resulting challenges for the banking sector. A handful of banks were affected directly by the war and sanctions, owing to their direct exposures to or interlinkages with Russia. But all banks alike were prone to being adversely affected by the energy and commodity shock, as well as by the environment of persistently high inflation coupled with the fast-paced normalisation of monetary policy.

Yet, in another sense, it was a year of development for ECB Banking Supervision. Our staff went back to working in the office more regularly, and it has been a real pleasure to see our offices buzz with activity once again. I have enjoyed chairing more in-person Supervisory Board meetings and I was very happy to be able to visit several national competent authorities in person.

We also made some good progress towards greater integration between the ECB and the national competent authorities that participate in the Single Supervisory Mechanism (SSM). We are further fostering a common SSM culture and integrated career paths, creating opportunities for supervisors to work more closely throughout the supervisory cycle, pursuing more coordinated planning and budgeting, further developing SSM tools for collaboration and introducing common technologies for both supervision and training.

How have banks fared following the Russian war in Ukraine?

We should make a distinction here between banks with direct interlinkages to Russia and all other banks.

A handful of banks were directly affected by the geopolitical events, mostly on account of the sanctions framework. Sberbank Europe AG, a banking group headquartered in Austria with Russian ownership, was, together with its subsidiaries in Croatia and Slovenia, hit by the reputational impact, and experienced significant deposit outflows. The bank was ultimately declared failing or likely to fail and exited the market. Another example of this kind was RCB Bank LTD, a Cypriot bank in which the Russia-based bank VTB was a significant shareholder. Following the imposition of sanctions and the changed geopolitical situation, the bank opted for a voluntary wind-down of its banking business, which led to the withdrawal of its banking licence.

Euro area banking groups with a direct presence in Russia are also prone to incurring losses should they wish and manage to exit that market. For some, this risk has already crystallised, but with a contained and manageable impact.

So far, the banking sector as a whole has proven very resilient to the war-induced macroeconomic shock, even more so than we had expected based on the vulnerability analysis we published in May 2022. The aggregate Common Equity Tier 1 ratio stood at 14.7% at the end of the third quarter of 2022, only slightly below the level seen at the end of 2019. Asset quality continued to improve, with the volume of non-performing exposures held by significant banks dropping to €349 billion at the end of September 2022, the lowest level since supervisory data on significant banks were first published in 2015. Profitability was also the strongest on record, with banks’ average return on equity reaching 7.6% in the third quarter of 2022.

On the back of this positive performance, banks have planned distributions for 2023 which are pretty much in line with the catch-up in dividends and buybacks they made in 2022, coming out of the pandemic-related restrictions. We have not objected to any bank-specific plans, but we have engaged in a bilateral supervisory dialogue with all of the banks as part of our business-as-usual assessment of capital trajectories.

Towards the end of 2022, the macroeconomic outlook started to improve again. But this does not mean that the macroeconomic shock is over. If inflationary pressures should persist, the necessary fast-paced monetary policy normalisation process could in turn affect specific banks’ portfolios and business lines, bringing a wide range of challenges and creating potential winners and losers.

Speaking of challenges, which are the key challenges facing European banks in your opinion?

The first set of challenges is conjunctural.

If the energy crisis is not remedied, credit risk may increase in those corporate lending portfolios where economic activity is most dependent on energy. More generally, the slowdown in our economy towards the end of last year was accompanied by a resurgence in corporate defaults, which calls for heightened vigilance regarding asset quality.

The fast-paced normalisation of monetary policy – and particularly the increasing interest rates – was an important driver of the recovery in profitability. However, this may also lead to a deterioration in asset quality, with borrowers struggling to repay their debt, across a set of loan portfolios that are particularly sensitive to interest rates.

This shift in the interest rate environment could also cause disorderly adjustments in some segments of the financial market and in non-bank financial institutions, increasing counterparty credit risk among banks that have concentrated exposures towards those particular markets and market players.

Beyond the conjuncture, the normalisation of interest rates and the quantitative tightening may force some banks to revise their medium-term funding strategies and place greater focus on liquidity and funding risks.

The 2022 Supervisory Review and Evaluation Process (SREP) shed new light on a set of persistent weaknesses. Risk control deficiencies are still affecting credit risk scores, and there were a number of findings on the effectiveness of management bodies, risk management, compliance and internal audit functions. Our concerns about banks’ risk controls and governance are exacerbated by the uncertain external environment, as backward-looking indicators of risk levels can provide an inaccurate picture when forecasting future trends and risks.

The digital transformation, as well as climate-related and environmental risks, are also key medium-term challenges for our banks and require immediate and focused attention.

You mentioned monetary policy normalisation. How are European banks positioned for the changing interest rate environment?

Interest rates going up is usually a good news story for banks. It means they can earn more from the interest rate margin – the difference between the interest rate that they charge for loans and the interest rate that they pay on deposits. The normalisation of interest rates and the boost that this long-awaited shift provided to net interest income is at the core of banks’ positive performance in 2022. For the first time in several years, net interest income increased not only because of expanding lending volumes, but also because of expanding net interest margins.

Banks and analysts alike expect the profitability outlook to remain similarly positive this year. According to our data, if the macroeconomy develops as currently expected, further orderly increases in interest rates will likely support the sector’s average earnings.

However, if we depart from the baseline scenario and consider more adverse developments, things may go differently. For specific portfolios and business lines, the costs associated with a deterioration in asset quality may outweigh the income benefits as interest rates increase, particularly if economic growth slows down. Borrowers may struggle to repay their debt across portfolios that are traditionally very sensitive to the cost of credit. Consumer lending, real estate lending and leveraged finance are notable examples of areas of supervisory focus.

As I mentioned, financial markets can turn disorderly during the interest rate adjustment process. The prolonged period of low interest rates favoured an unprecedented increase in debt levels, with some less or non-regulated entities taking highly leveraged and often very concentrated positions, which can quickly unravel if the economic outlook or the interest rate environment changes unexpectedly. The failure of Archegos in 2021 and the liability-driven investments turmoil in the United Kingdom in 2022 show how, in the absence of policy interventions, such episodes can easily spill over to the banking sector.

Increasing interest rates and quantitative tightening require banks to sharpen their focus on liquidity and funding risks. If banks do not swiftly adapt their risk management and strategic steering capabilities, a more challenging funding environment may call into question overly simplistic and clearly obsolete asset and liability management strategies, such as the carry trade practices adopted by some banks to benefit from the extraordinary monetary policy support. There is a risk that banks might be caught off guard.

Banks’ risk controls and internal governance were a focus area in 2022. How much further improvement do you expect to see from banks in this area?

To be honest, it’s an area where we are not seeing enough progress.

First, in 2022 there continued to be shortcomings in data aggregation and reporting owing to deficiencies in the effectiveness of data governance and data quality management procedures, fragmented IT landscapes, and the limited scope and ambitions of banks’ remediation projects. This makes it difficult for their management bodies to have the information they need to be able to manage risks and steer the strategy of their organisation.

Second, several banks still needed to further improve their internal control functions, particularly to address insufficient staffing, the low stature of the function and deficiencies in processes, such as compliance monitoring programmes and the definition of banks’ risk appetite. The targeted reviews we carried out during 2022 looked at banks’ risk management practices in relation to areas linked to the pandemic crisis and the normalisation of interest rates, notably commercial and residential real estate lending, interest rate and credit spread risks in the banking book, and counterparty credit risk.

To facilitate tangible progress where it is most needed, we are determined to make full use of all the supervisory tools and powers available to us under EU and national law. Where qualitative measures have not been effective enough in ensuring banks follow up and remediate identified weaknesses in a timely manner, we may use targeted Pillar 2 capital requirements, enforcement measures or sanctions to ensure that appropriate progress is made. To make our supervision even more effective, where banks’ progress is too slow and their results are persistently unsatisfactory, the ECB will reconsider how it escalates supervisory measures within a clearly defined time frame.

Some people say that European banking supervision is too intrusive, too burdensome, and imposes higher requirements which are harmful to the competitiveness of EU banks. How would you respond?

First of all, it is simply not true to say that regulatory and supervisory capital requirements are higher in the EU than in other jurisdictions such as the United States or the United Kingdom. We frequently meet with our colleagues from the US and the UK authorities and compare the requirements that we place on our banks, and I must say that we are in the same ballpark as our peers. If anything, the capital requirements for the largest systemically important European banks – which are the ones that truly compete across global markets – are a little bit lighter.

That being said, we are always willing to listen to criticism. In fact, we are currently making changes to our supervisory processes that should help to address some of the industry’s concerns.

We are introducing a risk tolerance framework, which will allow supervisors to intensify their efforts where they are most needed, facilitating the transformation of strategic SSM-wide supervisory priorities into supervisory planning for each specific bank. The risk tolerance framework does not relax supervisory standards or the intensity of our supervision of any given bank. Instead, it increases our focus on risk-based supervision. This also means banks should expect less tick-the-box supervision, potentially fewer requests and a reduced reporting burden, as we will not apply the full, comprehensive supervisory manual to each bank. We will instead be guided by bank-specific priorities. This is an important step towards making our supervisory processes more agile, adaptive, proportionate and risk based.

Through the new multi-year SREP, our supervision will also become less burdensome, as we will spread our supervisory interactions with the banks on different risk areas across multiple years rather than trying to cover everything each year. This will also help us to be more risk focused by prioritising the most important risk areas in any given year. We are also awaiting feedback from an independent panel of experts that is evaluating our SREP process and we will consider further increasing transparency over our methodologies. All of these initiatives are geared towards making our supervisory processes as attuned as possible to the risks that supervised banks may have to contend with in the future.

1 Banking Supervision in 2022

1.1 Banks under European banking supervision in 2022: performance and main risks

1.1.1 Resilience of banks under European banking supervision

Following the disruption of the Russian war in Ukraine, capital ratios remain sound at pre-pandemic levels

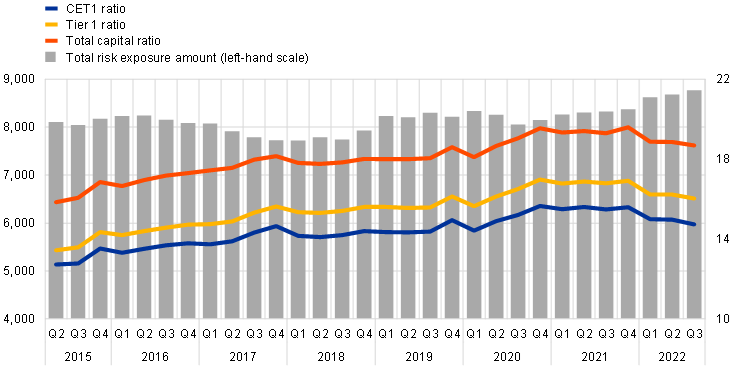

Significant institutions (SIs) had entered 2022 firmly on the path to recovery from the coronavirus (COVID-19) pandemic and with solid capital positions. The initial impact of the Russian war against Ukraine was contained, affecting only a very limited number of banks with direct exposures to the areas involved in the war. However, this rapidly evolved into an energy crisis and a wider macroeconomic shock characterised by persistent inflationary pressures and the fast-paced normalisation of monetary policy. Despite a decline in the first half of 2022, the euro area banking sector remained resilient, with the aggregated Common Equity Tier 1 (CET1) ratio standing at 14.7% at the end of the third quarter of 2022 (Chart 1), only slightly below the level seen at the end of 2019. With the banking sector reporting record levels of profitability during 2022, the decrease in the aggregate CET1 ratio was mostly driven by asset growth.

Less significant institutions (LSIs) saw their capital positions deteriorate, albeit remaining strong, as the average CET1 ratio declined by 54 basis points year on year to 17.0% in the third quarter of 2022 on the back of growth in lending and weaknesses in overall profitability. Risk exposure amounts increased by €112 billion or 4.8%, while eligible CET1 rose by just 1.5%.

Chart 1

Capital ratios of significant institutions (transitional definition)

(left-hand scale: EUR billions; right-hand scale: percentages)

Source: ECB supervisory statistics.

Note: The sample includes all SIs at the highest level of consolidation within the SSM (varying sample).

The aggregate leverage ratio for SIs stood at 5.2% in the third quarter of 2022 (Chart 2), among the lowest levels seen since the start of European banking supervision but still well above regulatory requirements and buffers. The drop (-90 basis points) experienced in the first three quarters of 2022 was largely driven by the increase in exposures, which reflected asset growth in the banking sector, but also, albeit to a lesser extent, by the expiry at the end of March 2022 of the exemption from including central bank exposures in the calculation of the leverage ratio. The aggregate leverage ratio for LSIs stood at 8.6% in the third quarter of 2022, which was lower as compared with the third quarter of 2021.

Chart 2

Leverage ratio of significant institutions

(percentages)

Source: ECB supervisory statistics.

Note: The sample includes all SIs at the highest level of consolidation within the SSM (varying sample).

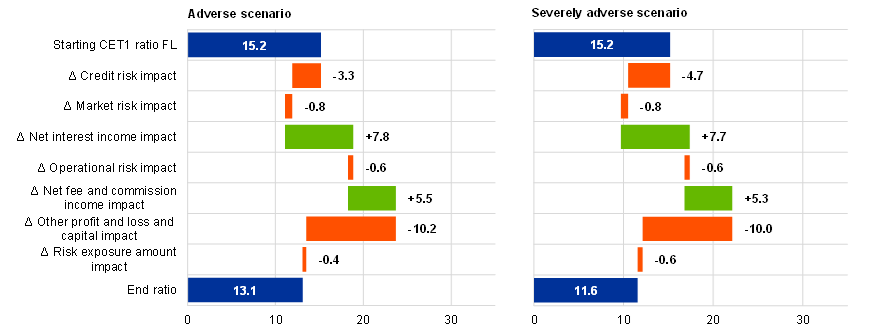

Box 1

Vulnerability analysis of banks’ resilience: war in Europe

Assessing second and third-round effects of the Russian war in Ukraine on significant institutions

Following the abrupt change in the geopolitical environment as a result of the Russian war in Ukraine, the ECB conducted a vulnerability analysis of banks’ resilience in the first half of 2022. This ad hoc assessment enhanced supervisors’ understanding of banks’ overall resilience.

The vulnerability analysis assessed the resilience and solvency of significant institutions under different adverse scenarios which reflected the high degree of uncertainty at the beginning of the war. Results confirmed the overall resilience of banks under European banking supervision, even when considering second and third-round effects stemming from the Russian war in Ukraine. The aggregate CET1 ratio (in fully loaded terms) was estimated to be 11.6% under a severely adverse scenario, with capital depletion amounting to 3.6 percentage points. It reached 13.1% under the adverse scenario, with capital depletion amounting to around 2.1 percentage points.

Chart A

Waterfall chart of aggregate results under adverse and severely adverse scenarios by risk type

(percentage points of CET1 ratio, fully loaded (FL))

Source: ECB calculations.

Notes: Market risk shocks and resulting impacts, as well as operational risk impacts, were the same under both scenarios. Impacts from net fee and commission income differ only slightly on account of similar financial shocks under both scenarios. For other profit and loss and capital, the impact stems from cost items whose contributions were left constant over the projection horizon.

This in-house exercise combined existing supervisory data with data from the 2021 European Banking Authority (EBA) EU-wide and ECB SREP stress tests, where appropriate. The methodology employed broadly followed the EBA 2021 EU-Wide Stress Test Methodological Note. ECB top-down models were used to assess banks’ credit and market risks, as well as risks to their profitability. New modules examined banks’ exposures to vulnerable sectors, existing stocks of non-performing loans (NPLs), targeted longer-term refinancing operation repayment effects and possible effects from a total loss arising from exposures to Belarus, Russia and Ukraine (“walk-away” effect).

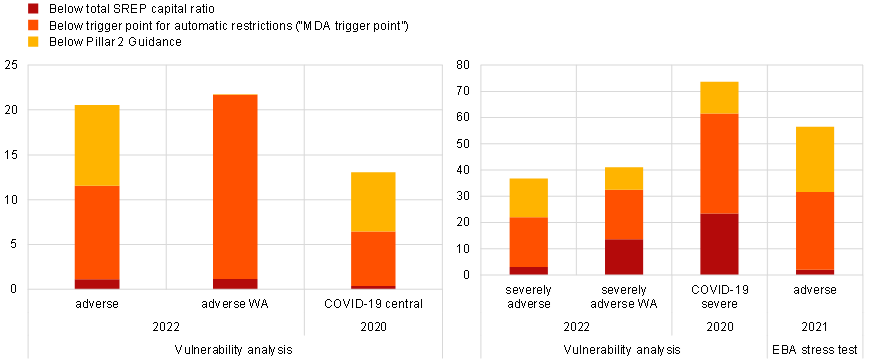

Chart B

Banks that fall below capital requirements in selected stress test exercises

(percentages of total risk exposure amount in the respective sample of significant institutions)

Source: ECB calculations.

Notes: The left panel shows mid-scenarios; the right panel shows severe scenarios under selected stress test exercises, i.e. the 2022 vulnerability analysis (also including “walk-away” (WA) effects), the 2020 COVID-19 vulnerability analysis and the 2021 EBA EU-wide stress test. CET1 ratios under transitional arrangements were compared with the individual total SREP capital ratio, the trigger point at which the maximum distributable amount (MDA) applies and Pillar 2 guidance by bank.

The three scenarios (baseline, adverse and severely adverse) considered were rooted in the March 2022 ECB staff macroeconomic projections for the euro area and are described in detail in the May 2022 Financial Stability Review.

The results of the vulnerability analysis served as input for direct supervisors to challenge their supervised banks, in particular those identified as most vulnerable to the current conditions. Aspects discussed included the severity of scenarios in bank-internal stress tests, stress-testing methodologies, sectoral concentrations, adequacy of provisioning and the challenges to profitability posed by a rising interest rate environment. This type of top-down exercise cannot yet fully replace bank-led, bottom-up stress tests. However, being able to quantify stress impacts centrally proved indispensable for supervisors to quickly assess the possible effects of the Russian war in Ukraine.

Asset quality continued to improve in 2022, keeping the cost of risk under control, but exposures to vulnerable sectors continue to be closely monitored

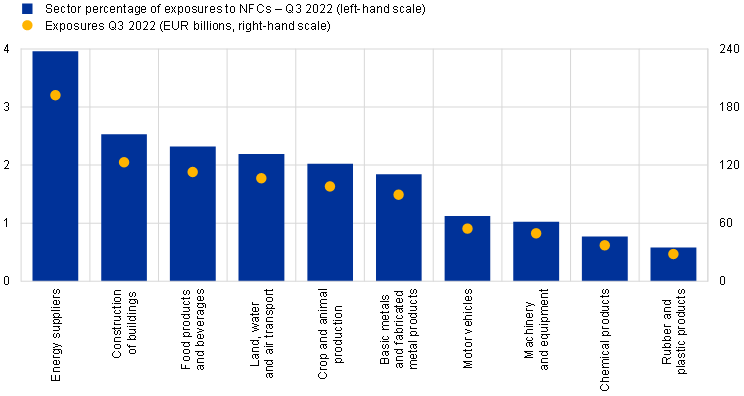

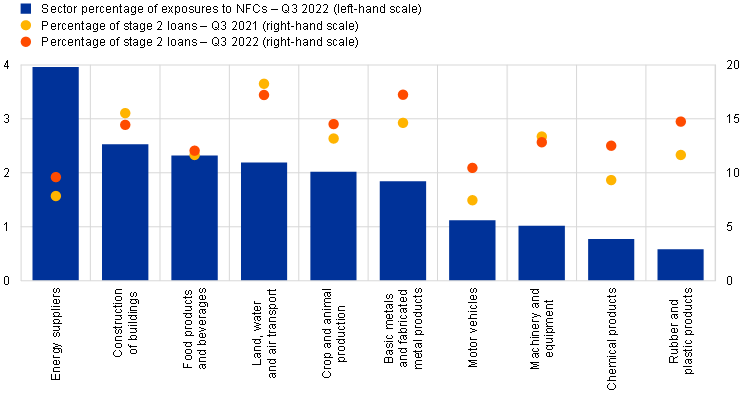

Asset quality continued to improve over the course of 2022. With no signs of material levels of crystallised credit risk and in the light of the sizeable amount of overlays of provisions built up during the pandemic, after a slight uptick at the start of the Russian war in Ukraine, the average cost of risk reverted to a downward trend over the second and third quarters of 2022, generally returning to pre-pandemic levels. In addition, NPL volumes decreased across virtually all portfolios in the first half of 2022, with some minor increases in consumer and small and medium-sized enterprise (SME) portfolios in the third quarter. Similarly, while there were some increases in underperforming loans, or stage 2 loans in accounting terms, a stable trend was observed by the end of the third quarter, albeit remaining above the peak of the pandemic. Notwithstanding this positive development, the path ahead remains uncertain, with some indications of increased risk, namely in the context of minor pockets of early arrears beginning to develop in some countries in the third quarter of 2022. This could indicate the build-up of heightened credit risk and a potential increase in NPL volumes in the near term. In this regard, there will be continued supervisory monitoring of developments in stage 2 loans, particularly in relation to banks exposed to sectors vulnerable to gas and energy price increases but also for portfolios, such as leveraged finance, consumer lending and real estate lending, which are sensitive to the fast-paced normalisation of interest rates. In this context, the energy price shock caused by the Russian war in Ukraine typically affected economic sectors involved in the production or processing of raw materials, energy suppliers and energy-intensive sectors. For some industries, the energy price shock could exacerbate pre-existing supply chain disruptions arising from COVID-19 restrictions in China and general microchip shortages. High input prices also weighed on construction and could additionally affect large-scale consumers of gas, such as producers of metals, chemicals, food and beverages. Supervisory activities focused on assessing banks’ actions to manage potentially vulnerable portfolios will continue.

Chart 3

Vulnerable sectors

a) Loans to vulnerable sectors

b) Stage 2 loan developments in vulnerable sectors

Source: ECB and ECB calculations.

Notes: Loans to vulnerable economic sectors as reported under AnaCredit. NFC stands for non-financial corporation as defined in paragraphs 2.45 to 2.50 of Annex A to Regulation (EU) No 549/2013.

Net interest income and trading income benefited from higher rates and volatility in a context of geopolitical tensions on energy and commodity markets

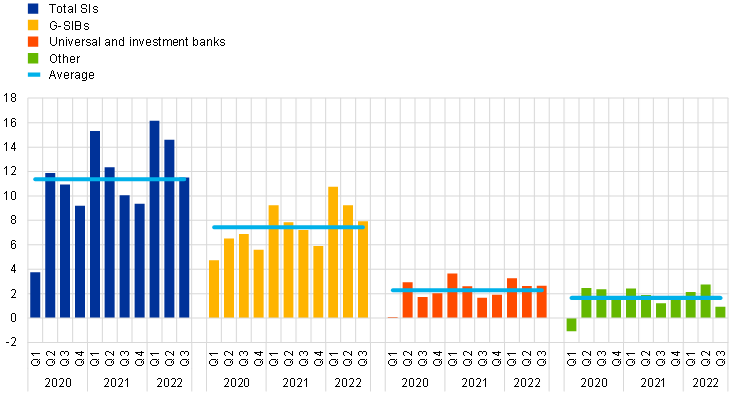

The acute geopolitical tensions observed in 2022 resulted in persistent inflationary pressures and volatility in energy and commodity prices. This had an impact on an already high inflation level, at a time when central banks were starting to normalise monetary policies, and contributed to the correction in equity markets. The subsequent fast-paced normalisation of interest rates provided a major boost to banks’ net interest income, which increased not only owing to expanding lending volumes, but also to increasing interest rate margins. Trading income, particularly for global systemically important banks (G-SIBs), generally profited from higher rates and higher volatility (Chart 4 and Chart 5).

Chart 5

Trading and investment income flows by selected business model

(quarterly flows in EUR billions)

Source: ECB.

Note: The sample for “average” includes all SIs at the highest level of consolidation within the SSM (varying sample); the “G-SIBs”, “Universal and investment banks” and “Other” samples denote the sub-samples within the respective business models.

Banks’ liquidity and funding positions remained sound in 2022, although monetary policy normalisation could be challenging

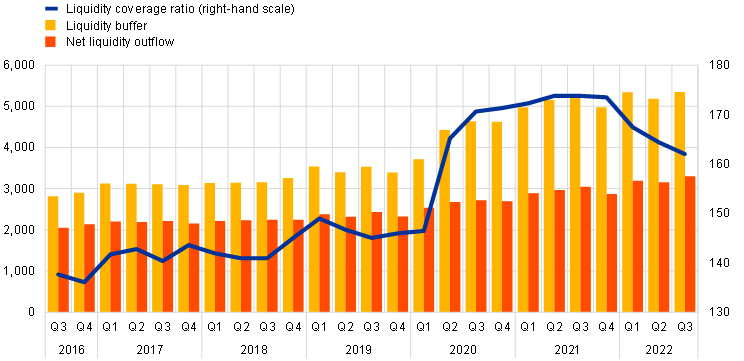

Liquidity and funding conditions for SIs continued to benefit from the monetary policy measures adopted in 2020 and 2021. As at 30 September 2022, the liquidity coverage ratio (LCR) stood at 162%, below the level observed at the end of 2021 but well above pre-pandemic levels and minimum regulatory requirements (Chart 6).

Chart 6

Developments in liquidity coverage ratio, liquidity buffer and net liquidity outflow

(left-hand scale: EUR billions; right-hand scale: percentages)

Source: ECB supervisory statistics.

Note: The sample includes all SIs at the highest level of consolidation within the SSM (varying sample).

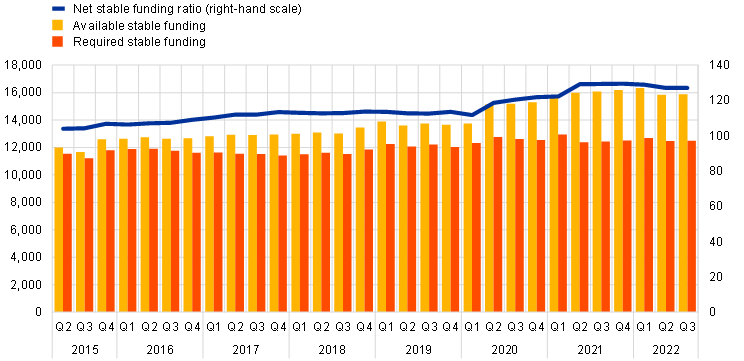

On the same date, the net stable funding ratio stood at 127.1%, broadly in line with the values observed in 2021, comfortably above pre-pandemic levels and minimum requirements (Chart 7).

Chart 7

Developments in net stable funding ratio, available stable funding and required stable funding

(left-hand scale: EUR billions; right-hand scale: percentages)

Source: ECB supervisory statistics.

Note: The sample includes all SIs at the highest level of consolidation within the SSM (varying sample).

As for LSIs, the respective supervisory metrics stood at 188.4% for the LCR and 130.2% for the net stable funding ratio, both slightly lower compared with the third quarter of 2021, but still significantly above regulatory thresholds.

In the last quarter of 2022, the ECB continued raising interest rates, changed the terms and conditions of the third series of targeted longer-term refinancing operations (TLTRO III) and offered banks additional voluntary early repayment dates starting from 23 November 2022. The normalisation of monetary policy will create a more challenging environment for bank funding and downward pressure on banks’ liquidity ratios.

As a result, 2022 was marked by the resilience of capital and liquidity ratios, along with improved asset quality and enhanced profitability. ECB Banking Supervision keeps a close eye on the distributional effects of these trends by continuing to monitor banks’ specific vulnerabilities. At the same time, it remains alert to potential uncertainties stemming from volatile markets or unexpected developments in the macroeconomic environment, such as a potential downturn, steeper interest rate increases or reinforced inflationary pressures.

Despite further business continuity challenges, the impact on operational risk has continued to be limited up until now

Over the course of 2022, the challenges linked to the pandemic and new hybrid working models being rolled out became less relevant. By contrast, the uncertainties stemming from the Russian war in Ukraine and the increasing geopolitical tensions meant that the environment for supervised banks continued to be challenging from an operational resilience point of view.

Banks with critical operations in countries directly affected by the Russian war in Ukraine implemented business continuity plans that proved to be robust during a fast-changing environment in the first phase of the war. These SIs were able to ensure protection, and where necessary the transfer of key staff, while at the same time continuing their operations. In some cases, critical operations were transferred to teams working in other locations, including in EU entities. The lessons learned during the COVID-19 pandemic played a key role in the efforts of institutions to quickly adapt.

As in previous years, in 2022 banks also showed the same trend towards digital transformation, which meant greater reliance on IT infrastructures and use of third parties, including cloud services for the delivery of critical services. While this trend certainly brings certain benefits for banks, it also comes with additional risks and challenges from an operational perspective, such as managing the increasing number and sophistication of cyberattacks and the potential concentration on a small number of critical third-party providers. For that reason, cyber risks and third-party dependencies remained a priority for ECB Banking Supervision (see Section 1.2.3.1 for more on emerging risks in IT and outsourcing) and continued work is required by banks to ensure they are resilient to potential operational disruptions from all hazards, including severe but plausible cybersecurity incidents, which could pose risks to the wider financial system[1].

The COVID-19 pandemic and the Russian war in Ukraine once again showed the importance of having sound governance arrangements in place, as well as internal control functions and data aggregation capabilities

As for supervised banks’ governance structures, the ECB emphasised the need for continued improvement in their governance frameworks. The COVID-19 pandemic and the Russian war in Ukraine showed once again the importance of having sound governance arrangements in place, as well as internal control functions and data aggregation capabilities.

More specifically, and with regard to the Russian war in Ukraine, ECB Banking Supervision identified a number of areas requiring particular attention: first, the capability of management bodies, as well as legal and compliance departments, to exercise strong oversight over the impact of sanction schemes; second, proper approval processes for client transactions, including proper risk data aggregation capabilities to identify critical exposures; and finally, some banks’ internal audit activities might need to be adapted to capture all relevant risks stemming from the changes in the current external environment.

The COVID-19 pandemic and the Russian war in Ukraine also amplified pre-existing weaknesses in a number of general governance and risk management arrangements. First, there continued to be shortcomings in data aggregation and reporting due to deficiencies in the effectiveness of data governance (e.g. insufficient independent validation of data quality) and data quality management procedures, fragmented IT landscapes, and the limited scope and ambitions of banks’ remediation projects. These setbacks can hinder banks’ decision-making processes. Second, several banks still needed to further improve their internal control functions, particularly to address insufficient staffing, the low stature of the function and deficiencies in processes (such as compliance monitoring programmes and the definition of banks’ risk appetite).

Moving the focus beyond crisis aspects, some banks continued to make progress following targeted measures by ECB Banking Supervision. This included specific areas such as collective suitability, the number of independent directors, committee structures, diversity policies and the level of involvement of non-executive directors. Nevertheless, some weaknesses remain in the majority of banks, namely: (i) the low level of involvement of the management body in its supervisory function and its ability to challenge strategic decisions in the areas most affected by the current crises; (ii) insufficient expertise in banking and risk management of non-executive directors in a few banks; (iii) insufficient promotion of diversity in some banks; (iv) low proportion of independent board members in some banks, which further hinders the ability of the management body in its supervisory function to constructively challenge executive directors. Increased supervisory scrutiny over those deficiencies is performed as part of the work on management body effectiveness and diversity (see Section 1.2.2.2).

1.1.2 General performance of banks under European banking supervision

The rebound in banks’ profitability in 2022 was driven by increased income and subdued cost of risk, but the outlook may be less positive as the macroeconomic environment deteriorates

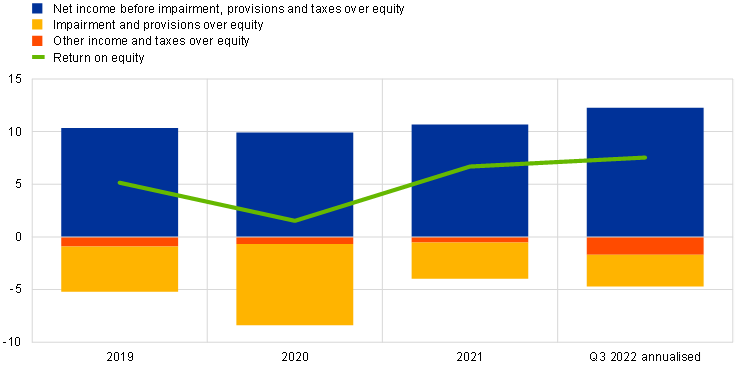

The profitability of SIs under European banking supervision showed strong resilience to the deterioration in the business environment related to the Russian war in Ukraine, supply chain disruptions and surging energy prices. Their aggregate annualised return on equity rose to 7.6% in the third quarter of 2022 (Chart 8) – the highest level recorded in several years, but still below banks’ average cost of equity. This increase was mainly driven by strong earnings largely related to rising interest rates, but it was also supported by a low cost of risk, as the adverse macroeconomic developments have not materially affected asset quality for the time being, and banks were also still able to benefit from provisions booked during the pandemic that they could redirect towards the current crisis.

Chart 8

Aggregate return on equity broken down by income and expense source

Increase in profitability driven by strong income supported by low impairments

(percentage of equity)

Source: ECB supervisory statistics.

Note: The sample includes all SIs at the highest level of consolidation within the SSM (varying sample).

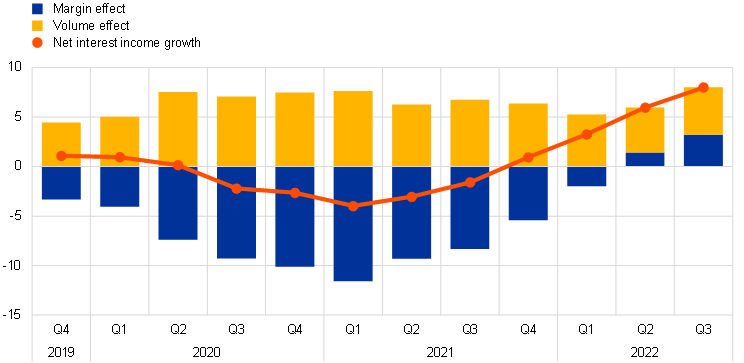

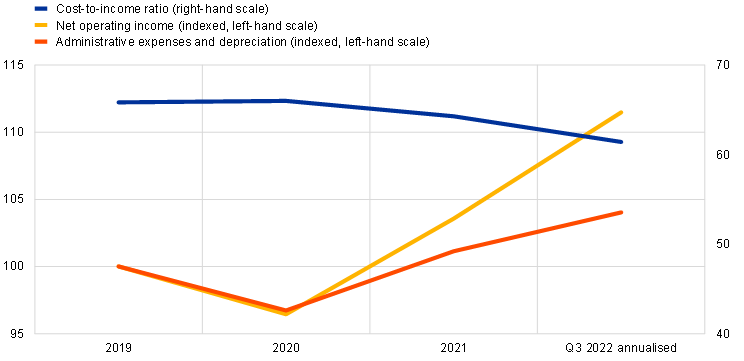

The increase in operating income was driven mainly by rising net interest income (+9.3% year on year), which benefited from an increase in margins supported by rising interest rates and a steepening yield curve, as well as from growth in lending volumes. By contrast, the total cost of funding and, namely, the cost of deposits of non-financial corporations increased notably over 2022, although this trend was heterogenous across banks. In the first three quarters of 2022, net fee and commission income was still higher than that of previous years, albeit with modest declines being recorded owing to the adverse impact of the deteriorating business environment on asset management and investment banking fees. The strong growth in income resulted in increased cost efficiency despite rising expenses: for each euro of income, banks needed to spend 61 cents as at the third quarter of 2022, compared with 64 cents in the previous year (Chart 9).

Chart 9

Cost-to-income ratio and indexed components

(percentages)

Source: ECB supervisory statistics.

Note: The sample includes all SIs at the highest level of consolidation within the SSM (varying sample).

On the cost side, administrative expenses and depreciations increased by 3%, primarily owing to increased staff expenses and IT-related costs as rising inflation percolated through the SIs’ cost structures. The increase in staff expenses was relatively modest, but as contractual wages are fixed in advance, inflation may affect this item further with some delay. Nevertheless, SIs maintained their broader strategic objectives of reducing expenses and investing in IT, even in the current environment as pandemic-related restrictions were gradually lifted.

Overall, banks’ profits were resilient to the slowing growth and benefited from rising interest rates. The pressure points on profitability included a potential increase in impairments and the need for valuation adjustments, higher operating expenses, a rise in the cost of funding, downward pressures on fee and commission income and insufficiently sustainable trading revenues. The first signs of increased pressure on profitability could be seen in SIs specialised in consumer credit.

Therefore, to consolidate and further improve the positive results achieved in 2022, banks should continue to actively steer their business models and focus their strategies on meeting sound risk-adjusted profitability targets. Supervisors continued monitoring the sustainability of banks’ business models in the light of short-term uncertainties and long-term structural challenges.

While LSIs’ profitability also improved against lower impairments in 2021, the first half of 2022 saw a reversal in some countries with negative other operating income

At first glance, the profitability of LSIs showed a different trend, with annualised return on equity decreasing to 1.3% after three quarters in 2022 (-4.3% year on year). The main driver behind this overall result was a substantial decline in net other operating income, however, this was largely attributable to developments in Germany. Here, banks experienced sizeable valuation losses as a result of rising interest rates and the impact of these on the securities portfolios under their respective accounting regime, which triggered book losses as a result of the strict lower-of-cost-or-market principle. In most countries, LSIs were actually able to improve their return compared with the previous year. The rise in interest rates had a positive impact on profitability in line with the general trend for SIs – both net interest income and net fee and commission income improved by 7.2% and 1.5% year on year respectively. Trading activities also recorded a material upsurge in net income (+89% year on year). Still, the cost-to-income ratio continued to increase and reached 85.6%, standing significantly higher by comparison with SIs, reflecting a material deterioration in net operating income. Administrative expenses and depreciations increased by 3.6% overall. At the same time, total assets increased slightly (3.2% year on year), driven by growth in corporate and retail loan business, further pushing down the return on assets to 0.12%, from 0.54% one year ago. As a result, the outlook for core income-generating capabilities temporarily improved, while higher expenses posed a risk to the LSI sector, especially in the light of continued regional discrepancies.

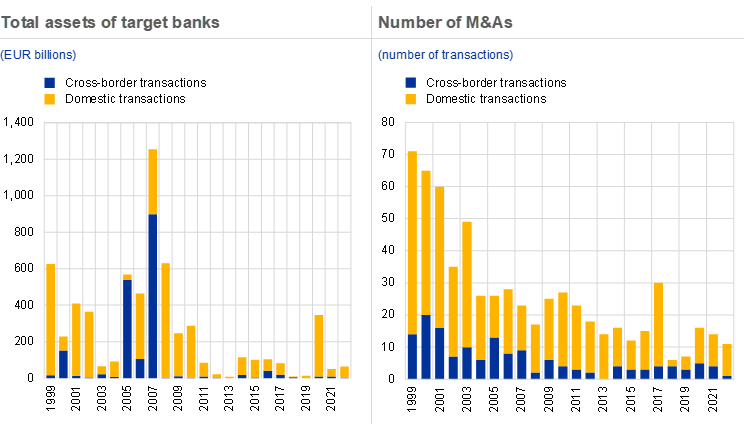

The deterioration in the macroeconomic environment, driven by geopolitical uncertainties and slowing growth prospects, has so far subdued banks’ efforts to further intensify M&A activity

Since the global financial crisis, the number of banks engaging in mergers and acquisitions (M&A) has been subdued. In line with developments globally, the value of M&A transactions, proxied by the total assets of M&A targets, fell by around two-thirds between the pre-crisis decade and the period since 2008, while the decline in the total number of transactions had been less steep.

More recently, over the course of 2020 and 2021, M&A activity appeared to gain some momentum, with banks more actively engaged in targeted consolidations at the level of business lines, such as leasing, factoring, wealth management, custody or securities services. Several of these business line acquisitions also included cross-border elements. For 2022, the deterioration in the macroeconomic environment, driven by geopolitical uncertainties and slowing growth prospects, has so far subdued banks’ efforts to further intensify M&A activity.

As in the past, fully fledged bank M&As are still predominantly domestic and involve smaller targets. However, some of the more targeted transactions featured a cross-border dimension and thus also contributed to financial integration within the EU. Another avenue to pursue cross-border integration would be for banks to review their cross-border organisational structures.

Chart 10

Total assets of target banks and number of M&As in the euro area

Source: ECB calculations based on Dealogic and Orbis BankFocus.

Notes: The sample includes M&A transactions involving SIs and LSIs in the euro area, excluding some private transactions and transactions between small banks not reported in Dealogic. Transactions associated with the resolution of banks or distressed mergers were removed from the sample. Transactions are reported on the basis of the year in which they were announced.

1.2 Supervisory priorities for 2022

1.2.1 Supervisory priorities for 2022: introduction

In 2022, while initially focused on vulnerabilities stemming from the pandemic, as well as other emerging risks, ECB Banking Supervision also broadened its scope of priorities to include risks posed by the rapidly changing macroeconomic environment

In 2022 ECB Banking Supervision focused its supervisory efforts on three different areas of priority to ensure that, first, banks emerge healthy from the pandemic (Priority 1); second, that they seize the opportunity to address structural weaknesses via effective digitalisation strategies and enhanced governance (Priority 2); and third, that they tackle emerging risks, including climate-related and environmental risks, exposures to counterparty credit risk, and IT outsourcing and cyber risks (Priority 3). Several supervisory activities designed to address these challenges were carried out in 2022, covering a wide range of banks and following a risk-based approach. ECB Banking Supervision also demonstrated flexibility by adjusting the scope, timing and intensity of its planned activities so as to tackle the emerging risks stemming from the Russian war in Ukraine, including high inflation and the subsequent monetary policy response.

1.2.1.1 Credit risk management frameworks and exposures to vulnerable sectors, including real estate

Effective credit risk management frameworks can help banks identify distressed borrowers and sectors at an early stage

On a positive note, the quality of banks’ assets continued to improve through a sustained reduction in the volumes of NPLs in the first half of 2022, with only minor increases in the SME and consumer portfolios up to end of the third quarter. These positive asset quality trends are highly welcome as the benefits of concrete bank action continue to be reaped following several targeted supervisory actions taken to combat credit risk over the past number of years. Positive credit quality developments, such as the continuing reduction in NPLs, contributed to marginal improvements in the average credit risk scores of banks for the 2022 Supervisory Review and Evaluation Process (SREP) cycle. While there are clear signs of efforts by banks to remedy identified deficiencies in the area of credit risk frameworks and controls, demonstrated by a decrease in the volume of related credit risk measures in the 2022 SREP, the pace of progress is still slow. As a result, the credit risk control scores remained low for the 2022 SREP.

Despite these positive trends, the changing credit risk environment, with its tighter financing conditions and an increasing risk of recession across Europe, is naturally holding back progress. This has had an impact on households, corporates and sovereigns to varying degrees, depending on factors such as their levels of indebtedness or sensitivities to the macro-financial environment. Therefore, the supervisory activities conducted to date and the supervisory expectations communicated since the outbreak of the pandemic with a view to tackling structural deficiencies in banks’ credit risk management frameworks remain relevant for addressing further challenges that may arise.

This is particularly relevant in the areas of loan origination and monitoring, forbearance flagging, the classification of distressed borrowers as NPLs and their provisioning frameworks, as well as in the area of vulnerable sectors. While most SIs developed concrete remedial action plans to address the gaps identified as part of the “Dear CEO” initiative[2] launched in December 2020, many of these gaps remain open. The expectation was that these deficiencies would be addressed by way of the credit risk work programme in 2023 and beyond. Furthermore, a horizontal analysis of credit risk patterns and trends carried out in 2022 found consistent evidence of this for the LSI sector.

Following a sharp price correction at the onset of the pandemic, conditions in commercial real estate markets continued to be of concern. This was particularly evident in the office and retail sub-sectors of the commercial real estate sector across Europe, which was challenged by rising interest rates and the surge in construction costs. Despite persistent signs of overvaluation in the euro area, residential house prices increased in the first half of 2022, further widening the gap with respect to rental prices. Coupled with the increase in the cost of living and the associated decline in real wages, this raised concerns of a sudden surge of NPLs, especially for those banks significantly exposed to residential mortgage loans with floating interest rates.

To shed light on banks’ preparedness to deal with a deteriorating commercial real estate market, and in line with the Recommendation of the European Systemic Risk Board on vulnerabilities in the commercial real estate sector in the European Economic Area, ECB Banking Supervision conducted a targeted review of the commercial real estate sector, focusing on the office and retail sub-sectors. Ad hoc data were collected to analyse the risk profile and materiality of these sub-sectors during an initial data gathering phase, which included 32 banks, with the sample size being narrowed down to 15 banks in the subsequent deeper qualitative phase. The key concerns identified through this exercise related to the effectiveness of banks’ credit risk management frameworks. In this respect, deficiencies were identified in most banks in terms of their assessments of borrowers’ repayment capacity at loan origination, particularly in the context of a more challenging environment characterised by increasing financing costs and stagnant rental income. Furthermore, the ability to identify emerging risks was also seen to be an area for improvement, chiefly because some banks’ frameworks did not sufficiently capture the forward-looking risk, and in some cases, also relied excessively on manual processes. As for the incorporation of climate risk into credit risk management, banks still lacked the necessary data to assess risk sufficiently, and there was heavy reliance on proxies to estimate missing “real” data. Detailed findings and requests for remedial action plans were subsequently issued to all banks included in this exercise, and the Joint Supervisory Teams (JSTs) were consistently engaged in this topic.[3]

A similar exercise was launched in the second quarter of 2022 on the residential real estate (RRE) sector. This focused on assessing potential risks embedded in existing exposures, addressing bank-specific gaps in the risk management of domestic RRE new lending business and, ultimately, on identifying credit risk management deficiencies and developing remedial action plans. The RRE sector is considered to be a material asset class on the balance sheets of significant banks. The sample for this exercise includes 29 banks, accounting for around 40% of SIs’ RRE exposures. The outcomes of the exercise are expected in the second quarter of 2023 and will be incorporated into the 2023 SREP exercise.

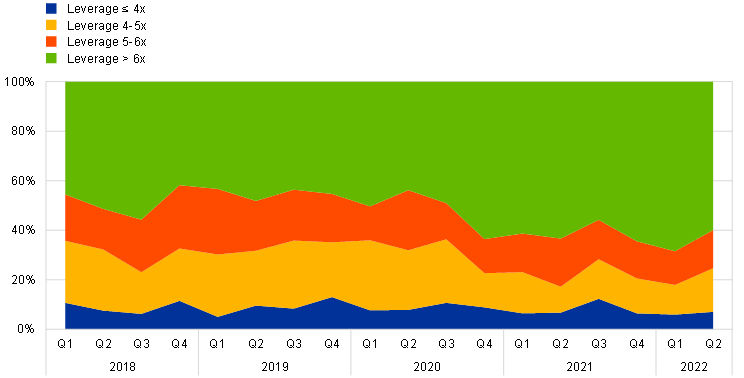

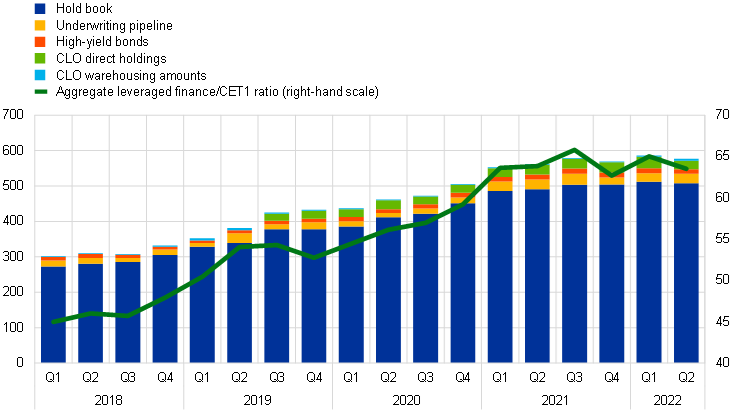

1.2.1.2 Exposures to leveraged finance

Over the past four years, the holdings of leveraged loans by SIs[4] under European banking supervision have increased, on an aggregated basis, by 80%, alongside an increase in the share of highly leveraged transactions[5] originated by SIs. This trend held until mid-2022, at which point SIs continued underwriting new syndicated loans. The exposure amounts of the SIs in the second quarter of 2022 were close to the record values posted in the fourth quarter of 2021. Since then, the primary market has shut down to a considerable extent. Substantial write-downs on corporate loan books held for sale were recorded by the largest players across Europe and globally.

Chart 11

Developments in leveraged transactions

Breakdown of underwritten volumes by leverage level

(share of total SI notional)

Exposure of euro area banks and share relative to CET1 capital, aggregate levels for supervised banks

(left-hand scale: EUR billions; right-hand scale: percentage of CET1 capital)

Sources: ECB Banking Supervision and ECB Leveraged Finance Dashboard.

Notes: Data are limited to a sample of SSM banks with the largest leveraged finance portfolios. CLO stands for collateralised loan obligations.

Since there were also concerns about increasing risk-taking in the leveraged finance segment during the pandemic, in March 2022 the ECB decided to send a “Dear CEO” letter on leveraged transactions to SIs. The aim of the letter was to further clarify the ECB’s expectations concerning the risk appetite framework for leveraged transactions and, in effect, to operationalise the ECB’s guidance on leveraged transactions that was published in 2017.

The responses to the letter confirmed that there were significant deficiencies in both the robustness of banks’ overall risk appetite frameworks and their management of market risk. The JSTs are currently working closely with individual banks to discuss how they can effectively close the gaps identified and meet the expectations.

The ECB has already started to apply capital charges to a few banks where the risks associated with leveraged lending activities were perceived to be excessively high – either because of the level of very high-risk exposures, weaknesses in risk management practices, or both. The ECB will continue to apply any necessary capital charges through the SREP exercise in the course of 2023. These charges reflect insufficient progress made by banks in meeting the expectations set out in the aforementioned guidance and will only apply as long as the identified deficiencies persist.

1.2.1.3 Counterparty credit risk

With market, economic and geopolitical uncertainties on the rise, ECB Banking Supervision sharpened its focus on banks’ counterparty risk management capabilities

The “low for long” interest rate environment which prevailed until 2022 fostered search-for-yield strategies by many types of investors. As a result, some banks increased the volume of the capital market services they provided to more risky and less transparent counterparties, often non-bank financial institutions, including through significant leverage.

Coupled with an increase in volatility across several markets (e.g. energy and interest rates) and a normalisation of monetary and financial conditions over the course of 2022, the material impact that counterparty bankruptcies (e.g. hedge funds and family offices) previously had on some banks in 2021 drew attention to risks stemming from weak governance or inadequate risk management practices by third parties.

With this in mind, and in line with its supervisory priorities, ECB Banking Supervision took a range of measures to fend off potential risks in this area. First, the ECB published an article in its Supervision Newsletter in August 2022 outlining its supervisory expectations for prime brokerage services. Second, from April to October 2022 the ECB conducted a targeted horizontal review focused on governance and risk management of counterparty credit risk across a wider sample of banks active in derivatives and securities financing transactions, including both non-bank financial institutions and non-financial counterparties. Third, on-site inspections were conducted for selected institutions.

Overall, although banks have made progress in terms of identifying, measuring and controlling counterparty credit risk, there are still several material shortcomings in key areas such as due diligence, definition of risk appetite, stress testing, risk mitigation and default management, both in the light of supervisory expectations and good practices observed in the industry. Looking ahead, the JSTs will continue to engage with banks in the course of 2023 to remedy deficiencies in those areas which have been identified as more material.

1.2.1.4 Sensitivity to interest rate and credit spread risks

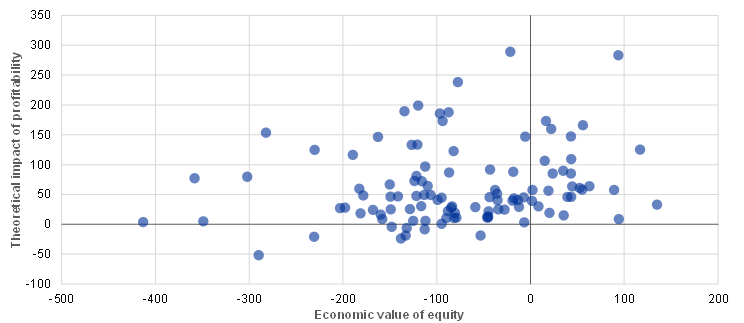

Most banks profited from increasing interest rates, but improvements in risk management are necessary

In 2022 the ECB carried out a review of interest rate and credit spread risk management practices among a sample of SIs particularly exposed to those risks. For most banks, an upward 200-basis point interest rate shock (Chart 12) would have a positive impact on profitability, even under a baseline scenario of an economic slowdown such as the one included in the ECB staff macroeconomic projections. As for potential increases in provisions reflecting the difficulties faced by borrowers, the ECB’s most recent analyses show that negative impacts on capital adequacy would remain, on average, fairly muted even with shocks of up to 300 basis points.

Irrespective of the applicable prudential and accounting regimes, banks should be mindful of the typically negative impact of rising rates on their economic value of equity. They should adopt sound and prudent asset and liability management modelling practices in order to capture shifts in consumer preferences and behaviour when interest rate regimes change. They should also carefully monitor risks arising from hedging derivatives.

Credit spread risk should be appropriately measured and managed, including for sovereign debt securities and other instruments accounted for at amortised cost. In particular, the calibration of internal stress tests should reflect the severity of historical stress episodes.

Interest rate and credit spread risks can have a material impact on LSIs as well

The considerations above also apply to LSIs, for which exposure to interest rate and credit spread risk can be very relevant. The concrete impact of the sudden shift in interest rates depended not only on the open risk position, but also on the applicable national accounting framework. Some banks were affected by significant valuation adjustments to their securities portfolios that needed to be reflected in the profit and loss statements, thus reducing regulatory capital. Over the medium term, the impact on profitability and capital will depend on the decision to sell the securities or hold them until maturity and, of course, on future developments in interest rates.

Chart 12

Impact of a 200-basis point increase in interest rates on significant institutions

Theoretical impact of profitability and economic value of equity on CET1 ratio

(basis points)

Sources: ECB calculations and short-term exercise data as at 30 June 2022.

Box 2

Follow-up on Brexit: outcome of the desk-mapping review

Integrating Brexit banks into European banking supervision

The key overarching objective of this project was to ensure that all significant institutions have prudent and sound risk management frameworks in place, as well as a local presence which enables effective supervision commensurate with the risks that they take.

On 1 January 2021, the United Kingdom left the single European market. From the EU’s perspective, the United Kingdom is now a third country. UK-based banks wishing to provide services within the EU can no longer do so via passporting, i.e. the right of a bank to serve customers across the EU from one of its Member States, either through the free provision of services or by establishing local branches under preferential terms.

The desk-mapping review, in other words, the review of booking and risk management practices across trading desks active in market-making activities, treasury and derivative valuation adjustments, is aimed at ensuring that third-country subsidiaries have adequate governance and risk management arrangements in place and do not operate as empty shells. The desk-mapping review was initiated because ECB Banking Supervision found that (i) banks had not made sufficient progress in ensuring adequate local trading presence and risk management capabilities in their newly established entities in the euro area; and (ii) banks needed clearer instructions in order to appropriately implement the target operating models previously agreed with their Joint Supervisory Teams. In this respect, ECB Banking Supervision closely collaborated with other supervisory authorities, particularly those in the United Kingdom, to make sure that the rationale behind its supervisory policies was properly understood by all parties involved.

As the supervisor for the euro area, it is the ECB’s duty to protect its depositors and other creditors of local legal entities, prevent the disruption of banking services and safeguard broader financial stability in its area of jurisdiction. In this context, empty shell structures – legal entities located in the euro area that book exposures remotely with their parent entity or book them locally, but rely fully on risk management hubs and financial infrastructures located in third countries, often by means of back-to-back mirror transactions and hedges transferring the risk to their parent entity – are a very real concern.

First, these structures are exposed to heightened operational and counterparty risk vis-à-vis their parent affiliate. In the event of financial stress or default at the level of the parent entity, the local entity can be left with large unhedged positions and little to no access to the staff and infrastructure needed to wind them down smoothly. This, in turn, undermines both the local entity’s recovery capacity during severe stress and, where applicable, its resolvability. This is particularly relevant under a third-country framework where, during episodes of financial stress, the diverging interests of the numerous entities and stakeholders involved may lead to retrenchment and ring-fencing. Second, even during normal times, having risk management resources and infrastructure located offshore can hinder a bank’s ability to identify, measure and monitor risk and can make governance and decision-making less transparent. Third, reallocating risk and revenue to third-country affiliates can worsen the incentive structure for local bank management.

The first phase of the desk-mapping review, which was launched across seven institutions and affiliated investment firms, found that incoming banks did not yet retain full control over their balance sheets, as required under the ECB’s 2018 supervisory expectations. Some 70% of the trading desks assessed still implemented a back-to-back booking model and around 20% were organised as split desks, whereby a duplicate version of the primary trading desk located offshore was established within the euro area legal entity to manage the part of the risk originated there.

The supervisory scrutiny applied by the ECB in response to these findings was purely risk-based and took a proportionate approach based on materiality. 56 trading desks warranting supervisory action were identified based on a common set of risk indicators. Following this materiality assessment and its engagement with supervised entities in the course of 2022, the ECB will issue/issued individual binding decisions which may require incoming banks to (i) appoint a head of desk within the euro area legal entity with clearly defined reporting lines and a compensation structure linked to the performance of that entity; (ii) ensure the desk has the adequate infrastructure and number and seniority of traders to manage risk locally; (iii) establish a solid governance and internal control framework of remote booking practices with parent affiliates; and (iv) ensure limited reliance on intragroup hedging.

The review of trading desks and their associated risks does not mark the end of the supervisory scrutiny of incoming banks’ post-Brexit operating models. Investigations into credit risk-shifting techniques, the reliance on parent entities for liquidity and funding, and internal model approvals are still ongoing.

1.2.2 Business model sustainability and governance

1.2.2.1 Banks’ digital transformation strategies

One of the supervisory priorities for 2022-24 was to address the challenges posed to banks by digital transformation.

Banks’ management bodies are chiefly responsible for setting strategic objectives for digital transformation and using innovative technologies. The focus of ECB Banking Supervision was to assess banks’ capabilities to develop and implement digital strategies that are adequate to strengthen their business model sustainability and prudently address related risks. Enhancing supervisory understanding of market developments and keeping pace with the impact of a fast-evolving technological landscape also remained a priority.

A survey on digitalisation collected information which was previously not available in a consistent manner across SIs; the results will benefit various supervisory activities

This is why ECB Banking Supervision took major steps to address these topics in 2022. Following a high-level dialogue with some of the leading market counterparts (as part of a market intelligence initiative) to understand market trends, all SIs were requested to respond to a survey on digital transformation and the use of fintech. This survey collected information which was previously not available in a consistent manner across SIs, and some of the national competent authorities (NCAs) also used the survey for some of their LSIs.

A system-wide overview of the main takeaways from the survey is featured in the February 2023 Supervision Newsletter, together with a link to the aggregated findings. In general, the survey findings confirmed that banks are increasingly digitalising and using innovative technologies, thereby transforming the way financial services and products are being delivered. Banks consider these to be essential elements for maintaining market shares and boosting their profitability. To achieve their digital transformation strategy objectives, banks tend to rely on outsourcing and external partnerships in an environment marked by competition to attract, retain and develop IT and digital expertise. However, as banks open up their IT infrastructures, they face heightened risks in terms of third-party dependency and cybersecurity. These risks require further monitoring and must be taken into account in banks’ governance and risk appetite frameworks.

Having said that, the responses are heterogenous, as there seems to be no common understanding of what digital transformation really means – it remains a very general concept relating to business models, processes and cultural change that is enabled by technologies. Therefore, further investigations and inspections are to be conducted in this area over the coming years.

The overall outcome of the survey will be instrumental for (i) developing guidance for supervisors to assess banks’ risks and best practices; (ii) identifying risks in specific supervised entities or technology use cases that require further targeted scrutiny; and (iii) potentially establishing further supervisory expectations. It will also be relevant for shaping the SREP methodology for the business models and governance underlying the use of new technologies.

ECB Banking Supervision also continued its efforts to actively shape digitalisation for the future European and international regulatory framework by further engaging with European Supervisory Authorities and international standard-setting bodies on the regulation of various aspects related to digitalisation and innovation in the financial sector. Moreover, ECB Banking Supervision continued to participate in discussions on the regulatory scope and legislative proposals made in the context of the digital finance strategy for the EU, such as the Markets in Crypto-assets Regulation[6], the Digital Operational Resilience Act[7] and the Artificial Intelligence Act[8].

1.2.2.2 Deficiencies in management bodies’ steering capabilities

Sound governance arrangements, robust internal controls and reliable data are essential for fostering adequate decision-making and mitigating excessive risk-taking both during normal times and in times of crisis. Despite the progress achieved by banks over the past few years in this area, supervisors continue to see a high number of structural deficiencies in internal control functions, management bodies’ functioning, and risk data aggregation and reporting capabilities.

This is why ECB Banking Supervision has been involved in several activities dedicated to achieving progress in this area, in particular with a view to strengthening internal governance and strategic steering capabilities. Over the period 2022-24, these activities will include targeted reviews of banks with deficiencies in the composition and functioning of their management bodies, on-site inspections, targeted risk-based fit and proper (re)assessments, the development of an approach to reflect diversity in fit and proper assessments, and the update of the 2016 supervisory statement[9], as well as data collections.

In 2022 ECB Banking Supervision finalised a data collection on banks’ management body composition and functioning. The exercise revealed that the level of formal independence within banks’ management boards was increasing but could be further improved in a number of cases. Furthermore, this exercise revealed that diversity in terms of both gender and expertise (especially in areas such as IT), which has long been recognised as crucial for effective governance, could still be improved. The need to have better succession planning policies for management boards was another area for further development. ECB Banking Supervision followed up on these findings in the context of the 2022 SREP by requesting banks which still had no diversity policy or diversity targets to put such frameworks in place. In this regard, the supervisory expectations communicated to banks made it clear that targeted policies should incorporate ratios for the underrepresented gender at banks’ management body level and include several dimensions such as age, gender, geographical origin, as well as educational and professional background, respectively. The JSTs are following up on banks’ implementation of such frameworks as part of their ongoing supervisory activities.

Governance arrangements are important for all banks regardless of their size. For this reason, ECB Banking Supervision also conducted a thematic review of the governance arrangements in place for LSIs[10] in 2021-22, using data from a sample of more than 200 LSIs across 21 participating countries. The results revealed several weaknesses in LSIs and underlined the importance of continuous improvement, facilitated by an ongoing dialogue between supervisors at all levels. ECB Banking Supervision and national supervisors will continue to promote greater alignment of European supervisory expectations and standards for internal governance, addressing any identified weaknesses along the way.

1.2.3 Emerging risks

1.2.3.1 IT and cyber risk

IT and cyber risk continued to be a key risk driver for the banking sector in 2022

Despite the Russian war in Ukraine, the number of cyber incidents reported to the ECB remained relatively stable in the first three quarters of 2022 by comparison with the same period of 2021.

ECB Banking Supervision conducted a number of off-site and on-site supervisory activities around IT and cyber risk in 2022 with the following takeaways: first, banks still showed room for improvement in terms of implementing basic cybersecurity measures, with around half of the severe findings being identified during IT risk on-site inspections conducted in 2022 and concentrated in the area of IT security and cybersecurity risk. Second, after some years of a steady increase, the reliance on end-of-life systems stabilised, albeit at a very high level. Third, data quality management remained the least refined risk control area and some of the key controls were not yet fully implemented in several banks. Fourth, the number of critical projects with an impact on the IT landscape increased very considerably, pointing to the clear relevance of having appropriate management procedures in place for IT developments and IT projects.

Furthermore, for the first time, ECB Banking Supervision was able to collect all of the outsourcing registers from SIs in 2022. A preliminary analysis of this information confirmed the high relevance of this topic: banks reported around 60,000 active outsourcing contracts, half of which covered their critical functions. While around 40% of all such contracts are related to ICT services, banks use outsourcing arrangements for all kinds of critical functions such as internal controls, customer and administrative services, payment services or cash management, among others.

The information collected on third-party dependencies also helped to identify certain emerging risks and challenges that needed to be properly managed, including the existence of several critical service providers difficult to substitute, the significant operational dependency of banks on companies from and services provided by non-EU countries, as well as a significant number of contracts that were still not fully aligned with either the European Banking Authority (EBA) Guidelines or the ECB’s supervisory expectations in this respect.

In 2022 ECB Banking Supervision also contributed to the activities of international working groups on IT and cyber risk, including those led by the EBA, the Basel Committee on Banking Supervision and the Financial Stability Board, and to the work around new regulatory proposals, such as the Digital Operational Resilience Act[11].

Overall, these developments underline the need for banks to continue improving their operational resilience framework to ensure appropriate business continuity, including that of their critical services, in an increasingly complex environment, as well as to adjust to the new and forthcoming regulatory requirements.

1.2.3.2 Climate-related and environmental risks

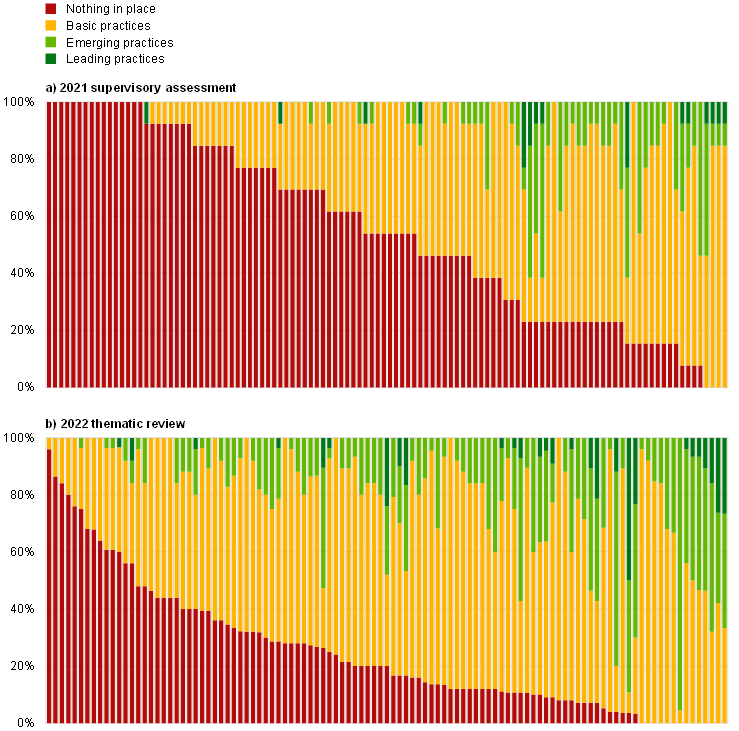

Following the publication of the ECB Guide on climate-related and environmental risks in November 2020, the ECB launched a range of supervisory exercises to assess banks’ capabilities to manage climate-related and environmental (C&E) risks and align their practices with supervisory expectations. Following the review of banks’ self-assessments and implementation plans in 2021, the ECB followed up with a thematic review in 2022. In the 2022 thematic review, the ECB evaluated the soundness and comprehensiveness of institutions’ key policies and procedures, as well as their ability to effectively steer their C&E risk strategies and risk profiles.

The review was conducted in tandem with the first supervisory stress test on climate-related risk (see Box 3) and complemented by a targeted review on commercial real estate and dedicated on-site inspections. The thematic review was conducted by the ECB and 21 NCAs and covered 107 SIs and 79 LSIs.

For over half of the banks significant concerns were expressed about their ability to effectively implement their strategies and process

The thematic review demonstrated[12] first that most institutions have now devised an institutional architecture to address C&E risks, having clearly built up capacity over the last year (Chart 13). Moreover, there was growing acknowledgement of the materiality of these risks and a broad set of good practices were being used in a variety of institutions. The ECB published a collection of good practices in a dedicated compendium[13] in order to respond to a request from the banking sector for further insight into good practices and to demonstrate that swift progress is possible. Notwithstanding this, virtually all institutions needed to make far-reaching and enduring efforts to align their practices with supervisory expectations. Generally, the approaches taken still lacked methodological sophistication, the use of granular information on C&E risk and/or active management of the portfolio and risk profile accordingly. Notably, blind spots in identifying C&E risks were revealed in 96% of institutions and for over half of the institutions significant concerns were expressed about their ability to effectively implement their strategies and processes.

Furthermore, in March 2022 the ECB published an updated assessment of the progress banks had made in disclosing C&E risks, as set out in the ECB’s November 2020 Guide. Although improvements had been made since the ECB’s first assessment in late 2020, no bank fully met the supervisory expectations. Compared with 2020, more banks were now able to disclose meaningful information on C&E risks. However, the overall level of transparency was still insufficient. Roughly 75% of the banks did not disclose whether C&E risks had a material impact on their risk profile, even though around half of the banks that failed to do so indicated to the ECB that they viewed themselves as exposed to such risks. And almost 60% of the banks in the sample did not describe how transition risk or physical risk could affect their strategy. The ECB sent individual feedback letters to banks explaining their main shortcomings and expecting them to take decisive action. This was also done to help banks prepare for new regulatory requirements such as the binding standards on Pillar 3 disclosures of environmental, social and governance risks. The ECB began reviewing banks’ C&E disclosures again at the end of 2022, with the results planned for publication in the course of 2023.

Following up on the various supervisory exercises, the ECB sent individual feedback letters to all SIs, setting institution-specific deadlines to gradually meet all supervisory expectations by the end of 2024.[14] The deadlines will be closely monitored and, if necessary, enforcement action will be taken. The ECB had already included bank-specific C&E findings in the SREP, whereby it imposed binding qualitative requirements on more than 30 banks, leading, for a small number of banks, to an impact on their SREP scores and, hence, an indirect impact on Pillar 2 capital requirements.

Chart 13

Results of the 2021 and 2022 supervisory assessments

Level of maturity of practices across areas of supervisory expectations (bank-by-bank)

(percentages of areas of supervisory expectations)

Source: “Walking the talk – banks gearing up to manage risks from climate change and environmental degradation”, ECB, November 2022.

Notes: The 2021 supervisory assessment scores are taken as a proxy to indicate the level of maturity of institutions’ practices in 2021. Owing to the updated assessment methodology used in the 2022 thematic review, direct comparison with the results from 2021 is indicative only.

Box 3

ECB climate risk stress test

In 2022 the ECB conducted a climate risk stress test (CST) as part of its annual supervisory stress test. Given the novelty of the exercise and the need for specific data and models to analyse climate-related risks, the 2022 CST should be seen as a learning exercise for both banks and supervisors and as a tool to enhance climate stress-testing capabilities in the industry. Hence, no direct capital implications were derived, although qualitative findings from the exercise were used as input for the Supervisory Review and Evaluation Process (SREP).

Structure of the exercise and scenarios