In 2021 we continued to contend with the effects of the coronavirus (COVID-19) pandemic on our economies and lives. The strong and coordinated policy responses to the pandemic crisis, coupled with progress in the roll-out of vaccinations, underpinned the rapid pace of the recovery during the year. Economic output in the euro area reached its pre-pandemic level by the end of 2021.

Unlike in previous crises, the banking sector was in a strong financial position to support the economy and help strengthen our policy responses. Measures taken by ECB banking supervision ensured that banks could smoothly transmit our monetary policy actions, aimed at preserving favourable financing conditions for all sectors of the economy. Taken together, the responses of monetary policy and banking supervision are estimated to have saved more than one million jobs.

But despite the unusually fast recovery, we now need to prepare for post-crisis challenges. The full impact of the pandemic will become visible only gradually. And as the true financial health of firms in some sectors more vulnerable to the pandemic comes to light, asset quality could be affected. European supervision is therefore keeping a close eye on the build-up of credit risks.

At the same time, the pandemic has led to more fundamental changes in the landscape in which banks operate. Digitalisation has accelerated and the urgency to tackle climate change has increased. Long-standing issues related to weak profitability and overcapacity could limit the ability of some banks to adapt and stay competitive in facing the digital and green transitions. The necessary response has two parts.

One is for banks to improve their cost efficiency and refocus their business models towards resilience and longer-term value creation. This includes making further progress in embedding climate-related and environmental risks into their existing strategies and risk management processes. Banks are still a long way off meeting our supervisory expectations in this field.

The second part is completing the banking union. A more robust, integrated and diversified financial sector would help unlock the large pool of private investment in Europe that is needed to accelerate the digital and green transitions.

I am confident that this is possible. Just as the banking sector has contributed to a successful solution to this crisis, it can also help get our economy ready for a greener and more digital future.

Introductory interview with Andrea Enria, Chair of the Supervisory Board

What was 2021 like for ECB Banking Supervision?

The pandemic continued to pose challenges for everyone in 2021, supervisors included. I am impressed with the operational resilience that the ECB as an institution has shown during the pandemic. Although we were still unable to conduct as many on-site inspections as we would have liked, our supervision remained effective. The frequency of our interactions with banks was relatively unabated too, even though most took place in remote working mode. We had good discussions within the Supervisory Board and were able to easily reach a consensus on most matters. Despite the difficulties raised by the pandemic, we managed to increase collaboration and team work across business areas within the ECB, within European banking supervision and between the ECB and the national competent authorities (NCAs). But I am keen to meet colleagues in person again and to restart visits to NCAs, face-to-face meetings with bankers and on-site inspections.

As uncertainty about the future decreased and the macroeconomic outlook improved in the course of 2021, we lifted most of the extraordinary measures we had put in place to enable banks to deal with the immediate impact of the crisis. In addition, we resumed the regular Supervisory Review and Evaluation Process (SREP), after having adopted a pragmatic approach in 2020 to focus on the challenges raised by the pandemic. For the first time we looked at climate risks in a structured way, mapping how much banks’ practices still diverge from our supervisory expectations. And, after five years of intense work, we completed our targeted review of internal models, marking a milestone in restoring reliability and consistency in the use of internal models for regulatory purposes. 2021 was also the year in which we took on the supervision of systemic investment firms in countries participating in the banking union. Our supervisory work was always coupled with efforts to clearly communicate our expectations to banks and other market participants, with a view to making our policies more transparent and sharing the progress made in achieving our supervisory objectives. Finally, we trialled an innovative process for setting priorities for supervisory work, which should enable our teams to focus more on the key risks and less on burdensome box-ticking tasks.

We are now two years into the pandemic. How do you think banks have fared during this period?

Since the outbreak of the pandemic European banks have shown strong resilience overall. I see this as the result of the post-financial crisis reforms, our long-standing efforts to strengthen banks’ capital, asset quality and liquidity buffers, and the prompt deployment of extraordinary public support measures. Banks’ capital ratios have remained resilient throughout this period, and they have been able to continue extending credit to households, small businesses and corporates. As yet, there has been no clear evidence of a deterioration in asset quality.

Although the macroeconomic projections for the euro area are generally positive, there is still uncertainty about how the pandemic will evolve. In particular, in some sectors more vulnerable to the pandemic, signs of latent credit risk have been observed. In addition, supply chain disruptions are weighing on trade and overall economic activity. Leverage in the financial system has also been on the rise and since some of our banks are exposed to it, we need to remain vigilant. Interest rate and credit spread adjustments along the path to recovery could increase credit risk for many banks and also harm those lenders that are particularly exposed to highly leveraged non-bank financial institutions. This deserves close attention.

But all in all, I would say that European banks have proven to be resilient in the face of a very serious crisis, and are in a much better position than they were after the 2008 crisis.

What do you think are the main challenges ahead for European banks? Is the COVID-19 crisis mostly behind them?

Thankfully, the macroeconomic outlook improved in 2021, and we are no longer expecting the wave of non-performing loans that we feared at the onset of the pandemic. That being said, banks should not lower their guard. The positive developments of 2021 prompted banks to reduce their provisioning significantly from the peak levels seen in 2020. But assessing the level of risk remains challenging, and the outlook still points to signs of latent credit risk. The share of underperforming loans did not recede in 2021. In accommodation and food services, as well as the air transport and travel-related sectors, underperforming loans continued to increase substantially during the year. So we will continue encouraging banks to tackle credit risks proactively and to keep a close eye on their loan books for any potentially material deterioration in asset quality.

In addition, some banks have increased their exposures to highly leveraged corporate counterparties, beyond our previously communicated supervisory expectations, and some are indirectly exposed to leverage through hedge funds and other non-bank financial institutions. These banks are particularly exposed to sudden interest rate and spread adjustments, which may materialise if the exit from the low interest rate environment turns out to be bumpy. If that is the case, we may witness significant corrections in asset prices and spreads, costly deleveraging and unexpected channels of direct and indirect contagion.

Moreover, too many European banks are still struggling with low profitability and heavy cost structures – the aggregate dynamics of the cost-to-income ratio since 2015 point to an enduring inefficiency problem in the European banking sector.

On the upside, several banks have recently embarked on comprehensive and tech-driven cost optimisation programmes, although these efforts will take time to translate into improved profitability and cost efficiency indicators. We have urged banks to refocus their business models towards long-term value creation, as robust and steady revenue generation capacity is the first line of defence in challenging business environments. The sustainability of banks’ business models continues to be one of our supervisory priorities. In 2021 we launched a series of inspections on business models and profitability, and these will continue throughout 2022.

Moving on to digitalisation in the banking and non-banking sector – how are banks dealing with the heightened competition it brings on the one hand, and the increase in customer demand for digital products on the other?

Digital transformation has accelerated during the pandemic and is changing the competitive landscape for good. There will be winners and losers, also in the banking sector. Effective strategic management, the volume and quality of IT investments and decisive actions to improve cost efficiency have proven to be key ingredients for success. More specifically, banks that have been successful in their digital journey have invested in modernising their IT infrastructures and optimising processes, and simplified and digitalised a number of internal procedures.

At the same time, the use of new technologies poses new challenges, not only to banks, but also to supervisors and regulators. Banks are increasingly exposed to IT and cyber risks. For the ECB to have a clear picture of these risks, we need our supervisors to be fully trained in this area as well. And in the same spirit, supervision should also embrace digital transformation: in 2021 we continued to roll out an array of suptech tools to make the work of supervisors across the banking union more effective and efficient.

Climate and environmental (C&E) risks gained prominence in 2021. Do you think European banks are prepared to tackle the expected increase in these risks?

In 2021 the ECB made notable progress in encouraging banks to become more proactive in their management of climate risks. We asked them to conduct self-assessments of their preparedness to deal with these risks, and we benchmarked their replies. We discussed our findings with the banks as part of our ongoing supervision, and published a report which describes some of the best practices we identified during this exercise. The bad news is that, according to the banks’ estimates, 90% of their practices were either partially or not at all compliant with our supervisory expectations.

But banks have started to reflect C&E risks in their current structures, and roughly half of them are adapting their governance arrangements accordingly. In 2022 we will continue our work on C&E risks by conducting a dedicated thematic review within the SREP and a supervisory climate stress test. These will serve as learning exercises both for us as the supervisor and for the banks, and will lay the groundwork for including C&E risks in our SREP methodology in a more structural manner.

You mentioned that the ECB has been taking further strides to increase its transparency. What progress did you make in 2021?

ECB Banking Supervision has always been committed to this goal and in 2021 we made our supervisory methods and outcomes more transparent in a number of ways.

In the context of the 2021 stress tests, we took two big steps towards greater transparency. For the first time, we published the high-level individual stress test results of banks that were not in the sample for the EBA’s EU-wide stress test, as well as the outcome in terms of banks’ Pillar 2 guidance by bucket. We hope that the additional details we provided on the new methodology for Pillar 2 guidance foster a better understanding of the use of stress test results within the SREP.

Moreover, we provided more detailed information on how we set our supervisory priorities for the next three years. We have clearly laid out our risk map for the future, linking each identified vulnerability to a concrete supervisory priority. This also guides how ECB Banking Supervision as a whole allocates its resources for this period.

Moreover, we have sought to improve the transparency of our work on C&E risks by publishing the results of the benchmarking exercise on banks’ preparedness, which I mentioned before, and sharing good practices within the industry. This is particularly important for a risk category that is in its infancy and for which substantial progress is needed very soon.

We also revised our Guide to fit and proper assessments. Besides introducing the concept of individual accountability, we focused on board members’ expertise in C&E risks and highlighted the importance of diversity – including gender diversity – in the composition of bank boards.

Finally, we revamped the ECB’s banking supervision website to make it easier and more intuitive to navigate for the public and for banks, with a simplified portal for banks and a streamlined whistleblowing platform.

Overall, I am very pleased with the progress achieved in 2021, especially when we consider that we were dealing with a unique crisis while working remotely most of the time.

1 Banking supervision in 2021

1.1 Supervised banks in 2021: performance and main risks

Overall resilience of the banking sector

Significant institutions entered the COVID-19 crisis with strong capital positions, which they maintained in 2021

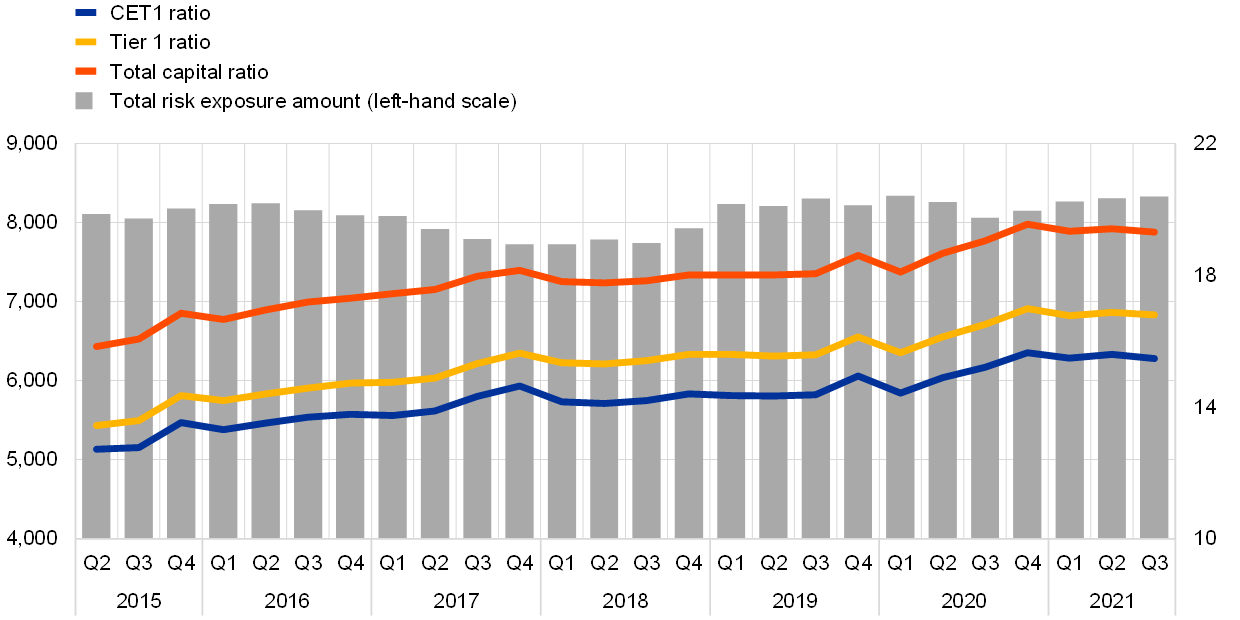

Significant institutions (SIs) under European banking supervision entered the coronavirus (COVID-19) crisis with strong capital positions. After a slight dip in the first quarter of 2020, the aggregate Common Equity Tier 1 (CET1) ratio reached 15.6% in the fourth quarter of 2020 and stabilised at this level in 2021 (Chart 1). Banks’ resilience during the crisis can be attributed to several factors, notably the public support measures implemented to protect customer solvency and facilitate access to credit, the strongly accommodative monetary policy response, and the timely supervisory and regulatory measures taken in response to the crisis. In addition, in March 2020 ECB Banking Supervision recommended that banks not distribute dividends or buy back shares and, in December 2020, that they limit such distributions. This allowed banks to strengthen their capital base amid relative uncertainty about the magnitude of potential credit losses. In June 2021, with macroeconomic forecasts pointing to an economic rebound and reduced uncertainty, the ECB decided not to extend its recommendation beyond September 2021. Instead, supervisors went back to the pre-pandemic practice of assessing the capital and distribution plans of each bank as part of the regular supervisory dialogue. Banks are expected to remain prudent when deciding on dividends and share buy-backs and to carefully consider their medium-term capital projections and the sustainability of their business models.

Chart 1

Capital ratios of SIs (transitional definition)

(left-hand scale: EUR billions; right-hand scale: percentages)

Source: ECB.

Note: The sample includes all significant institutions at the highest level of consolidation within the Single Supervisory Mechanism (varying sample).

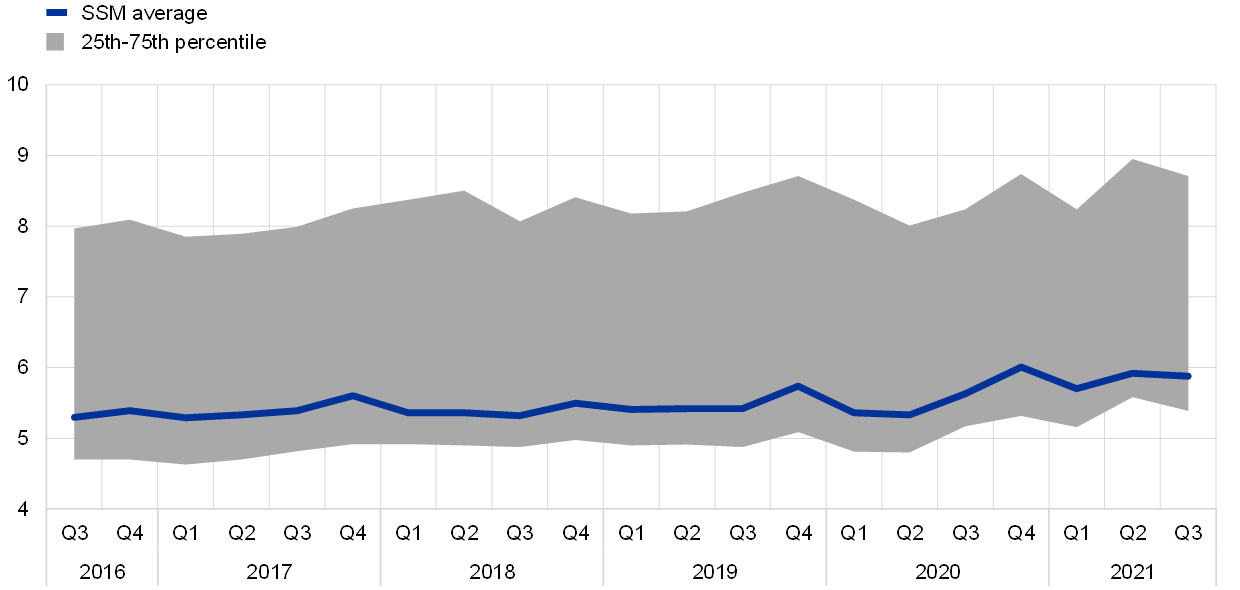

The aggregate leverage ratio followed a similar trend during the pandemic, stabilising at 5.9% in the third quarter of 2021 after increasing from 5.3% in the second quarter of 2020. Banks adequately prepared for the application of the leverage ratio requirement in June 2021. In addition, in 2022 the newly developed methodology for assessing the risk of excessive leverage – which aims to capture the contingent leverage originating from the extensive use of derivatives, securities financing transactions, off-balance sheet items or regulatory arbitrage – will be applied in order to identify banks for which qualitative measures or Pillar 2 requirements for the leverage ratio may be necessary. This will further restrict the build-up of excessive leverage and thus contribute to the resilience of the euro area banking system. However, risks to capital adequacy remain and banks should not underestimate the risk that additional losses may still have an impact on their capital trajectory as support measures expire.

Chart 2

Leverage ratio of SIs

(percentages)

Source: ECB.

Note: The sample includes all significant institutions at the highest level of consolidation within the Single Supervisory Mechanism (varying sample).

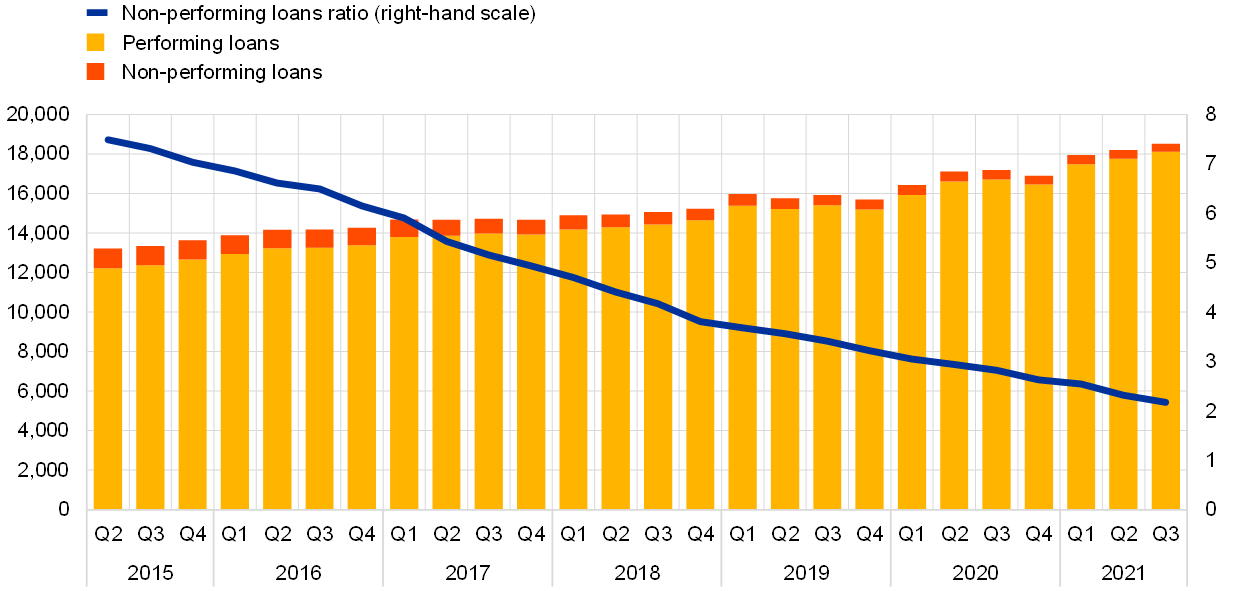

The COVID-19 related extraordinary support measures have helped prevent a surge in NPLs, but the full impact of the pandemic may only materialise in the medium term

The ECB continued to foster banks’ resilience by challenging their overall recovery capacity, i.e. the extent to which banks can recover from severe stress by implementing the recovery options set out in their recovery plans.[1]

Banks supported lending to customers throughout the crisis and so far there has not been a significant impact on asset quality. The overall positive trend in asset quality (Chart 3) has been driven by several factors, including the continued reduction of legacy non-performing loans (NPLs) by high-NPL banks and an increase in lending supported by state guarantees and other borrower support measures. In this regard, the range of COVID-19-related extraordinary support measures put in place to ease financing conditions and support households, small businesses, and corporates in 2020 and 2021 have helped prevent a surge in bankruptcies and NPLs. However, ECB Banking Supervision is still concerned about the quality of banks’ assets in the medium term, as the full impact of the pandemic may only materialise once the majority of the emergency public support measures have been withdrawn. Classifications of loans as underperforming (stage 2) remain higher than before the pandemic and loans that have benefited from COVID-19 support measures appear to have a slightly higher risk profile. In addition, the substantial increase in debt levels in various segments of the economy might translate into higher solvency risks, particularly in economic sectors or countries that have been more severely affected by the pandemic. In this context, as part of its supervisory work on credit risk in 2021, the ECB highlighted the need for a strong focus on robust credit risk management practices.[2]

Chart 3

Evolution of SIs’ NPLs (total loans)

(left-hand scale: EUR billions; right-hand scale: percentages)

Source: ECB.

Note: The sample includes all significant institutions at the highest level of consolidation within the Single Supervisory Mechanism (varying sample).

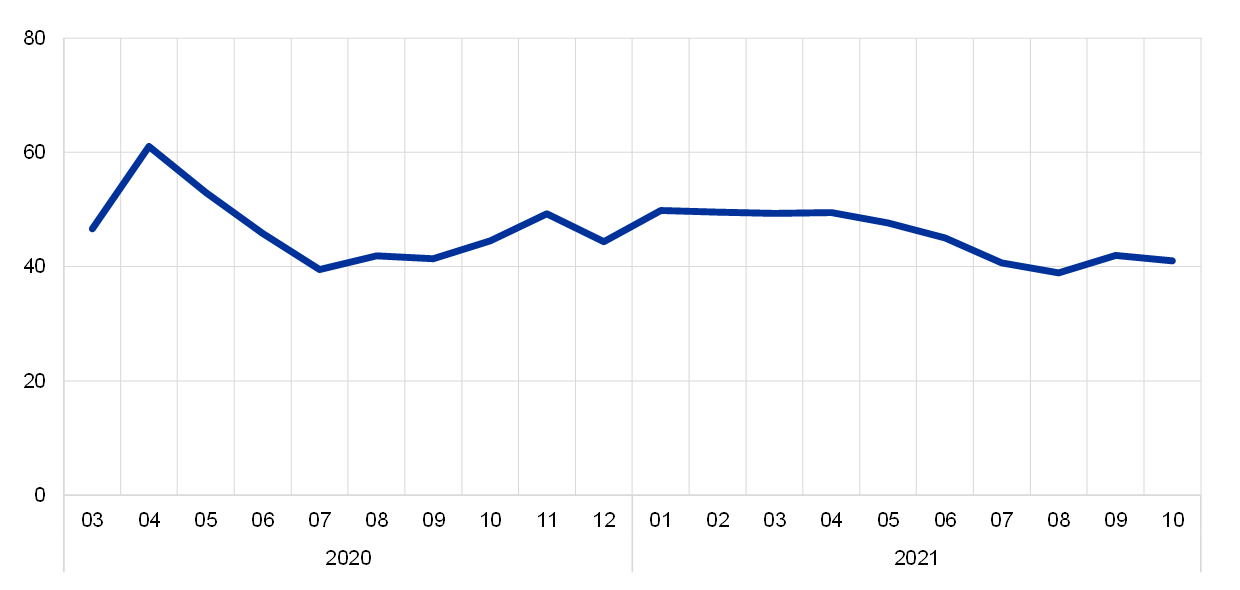

Despite business continuity challenges, the impact of the pandemic on operational risk has so far been limited

Despite the exceptional operational and business continuity challenges faced by banks since the outbreak of the pandemic, the amount of pandemic-related operational risk losses reported to have materialised in 2021 was significantly lower than in 2020. This is in line with the expectation that operational risk losses related to COVID-19 would mainly occur in the early stages of the pandemic, as these losses include major elements of a one‑off nature.[3]

After the initial activation of business continuity plans in response to the pandemic, remote working models stabilised from summer 2020, with between 40% and 50% of the workforce of SIs working from home in 2021 (Chart 4).

There was a moderate increase of 9.8% in significant cyber incidents reported to the ECB in the first half of 2021, but the impact on the availability of IT systems and the amount of losses caused by these attacks were very limited.[4]

Chart 4

(percentage of workforce working remotely)

Source: ECB.

Note: Data comprise a consistent sample of SIs which reported all data points during the period considered.

Nevertheless, operational and IT risks remain high, owing to the continued challenges facing banks and their service providers worldwide. As a result of the pandemic, cyber security threats, change management challenges and dependencies on IT infrastructures and IT service providers have all increased. It is crucial that banks properly manage the associated risks to ensure the uninterrupted provision of financial services.

Despite some improvements, several structural weaknesses related to banks’ management bodies and internal control functions remain

At the same time, the ECB has continued to emphasise the need for supervised banks to improve their governance frameworks. The COVID-19 crisis has shown the importance of having strong governance arrangements, internal control functions and data aggregation capabilities. Although some improvements have been observed, several structural weaknesses persist.

Banks have made some progress on the composition of their management bodies, such as by progressively enhancing the skillset of board members and appointing more formally independent board members. Nevertheless, some weaknesses remain, namely (i) the low level of involvement of the management body in its supervisory function and its limited ability to challenge strategic decisions in the areas most affected by the COVID-19 crisis; (ii) insufficient expertise in banking and risk management of non-executive directors in a few banks; (iii) the lack of a diversity policy and insufficient promotion of diversity in some banks, which hampers the board’s collective suitability; (iv) the low proportion of independent board members in some banks, which further hinders the ability of the management body in its supervisory function to constructively challenge executive directors.

The COVID-19 crisis also exacerbated pre-existing weaknesses in several areas of governance and risk management. First, there are still shortcomings in data aggregation and reporting owing to fragmented and non-harmonised IT landscapes, a lack of automation, widespread use of manual controls, and deficiencies in data governance (e.g. insufficient independent validation of data quality). This hinders banks’ decision-making processes. Second, several banks still need to further improve their internal control functions, especially to address low staffing, the insufficient stature of the function and deficiencies in processes (such as compliance monitoring programmes and the definition of the bank’s risk appetite).

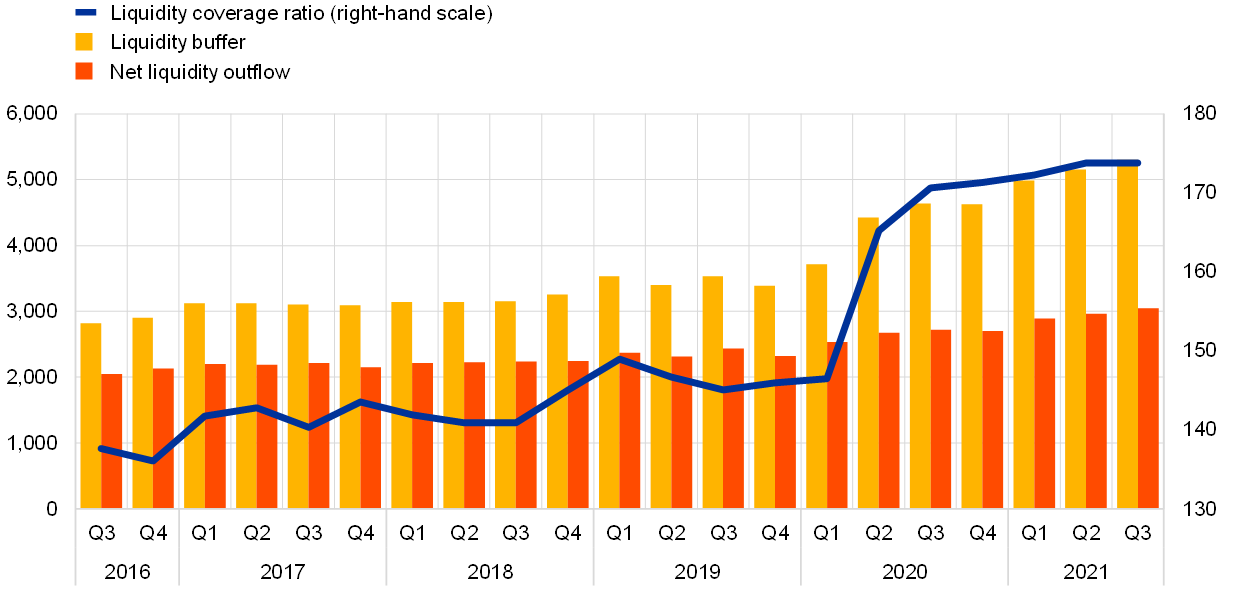

Monetary and prudential policies strongly supported the increase in SIs’ available liquidity and funding throughout 2021

Liquidity and funding conditions for SIs continued to improve, largely supported by monetary policy measures. Banks were allowed to operate below the general minimum liquidity coverage ratio (LCR) level of 100% until the end of 2021.[5] This notwithstanding, liquidity positions continued their upward trend, with the LCR reaching 173.8% in the third quarter of 2021, the highest level recorded since the start of European banking supervision (Chart 5). This can primarily be explained by the large take-up of targeted longer-term refinancing operations (TLTROs) by banks, as it enabled them to obtain funding and build cash reserves without encumbering their high-quality liquid assets. The total TLTRO uptake as at September 2021 reached €2.2 trillion, accounting for around half of the current excess liquidity in the Eurosystem.

Chart 5

Evolution of the liquidity buffer, net liquidity outflows and the LCR

(left-hand scale: EUR billions; right-hand scale: percentages)

Source: ECB.

Note: The sample includes all significant institutions at the highest level of consolidation within the Single Supervisory Mechanism (varying sample).

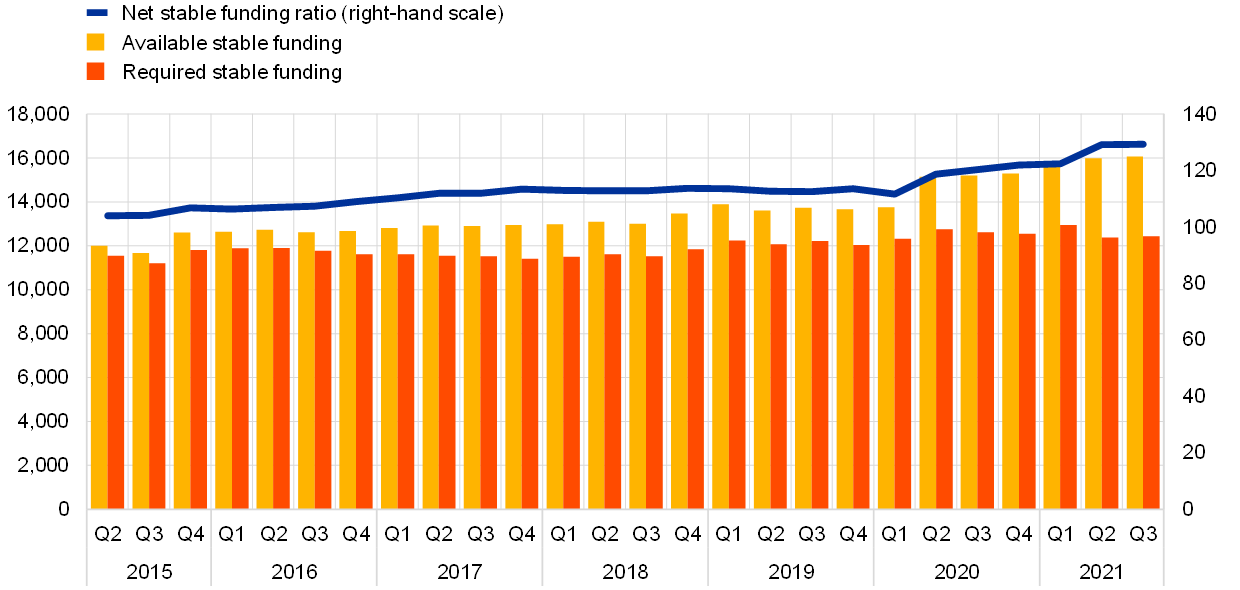

Like the LCR, the net stable funding ratio (NSFR) also increased steadily from the second half of 2020, reaching its peak of 129.3% in September 2021 (Chart 6). The NSFR requirement of 100% on an ongoing basis became applicable as a binding minimum requirement on 28 June 2021. While banks generally need to comply with the NSFR at both the consolidated and individual levels, in 2021 the ECB granted waivers from compliance at individual level to some banks when the conditions set out by the regulation were met and, in particular, when there was sound liquidity risk management in place.

Chart 6

Evolution of available stable funding, required stable funding and the NSFR

(left-hand scale: EUR billions; right-hand scale: percentages)

Source: ECB.

Note: The sample includes all significant institutions at the highest level of consolidation within the Single Supervisory Mechanism (varying sample).

General market conditions for euro area banks have continued to ease since the second half of 2020 following the exceptional intervention by governments and central banks, which resulted in lower volatility, tighter credit spreads and buoyant equity markets. As a result, broad market risk indicators, such as value at risk and risk-weighted assets (RWAs), have declined. Against this backdrop, potential market risks – linked mainly to counterparty credit risk and shocks to interest rates and credit spreads – have been identified as supervisory priorities for 2022-24.

General performance of banks under European banking supervision

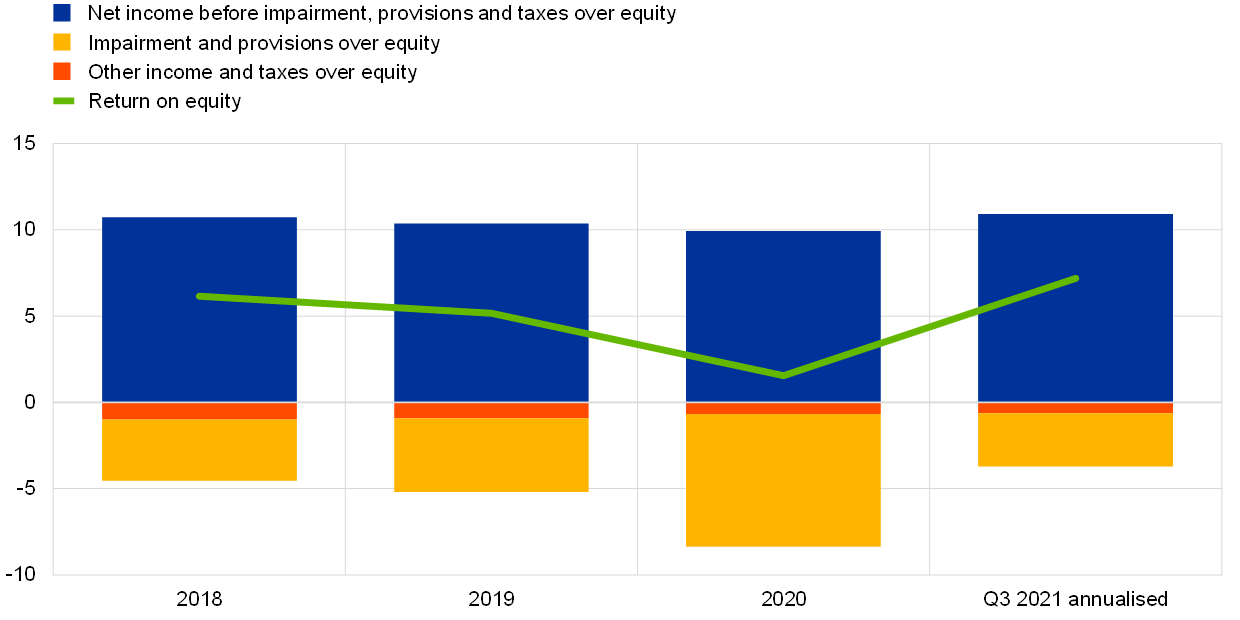

The rebound in banks’ profitability in 2021 was mainly driven by lower impairments as the economy recovered from the pandemic

After hitting a low in 2020 during the peak of the pandemic, the profitability of SIs under European banking supervision rebounded in 2021. Banks’ aggregate annualised return on equity rose to 7.2% (Chart 7) – the highest level seen in several years, but still below banks’ average cost of equity. This increase was mainly driven by a cyclical reduction in impairment flows, which more than halved compared with the previous year. Banks had to book significant precautionary provisions in 2020 owing to the unprecedented uncertainty about the impact of the pandemic. In 2021 this practice was halted or, in some cases, even reversed on account of the economic rebound observed during the year.

Chart 7

SIs’ aggregate return on equity broken down by income/expense source

Source: ECB supervisory statistics.

Note: The sample includes all significant institutions at the highest level of consolidation within the Single Supervisory Mechanism (varying sample).

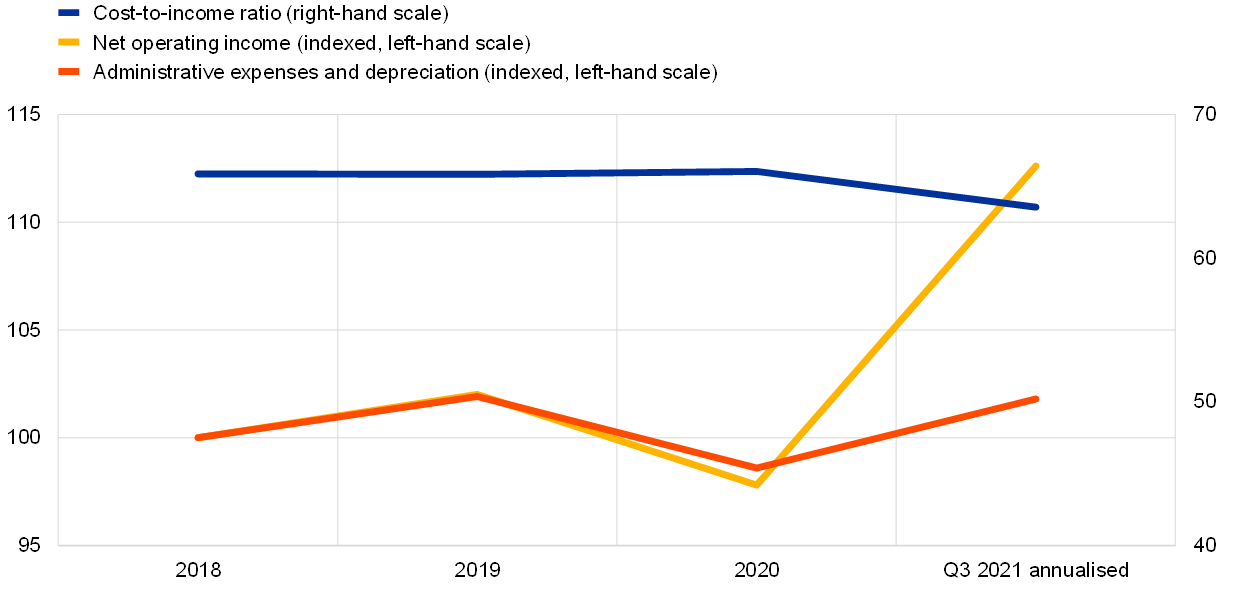

The economic rebound also benefited income before impairment, provisions and taxes, which recovered to pre-pandemic levels. This was mostly due to the boost to banks’ income from trading and investment activities and to their net fee and commission income, with asset management-related fees playing a key role. By contrast, net interest income remained subdued and below pre-pandemic levels owing to persistent pressure on banks’ lending margins. Overall, banks managed to increase their net operating income by 15% (Chart 8). This increase in income was central to the improvement in banks’ cost efficiency, with the cost-to-income ratio decreasing by more than 2 percentage points in 2021 to stand at 63.5%.

Chart 8

SIs’ cost-to-income ratios and indexed components

(percentages)

Source: ECB supervisory statistics.

Note: The sample includes all significant institutions at the highest level of consolidation within the Single Supervisory Mechanism (varying sample).

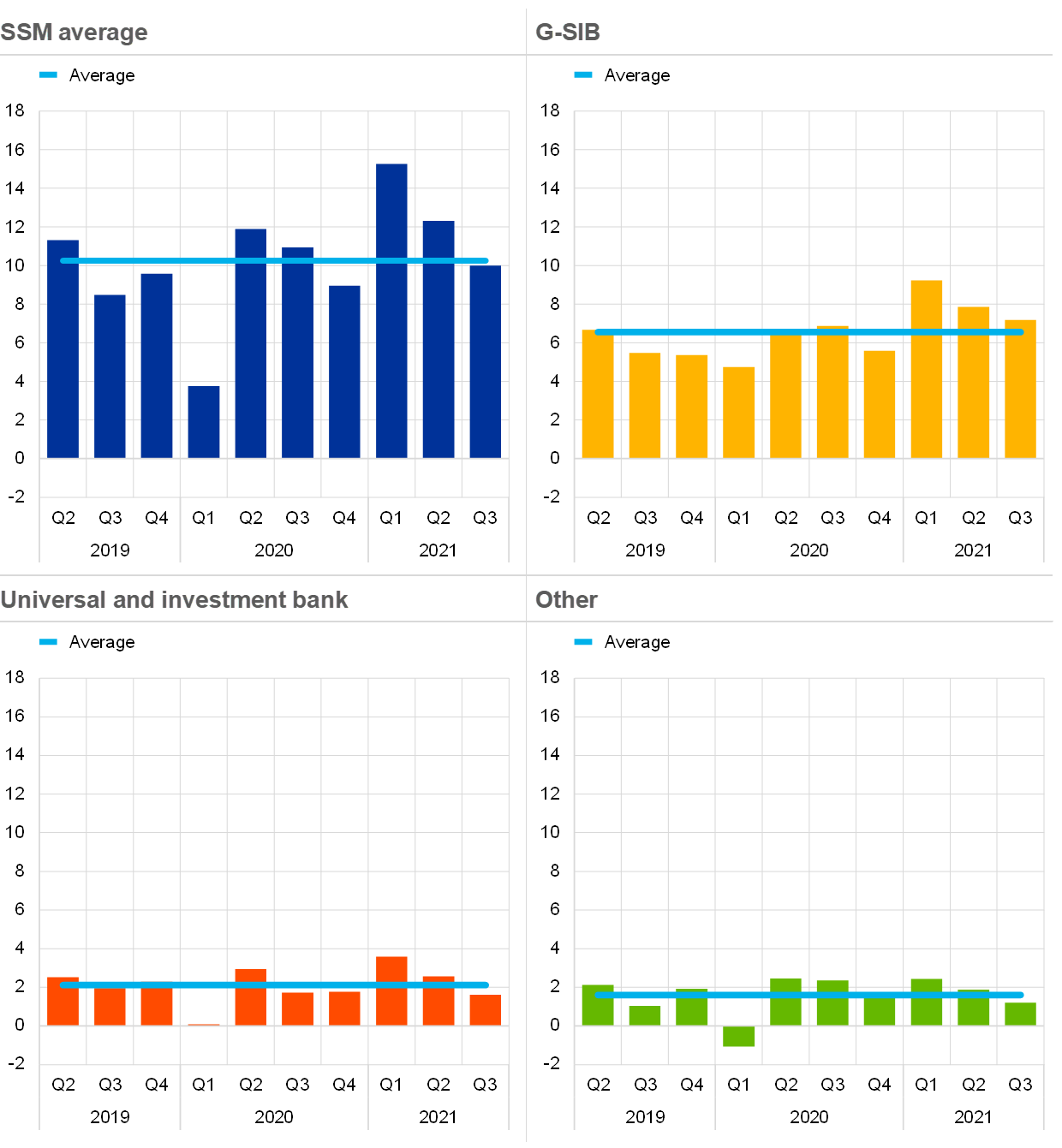

Trading income contributed positively to the profitability of banks under European banking supervision and peaked in the first half of 2021, especially for global systemically important banks (G-SIBs) (Chart 9). Banks also managed to substantially increase their net fee and commission income, with asset management-related fees benefiting from high asset prices.

Chart 9

Trading and investment income flows[6] by selected business models

(quarterly flows in EUR billions)

Source: ECB.

Notes: The sample for “SSM average” includes all significant institutions at the highest level of consolidation within the Single Supervisory Mechanism (varying sample); the “G-SIB”, “Universal and investment bank” and “Other” charts represent the sub-sample with the respective business models.

On the cost side, administrative expenses and depreciations increased by 3.3%, primarily owing to increased staff expenses and IT-related costs. However, banks maintained their broader strategic objectives of reducing expenses and investing in IT and digital initiatives. Such strategies entail significant costs that need to be borne upfront, but banks expect to reap the benefits of this transformation in the medium term. Additionally, in the light of customers’ increased usage of digital channels as a result of the pandemic, banks might be able to further reduce overcapacity and achieve leaner cost structures, thereby improving their cost efficiency even more.

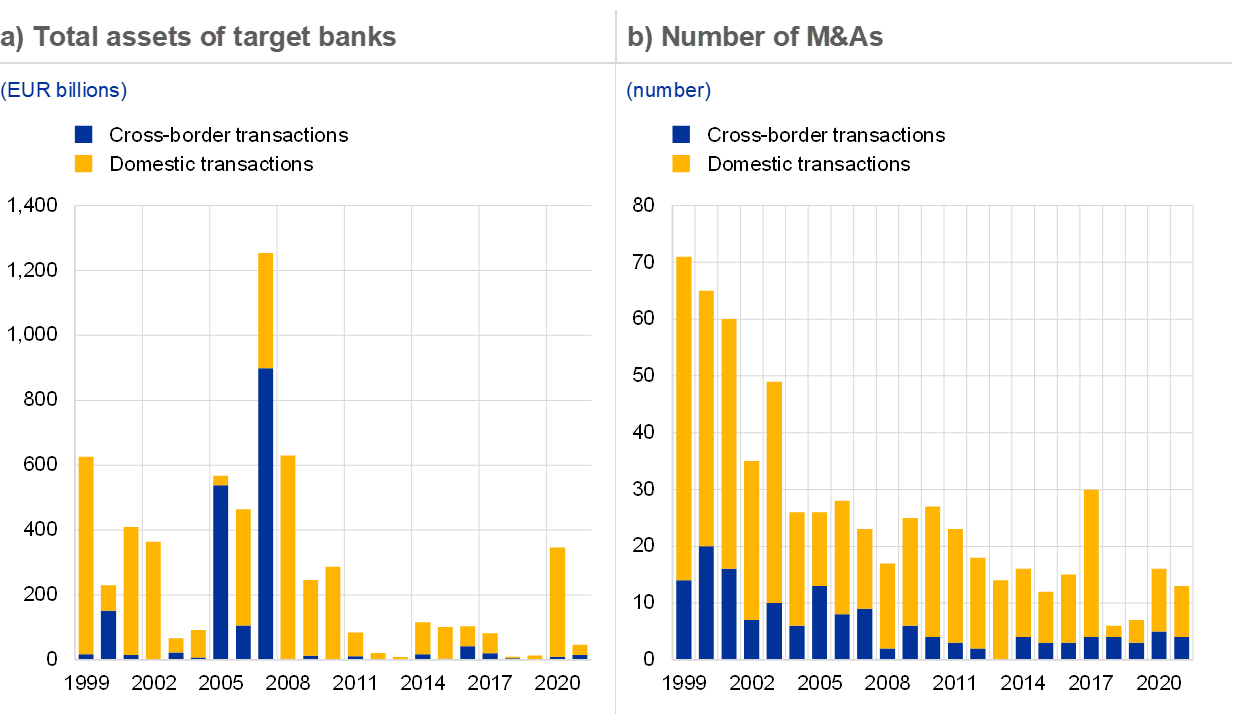

Bank mergers and acquisitions (M&As), generally considered the boldest and most transformative type of consolidation, appear to act as a catalyst for the sector to improve efficiency and return to more sustainable levels of profitability.[7] M&A activity appears to have gained some momentum over the past two years. In particular, banks have engaged more actively in targeted consolidations at the level of a business line. In the areas of asset management, securities business, custody services and payment technology, some institutions have been expanding or diversifying, while others have been downsizing in order to redirect resources.

Chart 10

Total assets of target banks and number of M&As in the euro area

Source: ECB calculations based on Dealogic and Orbis BankFocus.

Notes: The sample includes M&A transactions involving SIs and LSIs in the euro area, excluding some private transactions and transactions between small banks not reported in Dealogic. Transactions associated with the resolution of banks or distressed mergers were removed from the sample. Transactions are reported on the basis of the year in which they were announced.

Fully fledged bank M&As are still predominantly domestic, but some of the more targeted transactions feature a cross-border dimension and thus also contribute to financial integration within the EU. Another avenue to pursue cross-border integration would be for banks to review their cross-border organisational structures. In particular, relying more extensively on branches and the free provision of services, instead of on subsidiaries, could be a promising approach to developing cross-border business within the banking union and the Single Market.

Efforts to increase profitability in a sustainable way could also trigger further consolidation initiatives, which could lead to more diversified income sources and greater efficiency if accompanied by a clear operational direction and a sound business strategy. However, these strategic actions have to be designed and managed by the banks themselves, with their boards ensuring that there are robust governance procedures in place that can appropriately identify, manage and mitigate all material risks to the execution of these consolidation activities. To facilitate banks’ planning in this regard, in January 2021 the ECB published a guide on the supervisory treatment of mergers and acquisitions[8] to provide transparency on how the ECB assesses merger transactions, so that banks know what to expect from their supervisor.

LSIs’ profitability also improved in 2021, driven primarily by lower impairments

Following a similar trend to that of SIs, the profitability of less significant institutions (LSIs) under European banking supervision also showed signs of recovery in 2021. As at the end of September 2021, the average return on equity was 3.3%, up from 1.7% at the end of 2020. This increase was mainly driven by lower impairments compared with 2020, when LSIs had to book a significant amount of provisions to prevent a sharp deterioration of their loan books. Similarly to SIs, in 2021 some LSIs released some of their previously booked provisions, which helped to restore their profitability to pre-pandemic levels.

LSIs have been able to offset the pressure on their lending margins by enhancing fee and commission-based activities. Overall, LSIs’ net operating income increased by 9.7% year on year. This boost to LSIs’ sources of income supported the improvement in their average cost-to-income ratio, which decreased from 70.3% at the end of 2020 to 66.7% at the end of September 2021. On the cost side, LSIs were unable to effectively reduce their administrative expenses.

Box 1

Stress testing in 2021

As in previous years, the ECB was involved in the preparation and execution of the 2021 EU-wide stress test, which was coordinated by the European Banking Authority (EBA). As part of the preparatory work, the ECB took part in designing the stress test methodology as well as the baseline and adverse scenarios. The adverse scenario was developed together with the European Systemic Risk Board (ESRB) and the EBA, and in close cooperation with the national central banks and national competent authorities. The ECB also produced the official credit risk benchmarks for the EU-wide stress test. These benchmarks provide banks with projection paths for the behaviour of credit risk parameters (such as probabilities of default, transition rates and loss given default), with banks expected to apply them to portfolios where no appropriate credit risk models are available.

Following the launch of the stress test exercise on 29 January 2021, ECB Banking Supervision carried out the quality assurance process for the banks under its direct supervision with the aim of ensuring that the banks correctly applied the EBA’s methodology. Of the 50 banks covered by the EU-wide stress test, 38 are directly supervised by ECB Banking Supervision and account for around 70% of euro area banking sector assets. The EBA published the individual results for all 50 participant banks, along with detailed balance sheet and exposure data as at year-end 2020, on 30 July 2021.

In addition to the EU-wide exercise, the ECB conducted its own stress test on 51 medium-sized banks that are under its direct supervision, but were not included in the EBA exercise. For the first time, the ECB also published high-level individual results for these banks.

The 38 euro area banks covered by the EU-wide stress test and the 51 medium-sized euro area banks supervised by the ECB together represent slightly more than 75% of the total banking assets in the euro area.

Scenarios

The adverse scenario for the 2021 stress test assumed a prolonged impact from the COVID-19 shock in a lower-for-longer interest rate environment. In this scenario, the uncertainty around pandemic-related developments results in a prolonged economic contraction, characterised by a sustained drop in GDP and a strong increase in unemployment. Corporate bankruptcies and business downsizing force considerable adjustments in asset valuations, credit spreads and borrowing costs. Finally, residential and, in particular, commercial real estate prices fall significantly.

Results[9]

Under the adverse scenario, the final CET1 ratio for the 89 banks directly supervised by the ECB was 9.9% on average, 5.2 percentage points lower than the starting point of 15.1%. For the 38 banks tested by the EBA, the average CET1 capital ratio fell by 5 percentage points from 14.7% to 9.7%. The 51 medium-sized banks tested solely by the ECB showed an average capital depletion of 6.8 percentage points to 11.3%, from a starting point of 18.1%. Medium-sized banks experienced a larger capital depletion under the adverse scenario because they were more affected by lower net interest income, lower net fee and commission income and lower trading income over the three-year horizon.

Overall, banks were in better shape at the start of the 2021 exercise than at the start of the previous EU-wide stress test in 2018.[10] This was due to significant reductions in operational costs and material declines in NPL stocks in many countries. However, the capital depletion at the system level was higher in 2021. This is because the adverse scenario in the 2021 stress test was more severe than the one used in the 2018 exercise.

The first key driver of capital depletion was credit risk, as the large macroeconomic shock in the adverse scenario led to significant loan losses. In addition, and despite the overall resilience of the banking system even under adverse conditions, the stress scenario resulted in significant market losses for the largest banks in the euro area in particular, as they are more exposed to equity and credit spread shocks. The third main driver of capital depletion was banks’ limited ability to generate income under adverse economic conditions, as banks faced a significant decrease in their net interest income, trading income and net fee and commission income.

Integration of the stress test into regular supervisory work

The qualitative results (i.e. the accuracy and timeliness of banks’ submissions) and the quantitative results (i.e. capital depletion and banks’ resilience to adverse market conditions) of the stress test both served as input to the annual Supervisory Review and Evaluation Process (SREP). The quantitative impact resulting from the adverse scenario was also a key input for supervisors to determine the level of Pillar 2 guidance (P2G), through a new two-step bucketing approach. The details provided on the new P2G methodology should foster a better understanding of the use of the stress test results within the SREP.

1.2 Supervisory priorities and projects in 2021

Supervisory priorities for 2021

In 2021 the ECB’s supervisory priorities focused on areas materially affected by the pandemic

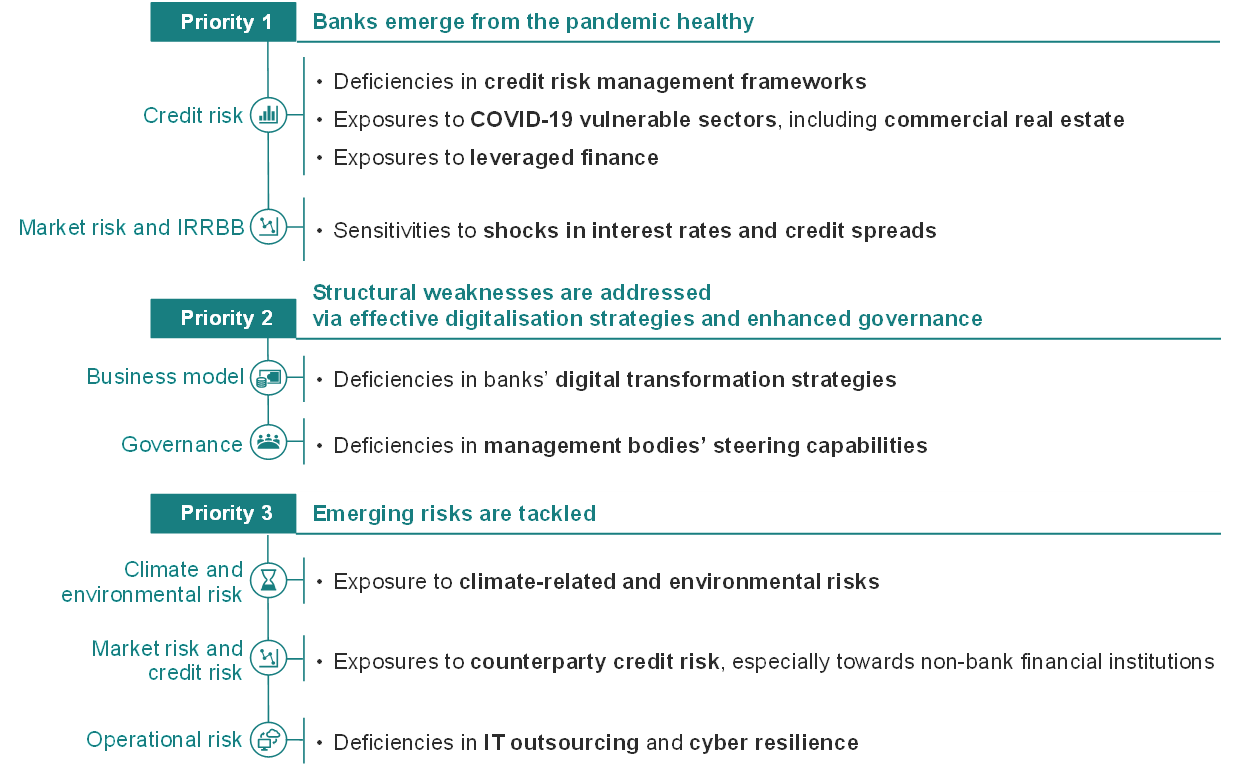

In 2021 ECB Banking Supervision primarily focused its supervisory efforts on four priority areas materially affected by the COVID-19 pandemic: credit risk management, capital strength, business model sustainability and governance. The supervisory activities and projects carried out over the year were aimed at strengthening the resilience and practices of supervised banks, with a particular focus on those vulnerabilities deemed critical in the context of the pandemic.

Credit risk

A unique feature of the COVID-19 crisis is that, amid an enormous drop in economic output, NPLs have continued to fall, also thanks to the exceptional policy measures taken to support the real economy. These unprecedented measures have blurred borrowers’ creditworthiness and therefore challenged banks’ ability to manage credit risk. Against this background, the work undertaken by ECB Banking Supervision in 2020 to assess the adequacy of banks’ credit risk management frameworks continued through 2021. The objective was to strengthen banks’ operational preparedness to address distressed debtors in a timely manner as well as their ability to adequately identify, assess and mitigate potential deteriorations in borrowers’ asset quality, especially in sectors particularly vulnerable to the impact of the pandemic. Initiatives undertaken in 2021 to achieve this objective include deep dives into banks’ exposures to the accommodation and food services sector, dedicated on-site activities, and follow-ups by Joint Supervisory Teams (JSTs) with banks that were flagged as deviating considerably from the supervisory expectations.

Capital strength

The concerns about heightened credit risk made it essential for supervisors to assess the strength of SIs’ capital positions and identify bank-specific vulnerabilities at an early stage, so that timely remedial actions could be taken where needed. In 2021 ECB Banking Supervision reviewed banks’ capital planning practices to assess their capacity to produce realistic capital forecasts that take into account the economic uncertainties stemming from the pandemic. The 2021 EU-wide stress test exercise allowed for an in-depth assessment of banks’ capital positions and showed that the euro area banking sector would remain resilient even under an adverse scenario.

In July the ECB decided not to extend beyond September 2021 its recommendation that all banks limit dividends. The capital and distribution plans of every bank would instead be assessed as part of the regular supervisory process. Banks are expected to remain prudent when deciding on dividends and share buy-backs and to carefully consider the sustainability of their business model and the risk of additional losses affecting their capital trajectory once public support measures expire. At this stage, the ECB does not expect to extend its prudential relief measures related to banks’ use of capital buffers beyond the end of 2022.

Business model sustainability

Banks’ profitability and business model sustainability remained under pressure in 2021 against an economic background of low interest rates, excess capacity and low cost efficiency in the European banking sector and increasing competition from non-banks. ECB Banking Supervision has continued to strengthen its supervisory toolkit to assess banks’ business strategies to meet these challenges as well as their ability to effectively implement them, with a specific focus on digitalisation strategies. In this context, JSTs have engaged in a structured dialogue with banks’ management bodies on the oversight of their business strategies. Finally, bank-specific deep dives and on-site inspections were conducted to investigate profitability drivers and weaknesses.

Governance

Sound governance practices and robust internal controls are crucial for mitigating the risks that banks face during normal times, and even more so in times of crisis. In 2021 ECB Banking Supervision pursued several supervisory activities in the area of governance. First, it scrutinised banks’ procedures for responding to a crisis, which included assessing banks’ capacity to produce effective recovery plans and credibly demonstrate their overall recovery capacity. Second, it followed up on the thematic review on risk data aggregation and reporting and launched targeted reviews for specific banks, in an effort to promote banks’ management having access to and challenging the accuracy of risk information. Finally, prudential work continued on money laundering and terrorism financing risks, which included updating the supervisory methodologies for the SREP and on-site investigations to reflect these risks.

Credit risk management

ECB Banking Supervision assessed banks’ compliance with the supervisory expectations on credit risk management and JSTs have been following-up with the banks on addressing identified gaps

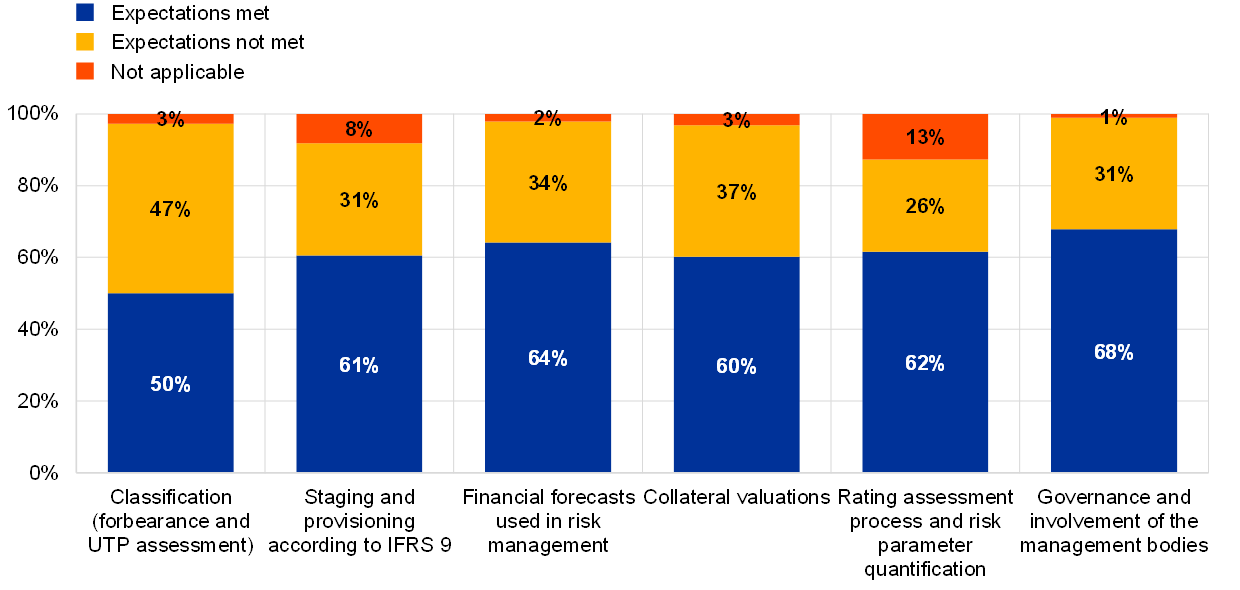

In times of uncertainty, such as during the COVID-19 pandemic, credit risk management – and in particular identifying, classifying and measuring credit risk in an adequate and timely way – is key to ensuring that banks are able to provide viable, prompt solutions to distressed debtors. On 4 December 2020 the ECB sent a letter to the CEOs of all SIs setting out its supervisory expectations in this regard. During 2021 ECB Banking Supervision assessed banks’ risk management practices against these expectations and concluded that 40% of SIs have significant gaps. The main gaps relate to early warning systems, classification (including forbearance and unlikely-to-pay (UTP) assessments), provisioning practices and, for some banks, practices for collateral valuation and financial forecasts (Chart 11). The issues identified are structural and relevant both in the context of the COVID-19 crisis and in a business-as-usual situation. Notably, shortcomings were identified and will also need to be addressed in banks that have not seen a significant build-up of credit risk in previous years. JSTs have been following up with the banks on their implementation of remedial actions.

Chart 11

Gaps in SIs’ credit risk management

(percentage of SIs)

Source: ECB. The sample includes 108 significant institutions at the highest level of consolidation within the Single Supervisory Mechanism.

Note: The chart presents the JST view on the materiality of the gaps in SIs’ credit risk management in relation to the supervisory expectations set out in the “Dear CEO” letter of 4 December 2020.

Box 2

Vulnerable sector analysis

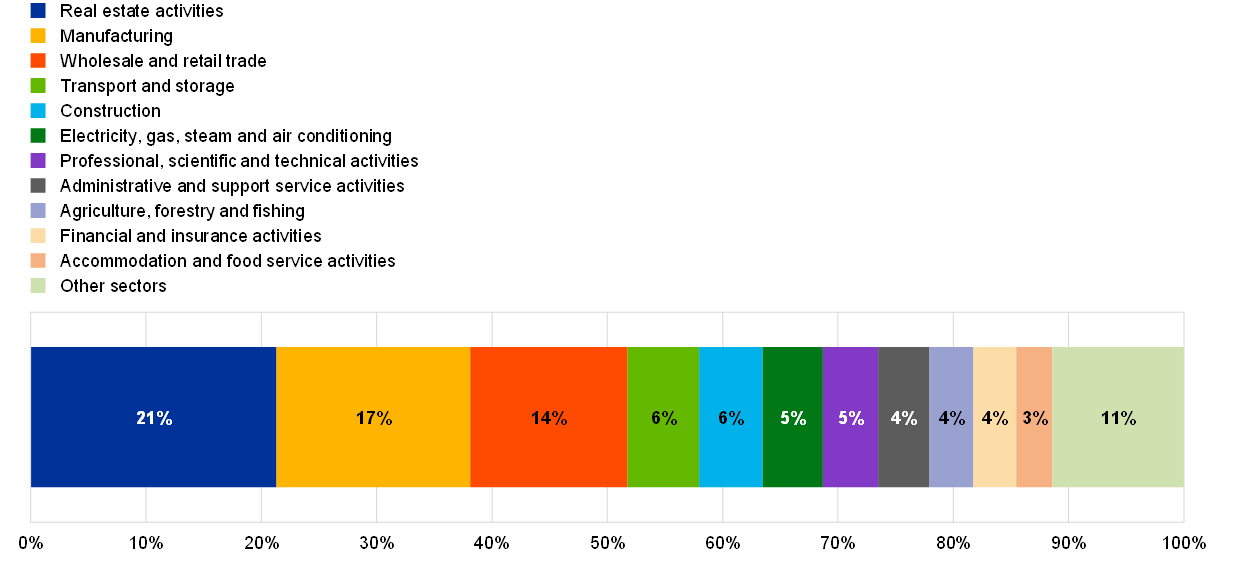

The COVID-19 pandemic has increased corporate vulnerabilities in certain sectors. The immediate impact of the pandemic shock was largely mitigated by the substantial schemes that were set up to support smaller companies, while larger companies were able to tap into capital markets to withstand the initial fallout from the shock. However, as the extraordinary support measures start to be withdrawn, some companies may find themselves in financial distress as debt accumulated during the COVID-19 crisis falls due. For some industries, persistent supply chain problems are increasing costs and putting a drag on liquidity, thereby further heightening credit risk. Significant institutions’ exposure to all business sectors is outlined in Chart A.

Chart A

SIs’ exposure to non-financial corporates by economic sector of activity

(as a percentage of gross carrying amount of total loans and advances to non-financial corporates)

Source: FINREP reporting.

Notes: Economic sectors are based on the NACE level 1 classification. “Other sectors” includes Other services; Information and communication; Human health services and social work; Mining and quarrying; Water supply; Arts, entertainment and recreation; Education; and Public administration and defence, compulsory social security.

In the light of the increased vulnerabilities in certain sectors, in early 2021 ECB Banking Supervision launched a targeted review of the accommodation and food services sector, based on an analysis of exposures of a sample of SIs to this sector. The objective of this review was to understand and assess how banks were managing credit risk in one of the sectors most affected by the COVID-19 pandemic. ECB Banking Supervision identified several areas of concern across the different stages of the credit risk cycle, with small and medium-sized enterprise borrowers being a source of particularly serious concern.

In September 2021 ECB Banking Supervision continued its work on vulnerable sectors by launching a targeted review of the commercial real estate sector, with a particular focus on the office and retail market. This targeted review has continued into 2022. Although exposure varies across member countries, commercial real estate[11] is the largest sectoral exposure for SIs in the euro area, accounting for around 22% of the total exposure of banks to non-financial corporations.

IT and cyber risk

IT and cyber risk continued to be a key risk driver for the banking sector in 2021

IT and cyber risk continued to be a key risk driver for the banking sector in 2021 amid the trend towards digitalisation, which has been accelerated by the pandemic. This trend has forced banks to adopt widespread remote working arrangements and increased their exposure to cyberattacks and their reliance on third-party providers. In the first half of 2021 the number of significant cyber incidents reported to the ECB increased slightly, by 9.8%, compared with the same period in 2020, but the impact of the incidents remained relatively contained. Although some of the reported incidents have increased in complexity, many still reflect failures in basic cyber security measures, suggesting that banks are yet to implement comprehensive cyber security practices.

In July 2021 ECB Banking Supervision published its Annual report on the outcome of the 2020 SREP IT Risk Questionnaire, which presents the ECB’s main observations about SIs’ responses to the questionnaire. The report notes that (i) SIs are becoming increasingly reliant on third-party service providers, including cloud services; (ii) there is room for improving the way banks implement basic measures to maintain the health and security of their systems; (iii) the number of end-of-life systems is increasing; and (iv) data quality management remains the least mature risk control area. While many banks embarked on large-scale programmes to improve their data management capabilities, progress has varied. This is due to difficulties in managing the programmes’ complex interdependencies with strategic and regulatory IT and operational projects as well as the structural changes the programmes entail in the IT landscapes of institutions. The pandemic conditions have also slowed progress in this area.

To address IT and cyber risk, ECB Banking Supervision has continued to strengthen its use of supervisory instruments such as the annual SREP, the SSM cyber incident reporting process, on-site inspections and other targeted horizontal activities.

In 2021 ECB Banking Supervision also contributed to the activities of international working groups on this topic, including those led by the EBA, the Basel Committee on Banking Supervision, and the Financial Stability Board.

Follow-up on Brexit

The transition period – during which time European Union law continued to apply within and to the United Kingdom – ended on 31 December 2020, marking the end of banks’ Brexit preparations.

ECB Banking Supervision will continue to monitor banks’ alignment with its post-Brexit expectations and, if needed, further refine its stance towards the adequacy of banks’ structures and governance

In this context, and as part of its ongoing supervision, ECB Banking Supervision monitored the implementation of the post-Brexit target operating models of SIs affected by the United Kingdom’s departure from the EU to ensure they progressed in line with the time frames previously agreed on. Horizontal monitoring exercises were complemented by bank-specific follow-ups, and supervisory actions were taken when shortcomings were identified. To meet the ECB’s supervisory expectations, banks took action in the areas of internal governance, business origination, booking models and funding, repapering of EU clients and intragroup arrangements, and IT infrastructure and reporting.

To ensure that, post-Brexit, banks are operationally self-standing and not overly reliant on group entities outside the EU, the ECB focused on preventing empty shell characteristics in the newly established EU subsidiaries of international banking groups. In this context, it launched a desk-mapping review – a harmonised assessment of SIs’ booking models – to ensure that banks’ arrangements sufficiently reflect the size, nature and complexity of their business and risks. In addition, the ECB launched a targeted review of the credit risk management and funding set-ups of these banks to ensure that they are able to independently manage all material risks that could potentially affect them at the local level (i.e. in the EU), and that they have control over their balance sheets and exposures.

ECB Banking Supervision also followed post-Brexit regulatory developments to anticipate any possible impact on the financial industry. In particular, it asked banks to pay special attention to the European Commission’s communications on the risks stemming from over-reliance on UK central counterparties in the longer term.

Under the cooperation framework concluded in 2019, ECB Banking Supervision and the UK supervisory authorities continue to closely cooperate in supervising banks that are active in countries participating in European banking supervision and the United Kingdom. ECB Banking Supervision maintains close interactions with the UK authorities on topics of common interest, at senior level and operational level.

ECB Banking Supervision will continue to follow post-Brexit regulatory developments and monitor banks’ alignment with its post-Brexit expectations and, if needed, will further refine its stance towards the adequacy of their structures and governance.

Fintech and digitalisation

As banks continue their digital transformation, ECB Banking Supervision is actively shaping the European supervisory and regulatory frameworks on technology and digitalisation

In 2021 ECB Banking Supervision continued its work on fintech and digitalisation-related topics. This included organising a workshop with the JSTs of the largest SIs on the strategic, governance and risk management aspects of digital transformation. It also launched the revision of the SREP methodology on business models with a view to better reflecting digital transformation aspects in upcoming supervisory cycles. Furthermore, ECB Banking Supervision continued to develop its tools to systematically assess banks’ digital transformation frameworks. This assessment looks at key performance indicators and the use of new technologies by banks, focusing on the relevance of these aspects to their business models.

The COVID-19 pandemic has demonstrated the importance of digital transformation and technology in enabling banks to remain operationally resilient in a remote working context. Given the role technology can play in reducing costs and meeting the expectations of increasingly digitally oriented banking customers, it is crucial that banks continue to innovate and pursue digital transformation to remain competitive now and in the future.

ECB Banking Supervision also took further steps to actively shape digitalisation aspects of the future European regulatory framework by contributing to the ECB opinions on the draft legislative proposals on markets in crypto assets[12], the pilot regime for market infrastructures based on distributed ledger technology[13], and the digital operational resilience act[14]. In addition, it contributed to the ECB opinion on the legal framework on artificial intelligence. ECB Banking Supervision also took part in discussions with the European Supervisory Authorities on the regulation of fintech and big tech and the regulatory scope of consolidation.

1.3 Direct supervision of significant institutions

Off-site supervision

ECB Banking Supervision strives to supervise SIs in a proportionate and risk-based manner that is both demanding and consistent. To that end, it defines a set of core ongoing supervisory activities for each year. These activities draw on the existing regulatory requirements, the SSM Supervisory Manual and the SSM supervisory priorities, and are included in the ongoing supervisory examination programme (SEP) for each SI.

In addition to those activities addressing system-wide risks, other supervisory activities that are tailored to banks’ specificities can be included in the SEP, leaving room for JSTs to analyse and tackle idiosyncratic risks.

The off-site SEP activities include (i) risk-related activities (e.g. the SREP), (ii) other activities related to organisational, administrative or legal requirements (e.g. the annual assessment of significance), and (iii) additional activities planned by JSTs to further tailor the ongoing SEP to the specific characteristics of the supervised group or entity (e.g. analyses of the bank’s business model or governance structure). While the first two sets of activities are defined centrally, the third is bank-specific and defined by the respective JST.

Being proportionate

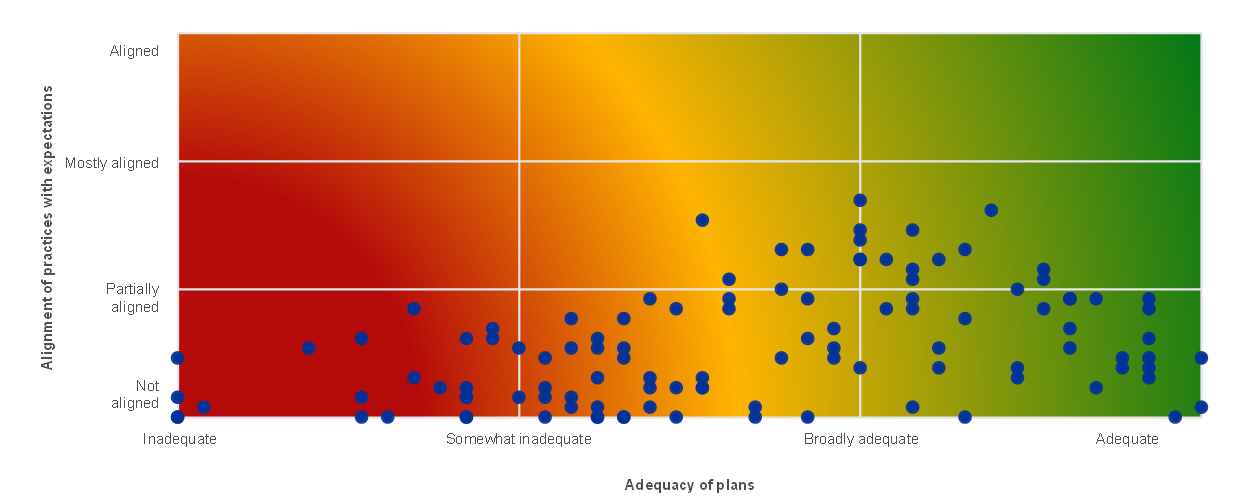

Planned supervisory activities in 2021 followed the principle of proportionality, tailoring the intensity of supervision to the systemic importance and risk profile of the supervised bank

The SEP follows the principle of proportionality, i.e. the intensity of the supervision depends on the size, systemic importance, risk and complexity of each institution.

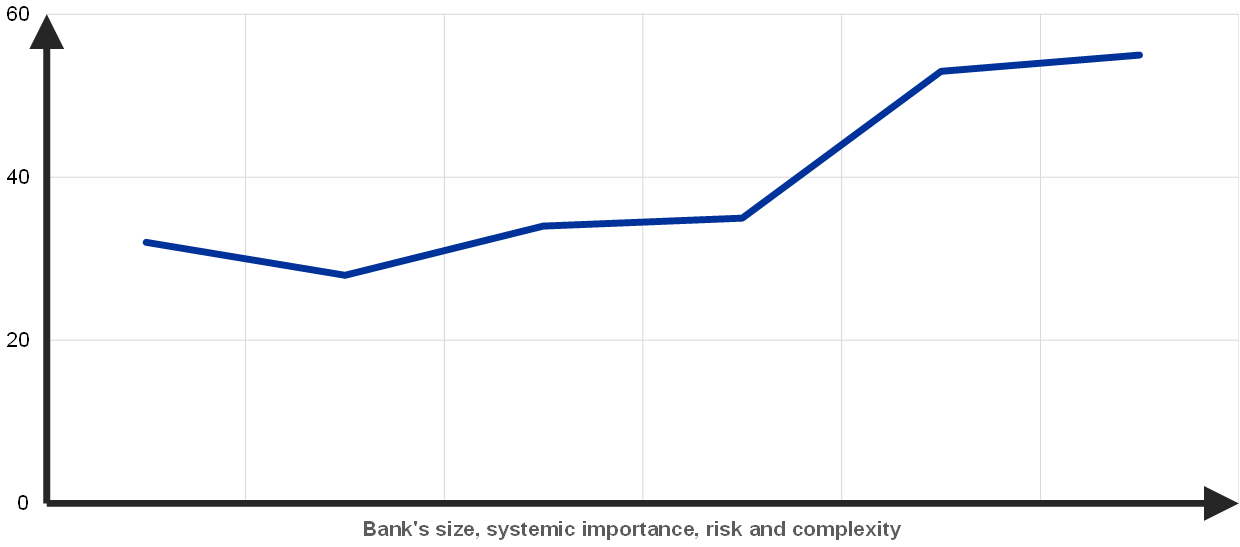

As in previous years, the average number of planned supervisory activities per SI in 2021 reflects this principle of proportionality, ensuring that JSTs have sufficient leeway to address institution-specific risks (Chart 12).

Chart 12

Average number of planned tasks per SI in 2021

Source: ECB.

Note: Data extracted as at 29 December.

Taking a risk-based approach

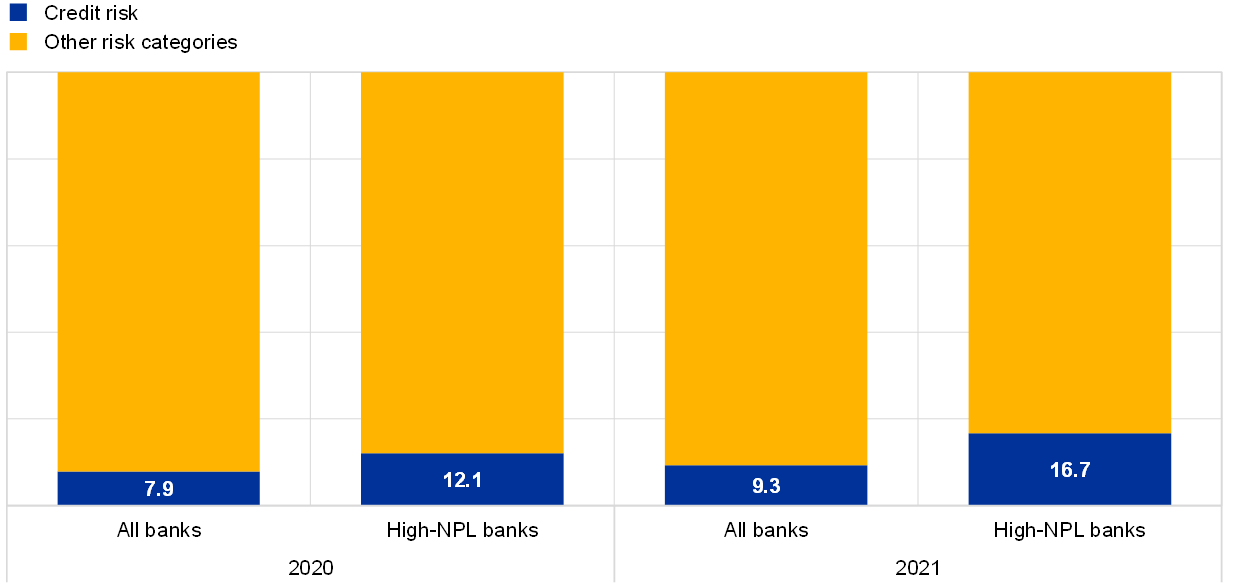

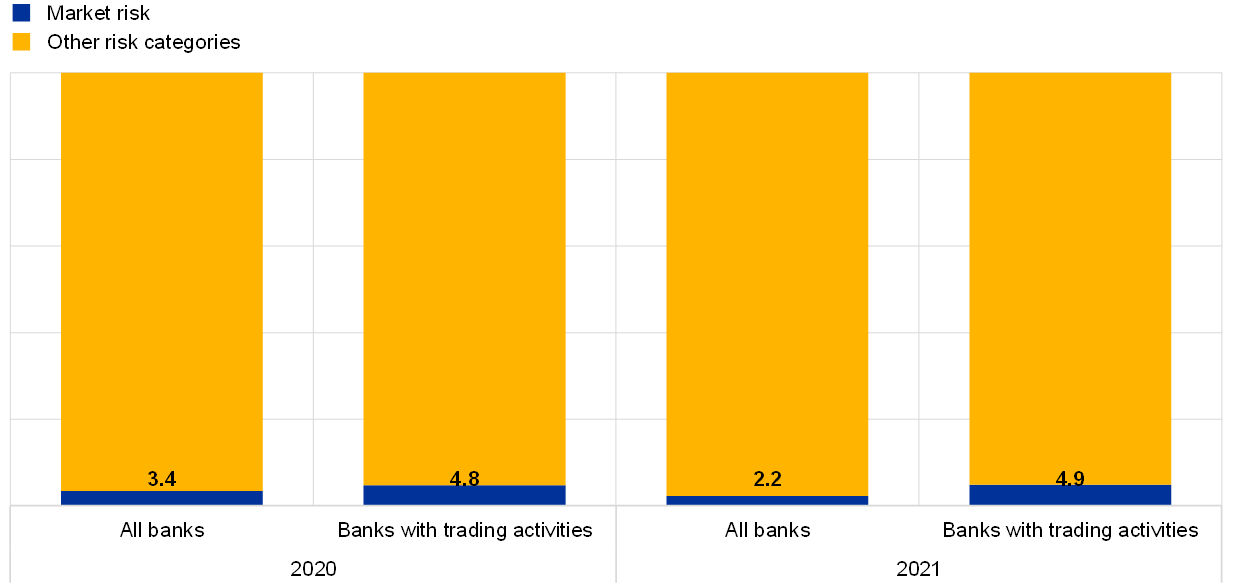

The SEP follows a risk-based approach, focusing on the most relevant risk categories for each SI. For example, the percentage of tasks related to credit risk is greater for high-NPL banks than it is for the average bank. Similarly, the percentage of tasks relating to market risk is higher for banks with large exposures to market and trading activities than it is for the average bank (Chart 13).

Chart 13

SEP activities in 2020 and 2021: credit and market risk activities as a share of all activities

Credit risk

(percentages)

Market risk

(percentages)

Source: ECB.

Notes: The sample includes all banking supervision activities carried out by JSTs (varying sample). Data extracted as at 29 December. Only planned activities related to risk categories were considered. Activities with multiple risk categories (e.g. the SREP and stress test exercises) are included under “Other risk categories”.

Highlights of off-site supervision in 2021

As a consequence of the reorganisation of ECB Banking Supervision, the COVID-19 pandemic and simplification efforts, ECB Banking Supervision reviewed and reprioritised supervisory processes and activities to enable the JSTs to adequately focus on monitoring the conditions of supervised banks. The planned set of off-site activities for 2021 was also reviewed and calibrated to the risk prioritisation. Examples of the centrally driven activities carried out in 2021 are the SREP assessment, the reviews of credit risk management practices and sectoral vulnerabilities, the SSM-wide stress test exercise, the NPL strategy assessment and the climate risk self-assessment.

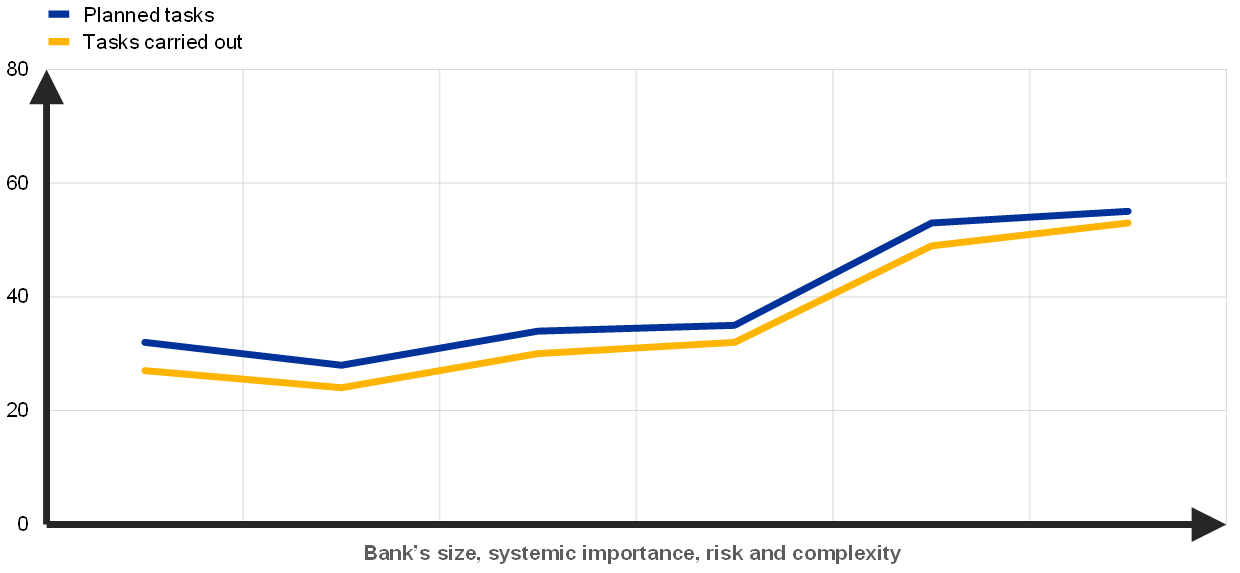

The number of activities carried out in 2021 was marginally lower than what was originally planned at the beginning of the year (Chart 14). This is mostly due to a small number of administrative tasks being cancelled throughout the year, which is in line with previous years.

SREP assessment

In 2020 ECB Banking Supervision adopted a pragmatic approach to the SREP in the light of the COVID-19 pandemic. In 2021 it returned to a full SREP assessment. The SREP results point to a broad stability in scores despite the challenges posed by the COVID-19 crisis, as banks had generally entered the pandemic with strong capital positions and were supported by relief measures, which remained in place in 2021. Consistent with previous SREP cycles and the 2021 supervisory priorities, the majority of measures addressed deficiencies in credit risk and internal governance.

Credit risk was the main area of focus of the SREP assessment. Banks’ risk control frameworks were assessed against the supervisory expectations communicated to banks in the “Dear CEO” letter of 4 December 2020. The assessment led to an increased number of findings, which mostly reflected concerns about the quality of banks’ processes. In a number of cases, the severity of the findings raised concerns about the adequacy of the underlying provisioning processes, including in banks that had not previously stood out from a credit risk perspective.

Despite the challenges brought about by the pandemic, capital adequacy proved resilient: supervisors closely reviewed banks’ dividend plans and maintained a supervisory dialogue with banks whose plans were deemed not commensurate with their risk profile. Average Pillar 2 requirements (P2R) and Pillar 2 guidance (P2G) remained broadly stable and in line with previous years: a marginal increase in the average P2R was driven by add-ons to P2R which were imposed on banks whose provisioning of legacy non-performing exposures was not yet in line with previously communicated coverage expectations. Average P2G has marginally increased owing to higher capital depletions in the 2021 EU-wide stress test. The methodology for determining P2G was revised for the 2021 SREP.

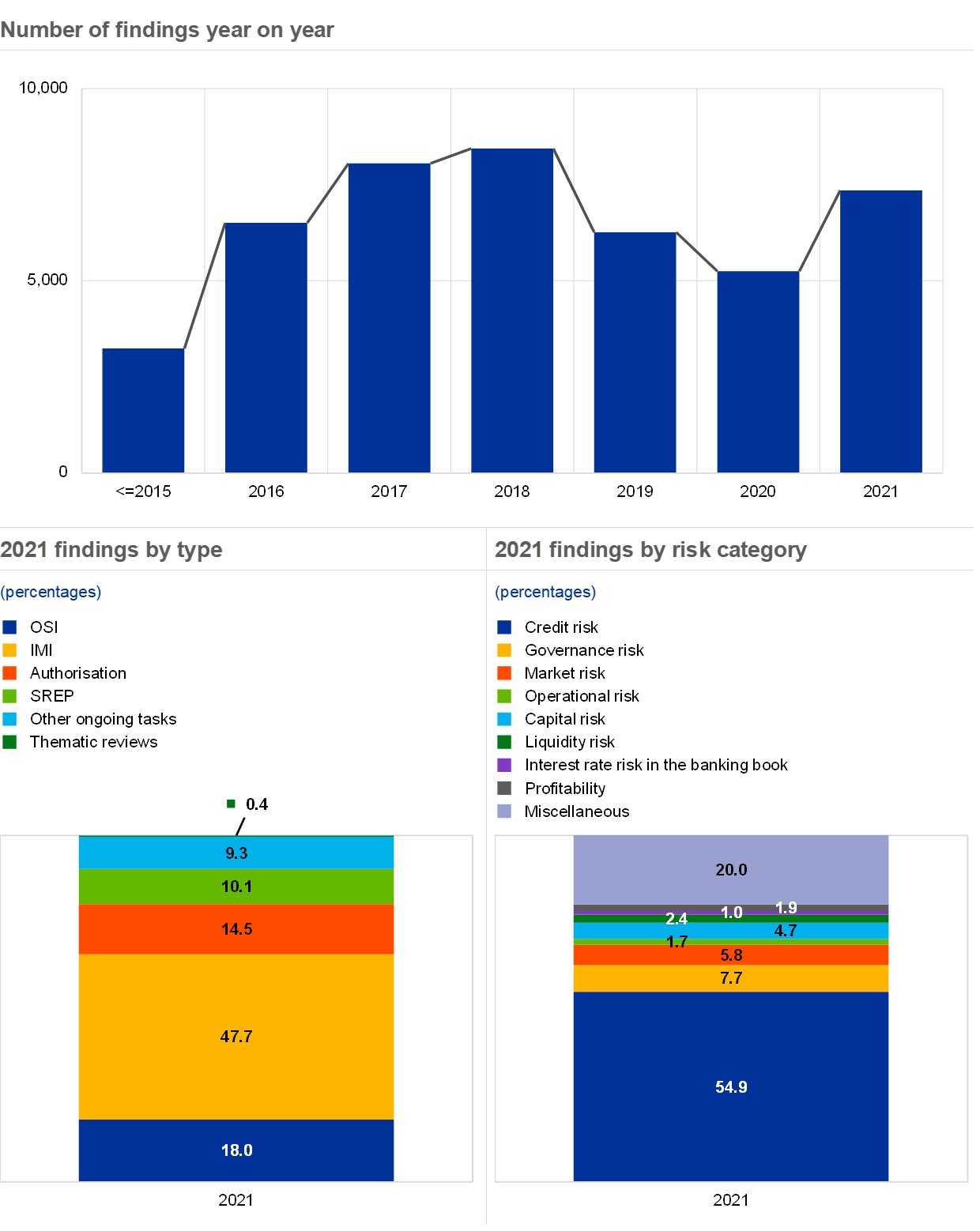

Supervisory findings

Supervisory findings are one of the main outcomes of the regular supervisory activities and reflect shortcomings that need to be remedied by banks. The JSTs are responsible for monitoring how banks follow up on these findings. As at 29 December 2021, the overall number of findings increased in comparison with 2020, reaching a level similar to that seen before the pandemic. This was mainly caused by the partial resumption of on-site inspections (OSIs) and internal model investigations (IMIs)[15]. The majority of the findings originated from IMIs, OSIs and activities related to authorisations. The largest number of findings were reported in the area of credit risk (Chart 15).

Chart 15

Source: ECB

Notes: The sample includes findings from all JSTs working in banking supervision (varying sample). 23 findings from old JSTs have been excluded. Data extracted as at 29 December.

On-site supervision

In 2021 most missions were performed remotely off-site

In 2021 the COVID-19 pandemic continued to significantly affect how OSIs and IMIs were carried out. Most missions[16] were performed off-site, as in 2020. From October 2021 onwards, a hybrid approach was adopted for a number of inspections, combining the traditional on-site presence at the premises of the supervised entity with a greater reliance on remote working arrangements tested during the pandemic.

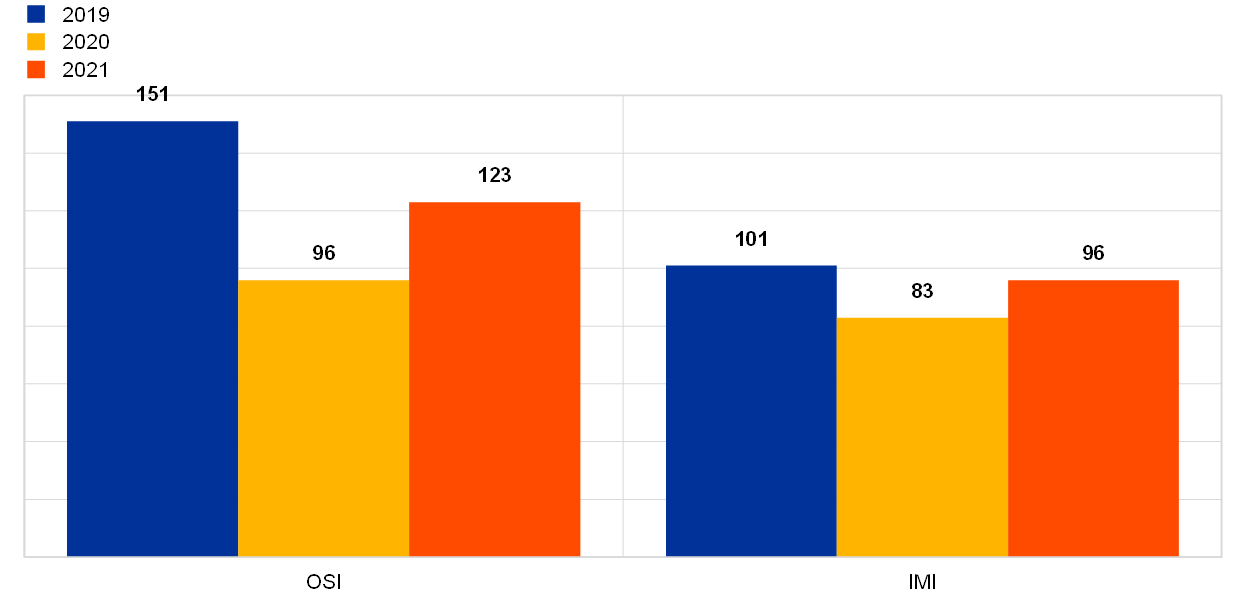

Following the slow-down experienced in 2020, 123 OSIs and 96 IMIs were launched in 2021, moving closer to the levels seen before the pandemic (Chart 16).[17]

With regard to OSIs, the campaign approach used in previous years continued to be applied[18], complementing the bank-specific OSIs requested by JSTs. In line with the supervisory priorities for 2021, key campaigns launched by the ECB included: (i) the commercial real estate (CRE) campaign which assessed the quality of banks’ exposures to the CRE sector by challenging collateral valuations; (ii) the large SME/corporate campaign, which focused on the management, monitoring and control of the relief measures granted in response to the crisis; (iii) the granular portfolios campaign, which reviewed banks’ IFRS 9 provisioning frameworks; (iv) the market risk campaign on valuation risk; (v) the IT and cybersecurity campaign; (vi) the internal capital adequacy assessment process (ICAAP) campaign; and (vii) the business model and profitability campaign.

For IMIs, the main topics addressed in 2021 concerned the implementation of new EBA regulatory products, the temporary tolerance of models in the context of Brexit, and follow-ups to the targeted review of internal models (TRIM). In addition, a new off-site investigation approach was adopted for the first time in 2021 to deal with less material or less complex model change requests; these investigations have a very targeted scope and a resource-light assessment concept.

Chart 16

OSIs and IMIs launched in 2019, 2020 and 2021

(number of investigations)

Source: ECB Banking Supervision.

In 2021 ECB Banking Supervision began exploring new approaches to enrich the on-site investigations model

While preserving the primacy of the on-site approach to mission work, the gradual return to a normal work environment will incorporate the valuable lessons learned and good practices acquired during the pandemic as regards remote working modalities. To this end, ECB Banking Supervision began exploring ways to enrich the traditional on-site model by integrating hybrid working modalities that can improve the overall efficiency, agility and resilience of investigations while maintaining their thoroughness, intrusiveness and quality. These approaches also aim to reduce the environmental impact of investigations while further promoting cross-border[19] and mixed team[20] cooperation, fostering integration across European banking supervision, and supporting diversity and inclusion.

Key findings from OSIs

The following analysis provides an overview of the most critical findings identified in OSIs.[21]

Credit risk

In the context of the COVID-19 pandemic, credit risk OSIs were mainly conducted off-site and had a qualitative focus. Their purpose was to assess the robustness of credit risk management and control as well as the implementation of relief measures. In the sample considered for this analysis, only a limited number of investigations were based on a more quantitative approach focusing on credit file reviews; these led to additional reclassifications of exposures amounting to €855 million and additional provisions of €1 billion.

In 2021 credit risk inspections highlighted the following important weaknesses in how banks carry out and monitor key credit risk processes in the pandemic environment.

- Underestimation of expected credit losses (ECL): overvaluation of collateral and inappropriate ECL calculations owing to shortcomings in the estimation of key parameters.

- Credit underwriting and loan origination: poor eligibility controls related to the granting of COVID-19 relief measures.

- Inappropriate classification of debtors: shortcomings in the assessment of financial difficulties leading to UTP and forbearance classifications and to identification as stage 2 under IFRS 9.

- Weak monitoring processes: inadequate oversight of credit risk by the supervised banks’ management bodies and shortcomings in the adaptation of early warning systems and rating models to COVID-19 developments and government support measures.

Internal governance

The most critical findings[22] revealed deficiencies in the following governance areas.

- Internal control functions (including compliance, risk management and internal audit): severe shortcomings in the status, resources and scope of activity of all internal control functions.

- Risk data aggregation and risk reporting: insufficiently comprehensive risk management reporting and weaknesses in data architecture and IT infrastructure.

- Outsourcing: inadequate risk assessments for decision-making on outsourcing and flaws in the delivery and monitoring of outsourced services, especially in relation to IT services.

- Corporate structure and organisation: weak institution-wide risk culture, deficiencies in internal control frameworks and inadequate human and technical resources.

Market risk

The market risk campaign on valuation risk was concluded in 2021. This three-year initiative was launched with the aim of promoting a level playing field for banks based on a common methodology and providing consistent follow-up to findings from on-site missions. The main weaknesses identified in 2021 were related to fair value measurement and additional value adjustments (insufficient independent price verification coverage, inadequate methodologies for the fair value hierarchy and additional value adjustments, inappropriate day one profit recognition practices). Shortcomings were also identified in the management of market data to ensure reliable valuation inputs.

IT risk

In 2021 the main focus of IT risk OSIs was cybersecurity. Most of the high-severity findings were related to deficiencies in:

- banks’ cybersecurity management to identify potential cyber threats and risks and maintain an accurate inventory of all IT assets;

- how banks safeguard their IT assets and provide sufficient cybersecurity awareness training for their staff;

- banks’ restoration capabilities after disruptions from cyber incidents.

Regulatory capital and ICAAP

The main findings on regulatory capital (Pillar 1) were related to: (i) the underestimation of risk-weighted assets (RWAs) as a result of incorrectly allocating exposure classes; (ii) the use of ineligible collateral for credit risk mitigation techniques; and (iii) low data quality (e.g. for the recognition of guarantees). In addition, several weaknesses in the control framework were identified, such as the limited capacity to identify the incorrect use of risk weights for Pillar 1 risks.

The most severe issues identified in ICAAP inspections concerned: (i) internal quantification methodologies (e.g. for credit risk, market risk or pension risk); (ii) the definition of internal capital; (iii) the incorrect design and level of severity of the adverse scenarios; and (iv) the incompleteness of the capital planning process.

Interest rate risk in the banking book (IRRBB)

The majority of critical findings were related to weaknesses in the perimeter and risk identification of IRRBB and deficiencies in the audit plan for IRRBB management functions and the measurement and monitoring of IRRBB. Behavioural modelling assumptions, model validation functions and limit systems were found to be particularly insufficient or inadequate.

Operational risk

The most severe findings were related to the management of operational risks, with deficiencies in operational risk monitoring processes and inadequate quality assessments of operational risk data, risk prevention and remediation actions when dealing with operational risk events.

Liquidity risk

The majority of high-severity findings were related to weaknesses identified in the stress testing framework (stress test scenarios with insufficient coverage of all material liquidity risk sources, limited use of reverse stress-testing approaches and insufficiently conservative mitigating actions) and in risk measurement and monitoring (deficiencies in the set-up of internal limits).

Business model and profitability

The most critical findings were related to deficiencies in income, cost and capital allocation (contributing to a distorted view of the profitability of different business lines) and to the sensitivity analyses of financial projections (e.g. limited capacity to anticipate changes in key risk drivers such as the cost of credit).

Main topics of IMIs

In April 2021 the ECB published the results of TRIM[23], which aimed to assess whether the Pillar 1 internal models used by SIs are appropriate in the light of regulatory requirements and whether their results are reliable and comparable.

Under TRIM, 200 on-site IMIs across 65 SIs were performed between 2017 and 2019. Overall, the outcomes of the TRIM investigations confirmed that the internal models of SIs can continue to be used for the calculation of own funds requirements. However, for a certain number of models, limitations were needed to ensure an appropriate level of own funds to cover the underlying risk. In total, over 5,800 findings were identified across all risk types, of which around 30% had a high severity, requiring a significant effort by the institutions to remediate the deficiency by pre-defined deadlines.

While banks have started to address TRIM findings and the assessment of these remediation activities has been included in the scope of some IMIs, in 2021 a significant number of internal model-related requests were driven by the need for banks to change their models to comply with new EBA products.

For credit risk, a significant number of model change applications related to the EBA’s guidelines on the application and definition of default[24] and its internal ratings based (IRB) repair programme[25], for which institutions have to ensure compliance by 1 January 2021 and 1 January 2022 respectively. Furthermore, a high number of applications related to reverting to less sophisticated approaches, especially in the context of the initiatives launched by banks to simplify their model landscapes. For market risk, in addition to the follow-up on TRIM findings, several investigations were performed to assess model changes related to the inclusion of valuation adjustments in the internal models for market risk as well as other specific model change requests. Finally, initial approvals of internal models previously under temporary tolerance (for example owing to new SIs linked to Brexit or institutions subject to consolidation) were within the scope of ECB Banking Supervision’s assessments.

In total, 214 supervisory decisions on IMIs[26] (including for TRIM) were issued in 2021.

1.4 Indirect supervision of LSIs

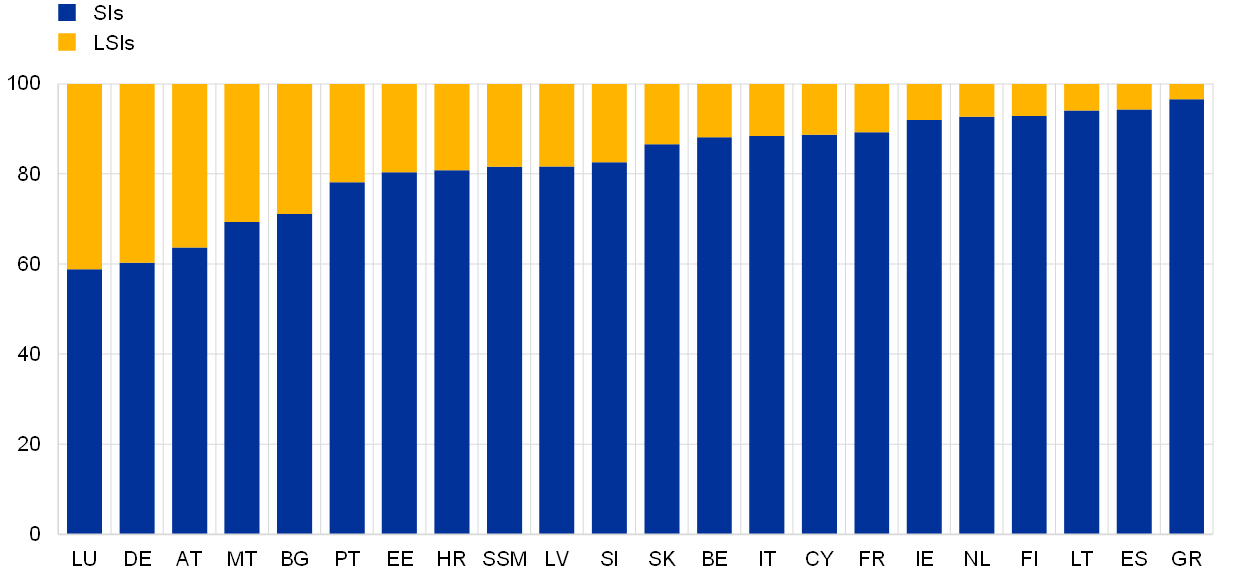

In 2021 the “market share” of the LSI sector remained unchanged

The number of LSIs fell in 2021 but the LSI sector managed to maintain its “market share”, representing 18.4% of total SSM banking assets. However, the weight of the LSI sector in the countries where they operate varies widely across countries participating in European banking supervision (Chart 17). While LSIs represent around 40% of total banking assets in Luxembourg and Germany, their importance is substantially lower in other countries, notably in Greece and Spain (3.4% and 5.7% respectively), whose banking systems are dominated by SIs. Relative to the size of their domestic economy, the biggest LSI sector can be found in Luxembourg, where LSIs primarily focus on private banking and custodian banking and accumulate assets representing 210.8% of GDP. The next two largest LSI sectors with respect to GDP are located in Austria (94.4%) and Germany (88.0%).

Chart 17

Market share of SIs and LSIs by country

(as a percentage of total assets)

Source: ECB.

Notes: Data as at 30 June 2021. Data reflect the highest level of consolidation, with the exception of Bulgaria, Croatia and Slovakia. For these three countries, the data include local subsidiaries of cross-border institutions in order to avoid a material misrepresentation of the market shares of SIs and LSIs.

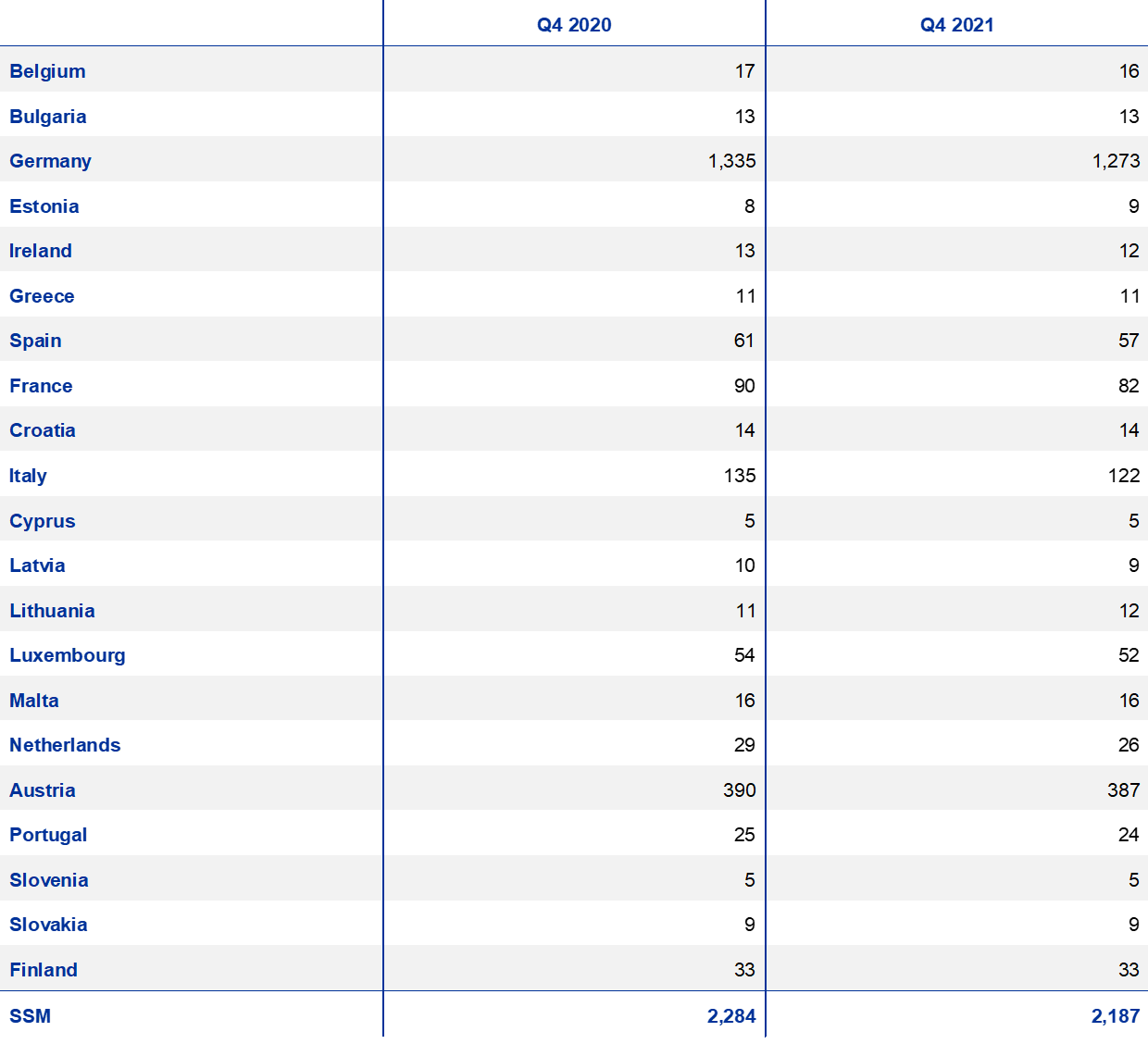

The overall number of LSIs decreased in 2021[27], despite 27 new LSIs being added to the ECB’s list of LSIs following the establishment of close cooperation between the ECB and Българска народна банка (Bulgarian National Bank) and Hrvatska narodna banka. According to the ECB’s list of LSIs, there were 2,187 LSIs as at the end of December 2021, a 4.2% decline on the previous year. As at the end of December 2021, 81.5% of all LSIs were domiciled in Germany, Austria and Italy, reflecting the presence of large decentralised systems of savings and/or cooperative banks in those countries. In terms of the share of total LSI banking assets, Germany accounted for 53.6%, while Austria and Italy each accounted for 6.5%.

In line with ongoing trends in the European banking industry, consolidation in the LSI sector continued to advance in 2021, albeit at a slower pace. A total of 61 LSIs were acquired or merged in 2021, compared with 69 in 2020. Given the larger number of German LSIs, most of the mergers in the last two years affected its LSI sector (with 32 in 2020 and 49 in 2021). In Italy, the consolidation of the cooperative banking sector into two major groups was concluded in 2019, while in Austria 26 LSIs merged in 2020. In 2021 there were no major developments in the LSI sectors of those two countries.

Table 1

Number of LSIs per country

Source: ECB.

Note: Data reflect the highest level of consolidation, except for Bulgaria, Croatia and Slovakia.

Selected LSI oversight activities

The aggregate NPL ratio of LSIs continued to decrease despite the pandemic, standing at 2.1% in June 2021, down from 2.3% in June 2020. In a similar vein, the number of high-NPL LSIs[28] also fell further, to 217.

While LSIs’ NPL ratios continued to decrease in 2021 despite the pandemic, the fact that many national support measures expired mid-year warrants further scrutiny in the future

In its LSI oversight capacity, the ECB focused on assessing, with the support of the national competent authorities (NCAs), the impact of the pandemic and of the wind-down of relevant national support measures on LSIs’ credit risk profiles, as well as LSIs’ readiness to deal with a potential increase in defaulting exposures. While the LSI sector appears to be broadly resilient to the negative effects of the crisis, the fact that the bulk of national support measures expired in the middle of 2021 warrants further scrutiny in the future. Therefore, credit risk activities in 2022 will continue to focus on assessing the effect of the pandemic on LSIs’ asset quality and on ensuring a consistent supervisory response across countries participating in the SSM.

In 2021 the ECB started a dialogue with NCAs on the fastest-growing LSIs in their countries. The NCAs provided their assessments of each of the fast-growing banks and outlined the supervisory actions being taken to ensure that they are not taking excessive risks. It was agreed to make this an annual exercise for supervised LSIs.

LSIs’ use of deposit platforms to attract deposits has been increasing

LSIs’ use of online deposit platforms to attract deposits has been increasing. The ECB has worked closely with the NCAs to better understand how banks are using these platforms and to find out more about NCAs’ supervisory approaches in this area. The purpose of the work on online deposit platforms is to gain greater visibility on the issue and a better understanding of the associated risks.

Governance has long been an area of supervisory focus. In 2021 the ECB, in cooperation with the NCAs, launched a thematic review on LSIs’ internal governance.

A thematic review on LSIs’ internal governance was launched by the ECB in cooperation with the NCAs

The focus of this thematic review is twofold and covers:

- the governance arrangements of LSIs in terms of the composition and functioning of the management body in its supervisory function (size, expertise, formal independence, committee structure, reporting lines, etc.) as well as their internal control functions;

- NCAs’ supervisory practices for governance in LSIs, with a particular focus on standard-setting and off-site and on-site supervisory activities.

The ECB and the Austrian Financial Market Authority (Finanzmarktaufsicht) approved the Raiffeisen institutional protection scheme (IPS) in 2021. The reorganised IPS has been recognised for prudential purposes since 28 May 2021. The ECB also conducted further monitoring activities for hybrid IPSs, some of which are undergoing significant changes. In this context, the ECB and the relevant NCA are following-up on the remediation actions taken by one IPS to address concerns raised by the ECB’s Supervisory Board.